Inglés (pdf)

Inglés (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Enviar articulo por email

Enviar articulo por email Citado por SciELO

Citado por SciELO  Similares en

SciELO

Similares en

SciELO

Permalink

PermalinkIntroduction

There is continuing interest among scholars and policymakers in the roles that fiscal policy plays in the mobilization and allocation of resources necessary to facilitate the realization of desired economic outcomes consistent with a country's development agenda (Moreno-Dodson, 2012). However, many developing and emerging market economies have experienced rising budget deficits in recent years, with growing concerns over implications for future fiscal sustainability, debt and macroeconomic stability (Kose et al., 2021). More recently, the coronavirus disease 2019 (COVID-19) pandemic has precipitated large macroeconomic imbalances, leading to loss of fiscal sustainability across many countries (Burger and Calitz, 2021; Makin and Layton, 2021; Brodeur et al., 2021).

While the literature on the macroeconomic determinants of fiscal deficits is voluminous, however, findings are inconclusive (Saleh and Harvie, 2005). In addition, existing studies have tended to focus on single-country case studies, limiting the generalization of findings to a wider range of country contexts (Mawejje and Odhiambo, 2020). While weak growth and low-interest rates explained the rising fiscal deficits in the pre-COVID-19 period (World Bank, 2019a), recent experiences suggest more nuanced developments, necessitating new and comprehensive analyses of the determinants of fiscal deficits. Indeed, evidence shows that in comparison to previous periods, the COVID-19 pandemic has precipitated disproportionately larger fiscal deficits and macroeconomic effects (Makin and Layton, 2021; Alberola et al., 2021). At the same time, if rising fiscal deficits result in unsustainable accumulation of debt, then new vulnerabilities would emerge with implications for growth and macroeconomic management (IMF, 2020a).

The purpose of this paper is to investigate the dynamic causality linkages between fiscal deficits and selected macroeconomic indicators. We examine these issues in five East African Community (EAC) member countries, namely Burundi, Kenya, Rwanda, Tanzania and Uganda. The analysis excludes South Sudan due to significant data limitations. The EAC is considered one of the most dynamic African regional economic communities with aspirations of becoming a monetary union (Drummond et al., 2015). Within the regional economic integration framework, EAC member countries agreed upon macroeconomic convergence targets that include inflation, fiscal deficits, debt and interest rates. Specifically, the target for fiscal deficits is 3% of gross domestic product (GDP), intending to maintain gross public debt levels below 50% of GDP in net present terms (Ltaifa et al., 2015). However, attaining converge may experience challenges as fiscal deficits have been rising over the past decade leading to the build-up of public debt across the region (IMF, 2018). In addition, emerging vulnerabilities including those related to the COVID-19 pandemic that has affected growth and led to higher financing needs may derail progress amidst heightened global uncertainty (African Development Bank, 2020; IMF, 2020b).

This study contributes to two strands of the literature. First, the study contributes to the literature on the macroeconomic determinants of fiscal deficits. Second, the study contributes to the literature on the macroeconomic effects of fiscal deficits in regional economic communities in developing economies. As has been argued by Papageorgiou et al. (2016), fiscal policy is probably the most important tool in dealing with country-specific fluctuations in a regional economic community. However, devising requisite responses requires a clear understanding of the determinants of fiscal policy and their dynamic causality linkages.

The rest of the paper is organized as follows: Section two provides a review of the literature and develops a simple analytical framework. Methods are discussed in Section three. Section four presents the results. A brief discussion is provided in Section five. Section six concludes.

Literature review

The determinants of fiscal deficits

From a theoretical perspective, the literature espouses four views that explain fiscal policy outcomes. The Ricardian equivalence theory postulates that fiscal deficits are neither determined nor yield any macroeconomic effects in the long run (Barro, 1989; Seater, 1993). The Keynesian theoretical view links fiscal deficits to investment and growth (Bernheim, 1989; Eisner, 1989). The neoclassical theory describes budget deficits as arising from market lending and borrowing decisions in inter-temporal optimization problems (Bernheim, 1989). This theoretical exposition gives rise to the twin-deficit hypothesis which describes a causal linkage between a country's fiscal and current account balances (Kim and Roubini, 2008). The fourth view describes fiscal deficits as arising out of political economy contestations (Alesina and Perotti, 1995; Eslava, 2011).

The empirical literature examining the determinants and effects of fiscal deficits using dynamic causality models is scant but evolving. Employing the Gregory and Hansen cointegration methodology, as well as asymmetric cointegration techniques, Trachanas and Katrakilidis (2013) showed that the twin deficits hypothesis holds for Portugal, Ireland, Greece and Spain. These findings are consistent with research by Xie and Chen (2014) who used bootstrap panel Granger causality methods to show that there is bi-directional causality between the current account deficit and the government budget deficit for eleven Organisation for Economic Co-operation and Development (OECD) countries. However, these results are contrasted by, among others, Sobrino (2013), who used quarterly data and Granger causality methods to reject the twin deficits hypothesis and instead show that current account balances cause fiscal deficits in Peru.

Research examining the dynamic nexus between fiscal deficits and inflation has provided useful insights. Catao and Terrones (2005) investigated the dynamic linkages among fiscal deficits and inflation in a panel of 107 countries over 1960-2001. Using the mean group and pooled mean group estimators within the panel Autoregressive Distributed Lag (ARDL) framework, results showed that budget deficits are significant drivers of inflation among high-inflation and developing country groups, but not among low-inflation advanced economies. These results are consistent with a wide range of literature that shows the positive dynamic relationship between budget deficits and inflation (Bhat and Sharma, 2020; Nguyen, 2015; Lin and Chu, 2013).

Investigations of the dynamic relationship between fiscal deficits and real economic growth have attracted much attention in the literature. Afonso and Jalles (2014) examined the causal dynamics between fiscal policy and economic growth. Using panel Granger causality methods on a large panel of 155 countries for the period 1970-2010, they uncover strong causality running from fiscal policy (government expenditures) to per capita GDP, but no evidence to support Granger causality from per capita GDP to government expenditure. More recently, Magazzino (2016) examined the relationship between fiscal variables and economic growth in panels of economic groups in Sub-Saharan African countries using annual data for the period 1980-2011, finding a positive relationship between the two variables. Specifically, a 1 percentage point reduction in economic growth would widen budget balances by about 0.18 percentage points for the West African Economic and Monetary Union (WAEMU) countries.

Research findings on the dynamic nexus between budget balances and interest rates have been inconclusive. Vamvoukas (2002) used a combination of seemingly unrelated regressions (SUR) and impulse response functions and concluded that bidirectional causality exists between budget deficits and interest rates using data on a small open economy. Cheng (1998) applied the two-step Engle-Granger causality methodology but found no causality between fiscal deficits and long-term interest rates in Japan. However, Cheng (1998)uncovered feedback causality between fiscal deficits and short-term interest rates using Hsiao's approach to causality testing. Uwilingiye and Gupta (2009) concluded that budget deficits Granger cause interest rates in South Africa with no feedback confirmed in a multivariate vector error correction framework. However, García and Ramajo (2004) did not find evidence to support the validity of causality between budget deficits and interest rates in Spain using error correction methods within the ARDL framework.

The literature shows that access to grants and loans has important implications for fiscal policy (Morrissey, 2015). There has consequently emerged an interesting thread of literature examining the fiscal effects of aid in developing countries. Within this realm, Bwire et al. (2017a) examined the dynamic causal links among aid and fiscal variables in Uganda, over the period 1972 to 2014 using a cointegrated vector autoregressive (CVAR) model with both annual and quarterly data. Importantly, they show that these variables form a stable long-run cointegrated relationship, implying causality in at least one direction. These findings are consistent with recent analyses on Ethiopia (Mascagni and Timmis, 2017), Rwanda (Bwire et al., 2017b) and Ghana (Osei et al., 2005).

More recent analyses have focused on the determinants of fiscal policies in the wake of the COVID-19 crisis. Within this realm, Benmelech and Tzur-Ilan (2020) showed that low-income countries with poor credit ratings had smaller fiscal space to respond more meaningfully to the crisis than high-income countries. In Africa, the fiscal effects of the pandemic are estimated to be especially severe with estimates indicating that fiscal deficits doubled in 2020 leading to increased debt burdens (African Development Bank, 2021). For many countries, however, the pandemic exacerbated an already precarious fiscal position, with depleted buffers offering limited space to manoeuvre, leading to loss of fiscal sustainability (Burger and Calitz, 2021; Makin and Layton, 2021; Brodeur et al., 2021). To restore fiscal sustainability, governments may consider growth-enhancing budget-neutral reallocation of expenditures, reliance on external grants and concessional lending, while avoiding inflationary financing of the budget (Loayza and Pennings, 2020).

Analytical framework

This study proposes a framework in which fiscal deficits are determined through the interaction of activities of households, government and external sector developments.

The household sector

The current study presents a representative household that maximizes an inter-temporal utility function that is dependent on the consumption of a homogenous good, defined in equation (1).

where C t refers to a consumption basket, and β t is the subjective discount factor, such that (0<β<1), i.e. β is strictly positive (non-negative) and less than unity. U defines a utility function that is assumed to be strictly increasing and concave in consumption.

Following earlier work that modelled household intertemporal budget constraints in general models for fiscal deficit determination, the study makes the following assumptions: (1) that the household is endowed with a positive quantity of a good Y t ; (2) that the household pays taxes Ƭt and can either consume or transfer the after-tax endowment over time by money holdings or through risk-free bonds (Catao and Terrones, 2005). Therefore, the household's inter-temporal budget constraint can be constructed as defined in equation (2).

whereC t is household consumption defined as previously;b t p represents the real value of household-held risk-free bonds;m t+1 represents household's holding of money balances;τ t is a lumpsum tax at periodt;p t is the price level and Rt ∗is the international real gross rate of return on one-period bonds. Rearranging equation (2), and defining inflation as

or a change in prices, and

defined as the real change in household holdings of real bonds, we can then define the household budget constraint as shown inequation (3). In this postulation, for a given level of income, consumption and taxes, the household budget deficit can be defined as a function of holdings of real bonds and inflation. Please note that the stock of bonds that a household can hold at any time, t can be expressed as a function of real disposable income and interest rate (or the return on bonds), such that:

Substitutingequation (3)intoequation (2)yields the optimal household budget constraint which can be thought of as a function of interest rates, defined as the return on government-issued debt/bonds, it and inflation, πt as shown inequation (4).

The government sector

In each period, government fulfils its budgetary obligations either by collecting taxes, issuing debt, running down reserves or printing money. Governments can also receive transfers or grants in the form of Overseas Development Assistance (ODA). Drawing from the public finance and fiscal sustainability analysis literature (Blanchard, 1985;Taylor et al., 2012), the government inter-temporal budget constraint can be defined as:

where Dt is the stock of public debt that includes both domestic and foreign debt; i is the average nominal interest rate; Bt is the budget balance defined as the difference between Tt and primary expenditure St; and Rt is access to grants. Assuming that nominal GDP growth is g, i.e. GDPt=(1+g)∗GDPt−1,equation (5) can be divided by GDPt and rearranged to obtainequation (6).

Rearrangingequation (6)yields the government budget deficit as a function of GDP growth rate, interest rates, debt and access to foreign grants as shown inequation (7). Specifically,equation (7)shows that budget deficits will be higher, the higher are interest rates; the lower is growth; the higher is debt (or debt servicing flows), and the higher are grants.

The external sector

The current account balance reflects a country's external position with the rest of the world. In this respect, the Mundell-Fleming model, based on the seminal works ofMundell (1963) andFleming (1962), provides a useful starting point and building blocks for the relationship between fiscal policy and the external sector. Building on the Mundell-Fleming framework,Abbas et al. (2011)provide a framework in which fiscal policy and the current account are represented using the following identity inequation (8)

where cat represents the current account; tbt is the trade balance; tbt are transfer payments. Spt and Ipt are private savings and investment respectively; Sgt and Igt are government savings and investment respectively. In the absence of government transfers to the private sector, Sgt − Igt is equivalent to the fiscal balance. In this respect, therefore, the budget balance, bt, can be expressed as a function of the current account balance cat and the private savings-investment gap (Spt−Ipt), such that:

Drawing from various theoretical underpinnings, including the accelerator principle and the saving and investment literature (Samuelson, 1939); intertemporal saving and investment models (Abel and Blanchard, 1983); and the intertemporal postulation of current account dynamics (Obstfeld and Rogoff, 1995), savings and investments are related to the GDP growth rate, gt, and interest rates, it. Thus, equation (9)can be reformulated in terms of the current account, cat; real GDP growth rate, gt and interest rates, it, as shown inequation (10).

The general model

Combining the determinants of budget balances from the household, government and external sectors into a single model yields the following general model (equation 11) that provides a useful framework for carrying out an empirical evaluation of the determinants of fiscal deficits in a given country:

Hypotheses

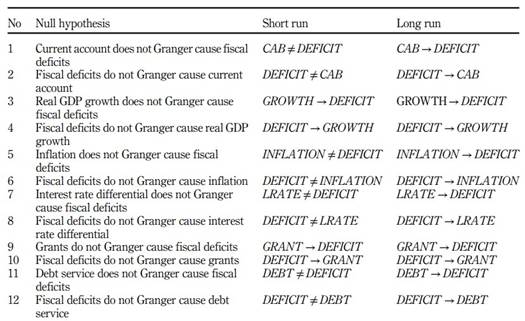

This general model specifies the determinants of fiscal deficits as interest rates, real GDP growth rate, debt (or debt service), grants, current account balance and inflation. Following the general model specified in equation (11), the following testable hypotheses are investigated:

H1. Current account does not Granger cause fiscal deficits;

H2. Real GDP growth does not Granger cause fiscal deficits;

H3. Inflation does not Granger cause fiscal deficits;

H4. Interest rate does not Granger cause fiscal deficits;

H5. Grants do not Granger cause fiscal deficits;

H6. Debt service does not Granger cause fiscal deficits.

Method

Data

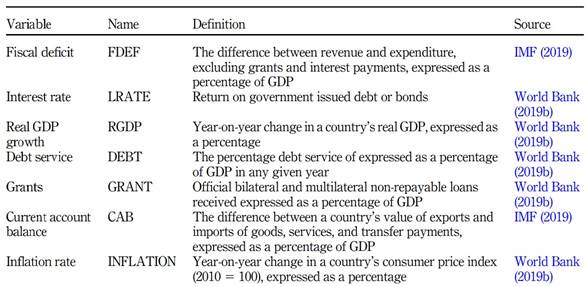

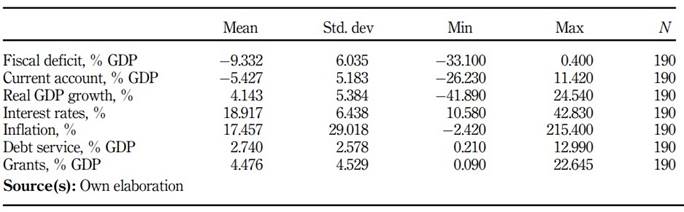

The study constructed a balanced panel dataset, spanning 38 years during 1980-2017, from annual time series data for each of the five East African countries considered in this study. Specifically, the study considers the following variables, chosen as appropriate from a review of extant literature as well as well availability of full and consistent data for all the countries: fiscal deficits (% GDP), current account balance (% GDP), real GDP growth; interest rates; debt service (% GDP) and grants (% GDP). Fiscal and current account balances data are sourced from the IMF's World Economic Outlook (IMF, 2019). Real GDP growth rates, interest rates, public debt service, grants and inflation data are sourced from the World Bank's (2019b) World Development Indicators (WDI). Table 1 summarizes the variables used in this study, including their definitions and sources. The descriptive statistics are provided in Table 2.

Research design

Panel unit root tests

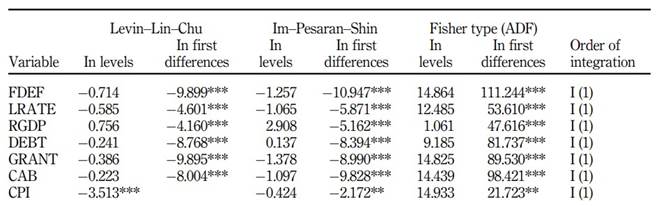

To ascertain the levels of integration of the variables, this study performed three unit root tests that include Im-Pesaran-Shin; Levin-Lin-Chu and Fisher-type Philips-Perron tests. The test results provided in Table 3 show that all variables are integrated of the first order, I(1).

Table 3 Panel unit root tests

Note(s): (1) Tabulated are test statistics; (2) *, ** and *** denote statistical significance at the 10%, 5% and 1% levels, respectively; (3) For all unit root tests the null hypothesis is specified as follows: Ho: Panels contain unit roots; (4) All tests are carried out including individual intercept and trend Source(s): Own elaboration

Panel cointegration tests

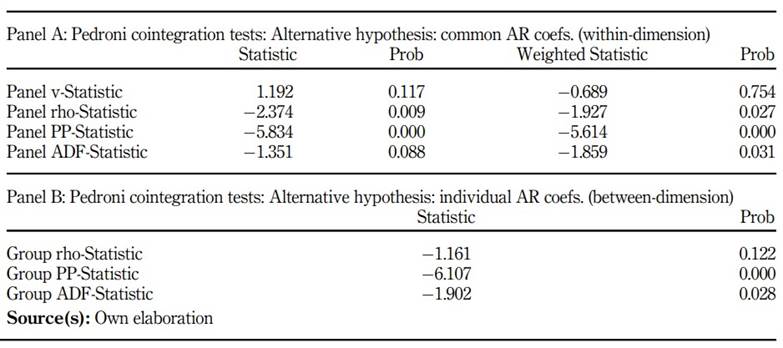

This study performs cointegration tests based on Pedroni (1999, 2004). These test procedures investigate the null hypothesis of no cointegration, against the alternative hypothesis that the variables are cointegrated in all panels. It is important to note that the tests are restricted to a maximum of seven covariates in the underlying panel regressions. Pedroni's co-integration test results in Table 4 show that, except for the panel v-statistic in panel A and group-rho statistics in panel B, all other statistics are significant, so the null hypothesis of no cointegration is rejected.

Panel-based cross-section dependence tests

The literature indicates that panel-data models are likely to suffer cross-section dependence in their error terms. This may be due to some reasons including spatial dependence, idiosyncratic pairwise dependence in the disturbances, the presence of common shocks and unobserved components that may be absorbed in the error term (Pesaran, 2021; Baltagi, 2005; Anselin, 2001). Cross-section dependence was shown to decrease estimation efficiency significantly and the usefulness of panel estimators over single equation least-squares methods may be lost (Phillips and Sul, 2003).

This study carried out two cross-section dependence tests suggested by Pesaran (2021) and Frees (1995) to ensure that cross-country correlations are not present and to avoid inconsistent parameter estimation. The general null hypothesis is in these tests is that the errors for the estimated panel regression are uncorrelated, that is, allowing to test the hypothesis that there is no cross-section dependence in the panel data. The test results for cross-sectional dependence are provided in Table 5. Results show that the null hypothesis of no cross-section dependence cannot be rejected based on the Pesaran and Frees tests. This study, therefore, concludes that there is no cross-section dependence based on the Pesaran and Frees test results.

Analytical procedures

Multivariate Granger causality tests

Investigations of the dynamic causal relationship among variables can be traced to the seminal work ofGranger (1969)who developed a bivariate causality testing framework based on time series data. More recently,Dumitrescu and Hurlin (2012)developed a procedure for implementing pairwise Granger causality tests in panel datasets. In this framework, a variable, say Yit, is said to Granger cause another variable, say, Zit if, given the past information or values of Zit, past values of Yit are useful in predicting Zit. A convenient way for testing Granger causality involves regressing Zit on its owned lagged values and lagged values of Yit and test for the joint significance of the estimated coefficients on Yit. If the coefficients on Yit are non-zero, then we can conclude that Yit Granger causes Zit, that is past information in Yit can be used to predict Zit.

However, pairwise Granger causality testing has been criticized for disregarding the short-run adjustment mechanisms that exist in level relationships. Therefore, these tests could suffer significant misspecification biases unless the lagged error correction terms are included if the variables are cointegrated (Granger, 1988). Importantly, these tests do not allow testing for both short-run and long-run Granger causality in a single framework. Moreover, these tests might suffer omitted variable bias if other control variables are not included. Multivariate Granger causality testing allows us to circumvent such shortcomings by including, as additional control variables, the differenced lagged values of all variables under consideration, in a panel ARDL error correction framework.

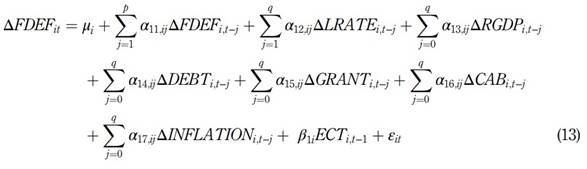

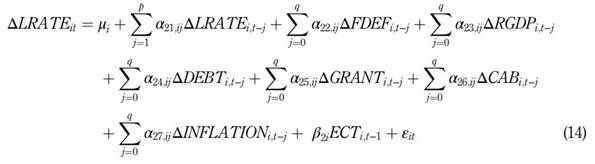

Following Engle and Granger (1987), we use a two-step procedure to implement multivariate panel Granger causality testing. The first step involves estimating a pooled long-run model in levels to generate the estimated residuals. This is done by estimating a system of models represented in equation (12).

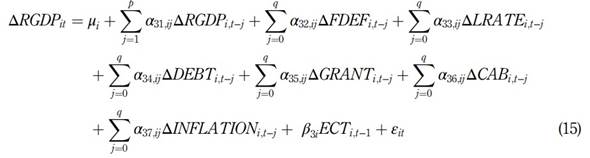

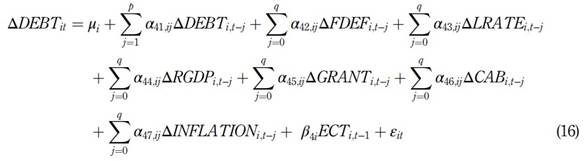

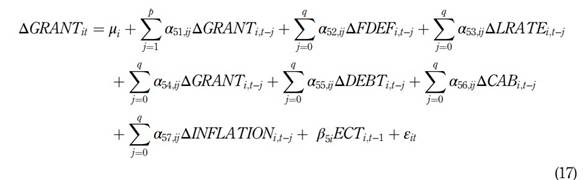

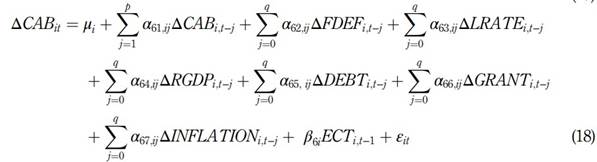

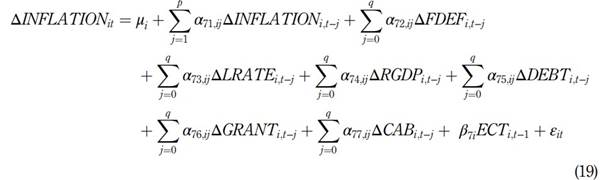

The second step involves using the lagged residuals from equation (1) above as the error correction terms in a panel ARDL system of equations used to test for both short-run and long-run multivariate Granger causality. This system of models is expressed in equations (13, 14, 15, 16, 17,18 and 19).

All variables are as previously defined, Δ denotes the first difference for each variable, ECT denotes the error correction term,pis the lag length of the autoregression,qis the lag of the distributed lags. Based on the error correction formulation in equations (2)-(8), we test for both short-run and long-run panel multivariate Granger causality between fiscal deficits and the vector of endogenous regressors included in the model. Short-run Granger causality is tested by the joint WaldFtest for coefficient restrictions. Long-run Granger causality is tested by attest of theβcoefficients for the ECT for each panel multivariate function once a long-run relationship is confirmed.

Impulse response functions

In addition to the panel error correction-based Granger causality tests, the study considers a dynamic panel autoregressive distributed lag model that is specified as shown in equation (20).

whereFDEFis described as before, Zitis a vector of other macroeconomic variables included in the model and εitare disturbances that are assumed to be independently and identically distributed.A(L)andB(L)are thepthandqthorder lag operators withp≥1 and withq≥0. In the benchmark model, we usep=1 andq=1.

The richness of our dataset provides critical advantages. Specifically, the dynamic feature of the panel autoregressive distributed lag model allows us to use impulse response functions to capture the dynamic relationships among budget deficits and selected macroeconomic variables. The impulse response function is given by the expression inequation (21).

Results

Multivariate panel granger causality analysis

In examining the multivariate panel Granger causality dynamics, the study followed the Engle and Granger (1987) two-step procedure. The first step involves estimating seven long-run models in levels using pooled panel regressions (see equation 12). These models are then used to generate residuals that represent the long-run cointegrating vector. The second step involves using the lagged residuals generated in equation (12) as the error correction terms in a system of equations used to test for both short-run and long-run multivariate Granger Causality. Long-run causality is inferred when the lagged error-correction terms are negative and statistically significant. In addition, their absolute values should be less than unity, which confirms convergence to a stable long-run stable relationship. Short-run causality is inferred by the joint significance of each of the short-run parameters included in the model.

Results in Table 6 indicate that there is long-run feedback causality between fiscal deficits and current account balance; fiscal deficits and real GDP growth; fiscal deficits and inflation; fiscal deficits and interest rates; fiscal deficits and grants; and fiscal deficits debt service. This is confirmed by the statistically significant error correction terms in each of the models in our system of equations. These results contribute to the literature that has examined the dynamic causal linkages between fiscal deficits and current account (Abbas et al., 2011); real GDP growth (Adam and Bevan, 2005; Kim et al., 2021); inflation (Lin and Chu, 2013); interest rates (Aisen and Hauner, 2013); grants (Mascagni and Timmis, 2017; Osei et al., 2005) and debt service (Maltritz and Wüste, 2015).

Table 6 Multivariate Granger causality test results

Note(s): (1) Short-run F-statistics and long-run ECT coefficients are tabulated (2) Short-run p-values are shown in parentheses (3) long-run t-statistics are shown in square brackets (4) Significance levels: *** 1 percent significance level; ** 5% significance level; * 10% significance level

Source(s): Own elaborat

Short-run Granger causality dynamics indicate mixed results. Results indicate that there is bi-directional short-run causality between fiscal deficits and GDP growth. Further, results indicate no short-run causality between fiscal deficits and inflation; no short-run causality between fiscal deficits and current account; no short-run causality between fiscal deficits and interest rates; two-way short-run causality between fiscal deficits and grants; and no short-run causality between fiscal deficits and debt service. Table 7 provides a summary of the direction of causality from the multivariate panel Granger causality tests.

Table 7 Direction of short- and long-run causality

Note(s): Causality relationships: → denotes causality in indicated direction; ≠ denotes absence of causality

Source(s): Own elaboration

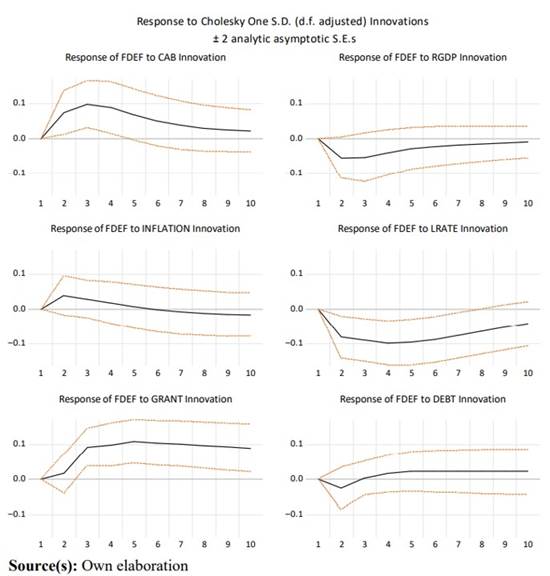

Impulse response functions

Results from the impulse response functions are qualitatively similar to those from the multivariate Granger causality analysis (see Figure 1). The effect of the current account balance on the fiscal deficit is positive and statistically significant. A one standard deviation shock in the natural logarithm of the current account increases the fiscal balance, with this effect reaching its peak in the third period (year) before becoming insignificant after the fourth year. This finding is consistent with literature showing the positive association between fiscal deficits and current account balance (Kumhof and Laxton, 2013; Kim and Roubini, 2008).

Results further show that the effect of a positive GDP growth shock on fiscal deficits is negative, with this effect reaching its peak in the third period (year) before turning insignificant in the fourth year. The divergent relationship between these two variables indicates that fiscal policy is countercyclical. This finding is contrary to the dominant literature showing that fiscal policy tends to be pro-cyclical in developing countries (Carmignani, 2010; Kassouri and Altıntaş, 2021). However, the findings of this study are consistent with Thornton (2007) who showed that South African fiscal policy is counter-cyclical.

Results further show that the effect of a positive inflation shock is positive and statistically significant. Specifically, the effect of inflation reaches its peak in the second year and thereafter dies out and becomes insignificant by the third year. These results are consistent with Lis and Nickel (2010) who showed a statistically significant and positive relationship between inflation and budget balances.

A positive shock to interest rates leads to a statistically significant reduction of the fiscal deficit. This effect reaches its maximum in the fourth year but is statistically significant until the seventh year. This implies that governments run larger budget deficits in response to lower interest rates and smaller deficits in response to higher interest rates. These results are consistent among others, Uwilingiye and Gupta (2009), who showed similar effects using South African time series data. In addition, results show that grants have a positive and persistent effect on fiscal deficits. However, the impact of debt service on budget balances is modest and insignificant.

Discussion

The EAC member states aspire to deepen economic integration, with a policy commitment to achieving convergence on key macroeconomic indicators. Regarding fiscal policy, the target is to achieve a deficit of about 3% of GDP. However, budget deficits have been rising over the past years raising concerns over increasing debt vulnerabilities. These fiscal vulnerabilities have been exacerbated by the ongoing COVID-19 shock and the weakened global outlook. While the fiscal policy is expected to play a critical role for COVID-19 economic recovery, it will play an even more important role in dealing with country-specific shocks as the countries deepen regional integration and prepare to ascend to a monetary union in the medium term. This study provided a better understanding of the dynamic linkages among fiscal deficits and key macroeconomic variables among EAC member countries.

The results of this study have significant social and practical implications. First, the dynamic relationships between fiscal policy and macroeconomic variables have social implications for welfare, equitable growth and the distribution of resources. Second, findings provide novel insights into fiscal policy determinants and causality dynamics considering the EAC's aspirations to achieve macroeconomic convergence targets. Finally, policymakers may find these results useful given the role fiscal policy is expected to play in supporting economic recovery in the wake of the COVID-19 crisis. Future research may consider examining the cyclicality of fiscal policy while differentiating between the revenue and expenditure components.

Conclusions

This study investigated the dynamic causality linkages among fiscal deficits and selected macroeconomic indicators in East Africa. Specifically, the paper considered the effects of real GDP growth, interest rates, grants, inflation, current account balances and debt service requirements. After deriving testable hypotheses from a simple analytical framework, the econometric analysis used two separate but complementary methodological approaches: (1) panel error correction-based Granger causality tests and (2) panel impulse response functions.

Results confirm that there is long-run feedback causality between fiscal deficits and each one of the explanatory variables included in the study. Short-run Granger causality dynamics show that there is a two-way short-run causality between fiscal deficits and GDP growth. Further, results indicate no short-run causality running from fiscal deficits to inflation; no short-run causality between fiscal deficits and current account; no short-run causality between fiscal deficits and interest rates; two-way short-run causality between fiscal deficits and grants; and no short-run causality between fiscal deficits and debt service.

Impulse response function results are qualitatively similar to Granger causality test results, confirming the robustness of our findings. Specifically, impulse response functions show positive and significant short-run impacts of current account balance, inflation and interest rates; negative impacts short-run of real GDP growth and lending rates; and insignificant short-run effects of debt service.

In order to maintain fiscal sustainability in the wake of increasing global and internal shocks, EAC countries should implement policies to spur real GDP growth, maintain macroeconomic stability with low inflation and external sector sustainability. Further, in the context of diminished fiscal space, the authorities should prioritize growth-enhancing budget-neutral reallocation of expenditures, reliance on external grants and concessional lending, and avoid inflationary financing of public deficits.