Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Enviar este artigo por email

Enviar este artigo por email Citado por SciELO

Citado por SciELO  Similares em

SciELO

Similares em

SciELO

Permalink

Permalink

INTRODUCTION

One of global society’s greatest challenges is implementing the 2030 Agenda proposed by the United Nations (UN), which aims to achieve 17 Sustainable Development Goals (SDGs) (United Nations, 2015). An ambitious response from the international community, the Agenda is aimed at changing the current style of development and building peaceful, fairer, more supportive, and inclusive societies where rights, the planet, and its natural resources are protected, thus demanding political actions at the national, regional, and international level (Comisión Económica para América Latina y el Caribe, 2018, cited in Retamal-Ferrada, 2020, p. 68). It is a unique global project that promotes the greatest collective agreement in view of a common goal (Garro, 2019) and will need “deep transformations in every country that require complementary actions by governments, civil society, science, and business” (Sachs et al., 2019, p. 1). In Latin America and the Caribbean, the follow-up and review of the implementation of the 2030 Agenda were conducted through a regional mechanism called “Forum of the Countries of Latin America and the Caribbean on Sustainable Development.” Five forums have been held so far, with the last one taking place in Costa Rica in 2022.

The implementation of this multi-stakeholder agenda requires the participation of all sectors of society (Kunsch, 2022; Naciones Unidas, 2018). Companies can play a meaningful role in advancing the SDGs by integrating them into their strategies and operations to help provide new solutions to the global challenges of sustainable development (United Nations Global Compact, n.d.) and “by connecting business strategies with the SDGs, developing business-led solutions, and enhancing corporate sustainability” (Adams et al., 2020, p. 4). However, measures must be adopted to ensure private initiatives produce real changes and reduce the risk of greenwashing in the marketing and public relations practices of companies (Comisión Económica para América Latina y el Caribe, 2022, p. 126).

One of the main instruments that can reflect the commitment from the business sector is a sustainability report that details both the positive and negative impacts on the pillars of sustainable development such as the case of the COVID-19 pandemic, which posed significant challenges in the continuity and implementation of new actions related to the SDGs.

The KPMG’s biennial Survey of Sustainability Reporting, whose purpose is to examine trends in sustainability reporting around the world, shows that the reporting rate of the top 100 companies has evolved from 12% in 1993 to 96% in 2020 (Threlfall et al., 2020; KPMG, 2022). On the one hand, this can be explained by the increased recognition of the link between sustainability and financial performance (Knox, 2020), the complex reality in which businesses are operating nowadays (Llanos-Herrera & Andrade-Valbuena, 2022), the dialogue on sustainability (Semenova, 2023), and the need to report on economic, social, and environmental issues (Beyne et al., 2021; Whittingham et al., 2022). On the other, interest groups exert increasing pressure on organizations and often punish irresponsible behavior (Nason, Bacq, & Gras, 2017). Consequently, both types of audit (Boiral et al., 2019; Abeysekera, 2022)-the use of comparable reports (e.g., Global Reporting Initiative, GRI)-have become tools for companies to communicate their activities transparently.

In Latin America, compared to other regions such as the European Union, sustainability reports remain, for the most part, voluntary with the exception of multinational corporations that operate in different jurisdictions where reporting may be mandatory or is a requirement from shareholders or corporate clients. Another key factor in sustainability reporting is the industry to which companies belong, since strategic sectors-including banking and finance, energy, and food and beverage-are key drivers in the functioning and economic progress of a country (Acevedo et al., 2019; Hengst et al., 2020).

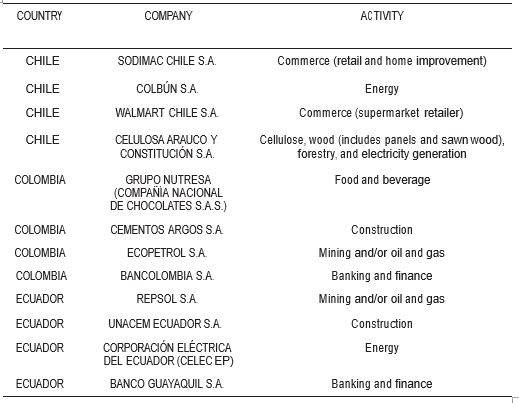

Within this framework, the present study examined the 2021 sustainability reports issued by 12 large companies from Ecuador, Colombia, and Chile in strategic sectors such as energy, mining, oil and gas, construction, banking, and food and beverage. The reports, which were downloaded from the companies’ websites, were analyzed to shed light on the actions carried out by various business sectors in relation to each of the SDGs.

The criterion for studying large companies that have higher sustainability performance follows the reasoning that they have the potential to influence sustainability trends and practices, and have the resources to do so (Durán et al., 2021b; Herrera, 2022; Martínez-Ferrero & García-Sánchez, 2017; Matus, 2018; Rosati & Faría, 2019a; Ruiz-Mora, 2012; Whittingham et al., 2022; Valenzuela et al. 2015; Villegas et al., 2022). Therefore, this study may have practical implications for managers, investors, and decision-makers tasked with developing country-specific strategies, investment initiatives, and policies to support the reporting and implementation of the SDGs (Global Reporting Initiative, 2022; United Nations Global Compact, n.d.). It may also aid communication managers in defining strategies and formats for disseminating progress in order to achieve the respective SDGs and contribute to the curriculum of different academic programs, thus strengthening the focus on sustainable development in future professionals’ careers.

Sustainability Reporting

Sustainability reporting can be defined as “an organization’s practice of reporting publicly on its economic, environmental, and/or social impacts” (Global Reporting Initiative, 2018). According to Herrera et al. (2013), reports, in addition to serving as a tool for companies to demonstrate how their corporate actions satisfy the social and environmental expectations of their main stakeholders, are a strategic instrument for measuring reputational risk. Sierra-García et al. (2018) point out that “a growing number of organizations are publishing information revealing the impact made by their activities on the environment, corporate governance, society, and human rights” (p. 1). Sustainability reports also play a key role in fostering trust, which is the basis of social legitimacy (Baviera-Puig et al., 2014), and helping organizations “in planning, implementing, measuring, and communicating their SDG efforts” (Rosati & Faría, 2019b, p. 1). The publication of sustainability reports can also be seen as a response to stakeholder pressure by communicating the company’s aspirations and progress in different areas (Bebbington & Unerman, 2018; Cho & Patten, 2007; Reynolds & Yuthas, 2008; Kazemikhasragh et al., 2021).

Among the various academic research works addressing the SDGs, it is worth highlighting Lee and Zhou (2022), who conducted a Systematic Literature Network Analysis (SLNA) using 237 publications from 2015 to 2021. Through a keyword analysis, the researchers collected an overview of the trends in SDG studies in business and management and classified them in five clusters: technology and innovation, education and human resource management, CSR and firm performance, supply chains and governance, and business strategies. A systematic literature review of 266 articles published by business scholars between 2012 and 2019 carried out by Pizzi et al. (2020) showed four significant themes of research regarding the fulfillment of the SDGs: technological innovation, firms’ contributions in developing countries, non-financial reporting, and education.

Farisyi et al. (2022), who performed a systematic literature review of 24 articles in Elsevier (Scopus), concluded that research on sustainability reporting currently focuses on nine variables: “firm size, profitability, financial leverage, corporate governance structure, ownership structure, firm age, industrial sector, corporate posture, and board qualification and experience” (p. 1). On the other hand, Grueso-Gala and Camisón (2022) gathered 3,113 articles from the Web of Science (WoS) Core Collection published between 1970 and 2019 to construct an updated state of the art. The authors identify and describe “a total of six research lines in the literature: determinants, essence, reports, integrated reporting, environment, and consequences of reporting” (p. 188).

Whittingham et al. (2022) conducted a computer-assisted text analysis of the language of sustainability reports of 164 top-performing large organizations according to the RobecoSAM Corporate Sustainability Assessment and in line with the Dow Jones Sustainability Index (DJSI) criteria to research how the SDGs affected sustainability reporting. The findings show that when comparing the companies’ sustainability reporting before and after 2015, there has been an increasing trend to report progress on some SDGs, while others may be lagging; therefore, direct political support and/or creative approaches to partnerships are needed.

Carrillo-Punina and Galarza-Torres (2022) presented a review of the sustainability reports published from 2012 to 2020 by different companies from Argentina, Bolivia, Brazil, Chile, Colombia, Ecuador, Paraguay, Peru, Uruguay, and Venezuela using the GRI methodology. The findings showed that the sectors with the highest number of publications following the GRI guidelines were the financial, energy, mining, construction, and food and beverage sectors. Similarly, the authors identified a direct and strong correlation between the gross domestic product (GDP) and the number of GRI reports. That is, if the GDP increases, GRI sustainability reports increase and if the GDP decreases, the number of reports also decreases.

In summary, the studies that address sustainability reports account for a constantly growing field of research reflected in a large number of articles stored in various data-bases as well as special editions in academic journals (e.g., Transnational Corporations, Academy of Management Discoveries, Corporate Governance, Organicom). Likewise, the topic has been discussed at various conferences organized by academic associations; however, this growing productivity poses a challenge for future research to further detail how these studies may be more practically linked to organizations and the State to achieve better results and a greater volume of production. In this context, the present study aimed to answer the following research questions:

METHODOLOGY

Sample Selection

Assuming that large companies with high revenues have sufficient resources to invest in social responsibility and communications management, the authors referred to a group of 100 companies in Chile, Ecuador, and Colombia that took part in a previous 2021 quantitative study on the level of development of social responsibility and communication, as well as the convergence rate among these disciplines (Durán et al., 2021a). This original list of 100 companies was collected from the top companies ranked by revenue and published by journals such as Ekos (Ecuador), América Economía (Chile), and Dinero (Colombia).

While other studies on sustainability reporting have mainly focused on general activities carried out by companies in the field of sustainability, the present study specifically focuses on actions that aim to achieve the SDGs. The following inclusion criteria were considered: the first one claims that the company must have had published a 2021 country-specific sustainability report in Spanish in a publicly available, downloadable format; the second one states that the report had to follow the GRI standards in terms of content (impacts, material issues, due diligence, and stakeholders) with clear details as to how the company’s actions contributed toward the SDGs in each specific country. As found by Carrillo-Punina and Galarza-Torres (2022), most companies that report their sustainability and business results based on the GRI standards come from the energy, food and beverage, and financial sectors. Thus, the third criteria was to belong to one of these strategic sectors.

An initial review of the 100 companies showed that 55% had published a 2021 sustainability report, which was readily available on their website. A second review found that 15% of the reports followed the GRI standards and included detailed explanations of how the company’s actions strived to achieve the SDGs. Moreover, some reports followed the GRI standards but did not mention the SDGs, while some multinational companies issued reports that met both the GRI and SDG criteria but were mainly focused on international operations with little or no explanation of how the SDGs were achieved through specific country initiatives. Therefore, companies with these types of reports were eliminated. In total, 12 companies whose reports met all the criteria were included in the study sample (see Table 1).

Methodological Approach

Based on the different designs proposed by Hernández-Sampieri and Mendoza (2008, as cited in Hernández et al., 2014), the present research followed an explanatory sequential design (DEXPLIX). Thus, quantitative (identification and number of SDGs in sustainability reports) and qualitative (contributions/actions concerning the main SDGs among the 12 companies under study) data were collected and analyzed through document analysis in the first and second stages, respectively. It should be noted that the second stage was built based on the results of the first one, and the findings in both stages were integrated into the interpretation and preparation of the study report (Hernández et al., 2014).

The technique used was content analysis (Andréu, 2002; Bardin, 1996; Krippendorff, 1990), including “presence/absence” as an indicator according to the study variable; i.e., the identification of the SDGs and the contribution or action referred to. In addition to the content analysis, the results were extracted and coded according to the specific contribution identified by either the SDG or the detailed target.

RESULTS

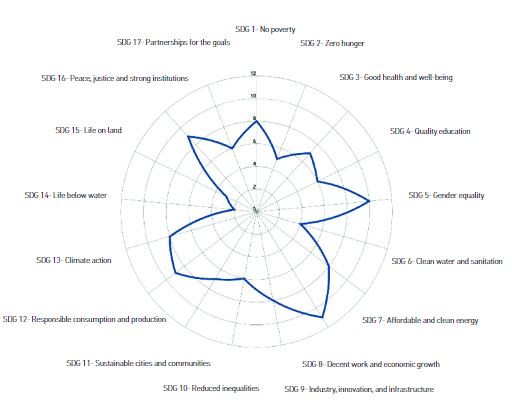

The selected companies carried out actions linked to several of the SDGs; some focused on a higher number of goals while others prioritized those considered relevant to the organization and its stakeholders (Figure 1). The only company to implement actions aligned with all 17 SDGs was Cementos Argos S. A. in Colombia, while the rest opted for compliance with three and five SDGs. The most recurring goal was “decent work and economic growth” (SDG 8), followed by “gender equality” (SDG 5). The least reported goals were “life below water” (SDG 14) and “clean water and sanitation” (SDG 6).

Most Commonly Referenced SDGs in Sustainability Reports

According to Figure 2, the three most prevalent SDGs are “decent work and economic growth” (SDG 8, 11 companies), “gender equality” (SDG 5, 10 companies), and “responsible consumption and production” (SDG 12, 9 companies).

SDGs such as “peace, justice and strong institutions” (SDG 16) are also mentioned in the reports, albeit less frequently, as is the search for “no poverty” (SDG 1), “affordable and clean energy” (SDG 7), “industry, innovation and infrastructure” (SDG 9), “good health and well-being” (SDG 3), “quality education” (SDG 4), and “zero hunger” (SDG 2).

Fulfillment of SDG 1: No Poverty

Among the eight companies that mentioned their contribution to ending poverty, Bancolombia states that it develops financial inclusion initiatives, such as bringing financial services to underprivileged segments of society to generate financial well-being and improve their quality of life (Bancolombia, 2021, p. 117). This initiative is important since, as a bank, the company not only shows concern for expanding its business abroad (as part of its corporate purpose) but also ventures into new ways of creating access to the financial system for people of lower socioeconomic status.

Fulfillment of SDG 2: Zero Hunger

Walmart Chile contributes to the no hunger goal through its Rescue and Donation program, which consists in the donation of food and personal hygiene products that are not marketable but still suitable for human consumption and use to more than 400 non-profit organizations that belong to their allied group, i.e., Red de Alimentos (Food Network). In their annual report, they point out that they have directly benefited over 70 thousand people through more than 1,043 tons of products donated throughout 2021 (Walmart Chile, 2021, p. 63).

Fulfillment of SDG 3: Good Health and Well-Being

Regarding SDG 3, Ecopetrol considers itself a relevant actor in the oil and gas industry with a commitment to the country to contribute to preserving the air quality in the surrounding areas of its operations for the well-being of citizens and the care of the environment (Ecopetrol, 2021, p. 244). Given the nature of its operations, a hydrocarbon company such as Ecopetrol must consider the health implications of its actions. Thus, the organization monitors and controls significant air pollutant emissions as well as volatile organic compounds that affect air quality.

Fulfillment of SDG 4: Quality Education

Celulosa Arauco y Constitución stands out for its contributions to SDG 4 through Fundación Arauco, which has benefited more than 5,141 teachers, 575 schools, and 101,940 children in Chile through different training programs and activities. The company’s actions in this regard are noteworthy, since they belong to one of the most important SDGs within the Latin American region, where levels of quality education are low according to test reports associated with education around the world. In its annual report, the company states its conviction that education has a transformative power in society and acts as the main driver of development (Celulosa Arauco y Constitución, 2021, p. 161), thus ratifying the company’s position regarding the value projected by this SDG in the region.

Fulfillment of SDG 5: Gender Equality

In keeping with social trends, the promotion and strengthening of gender equality, identified as SDG 5, was highly prevalent in the studied annual reports. Out of the 12 companies, 10 mentioned it in their reports and provided details on the initiatives toward its achievement during 2021.

Grupo Nutresa, in addition to reporting initiatives aimed at maintaining employment and supporting the professional growth of its employees, states that it has a 35% participation rate of women in different positions. Moreover, the company claims that it continues hiring people with disabilities and victims of the conflict in Colombia (Grupo Nutresa, 2021, p. 33).

Walmart Chile rolls out what it calls the “Diversity, Equity, and Inclusion (DEI) Week,” which aims to highlight its five pillars of work: Gender Equality, People with Disabilities, Interculturality, Generations, and Sexual Diversity. They worked collaboratively with 25 companies and organizations to launch the “Intercompany Diversity Week,” open to the general public, to spread knowledge about these pillars. Through a platform, they held live talks, broadcast e-learning pills, and digital resources (Walmart Chile, 2021, p. 29). Walmart’s work materialized its efforts by widely disseminating its gender equality actions through the use of digital platforms.

Bancolombia launched a strategy called “Me la Creo” (I Believe in It), aimed at gender equality, which includes female employees, suppliers, investors, customers, and the community in general. At the same time, its sustainability report indicates the progress made in the formalization and structuring of a diversity, equity, and inclusion strategy, integrating the Bancolombia Diversa project (gender identity and sexual orientation) under the same focus and updating its governance model (Bancolombia, 2021, p. 117).

Fulfillment of SDG 7: Affordable and Clean Energy

Although CELEC EP reports compliance with the fewest number of SDGs (three), its contribution in terms of affordable and clean energy is significant, as evidenced by the figures in its reports. As a public power generation company, it is responsible for generating 87% of all hydroelectric power produced in Ecuador. The company claims that these data show its contribution to the reduction of greenhouse gasses, as it has progressively displaced the use of fuels in favor of water resources for power generation (Corporación Eléctrica del Ecuador, 2021, p. 127).

Fulfillment of SDG 8: Decent Work and Economic Growth

Despite the situation caused by the pandemic, all companies report leading actions toward sustained, inclusive, and sustainable economic growth; full and productive employment; and decent work for all. In the case of Banco Guayaquil, its report explicitly states four of the 10 goals contained in SDG 8 (8.2, 8.3, 8.5, 8.10). Its contributions are mainly related to credit allocation to support entrepreneurs and the recovery of small- and medium-sized enterprises, especially those affected by COVID-19, through social cash transfers at the end of 2020. They also describe themselves as direct job creators in their teams and offer permanent contracts (Banco Guayaquil, 2021, p. 93).

In the cases of Banco Guayaquil and Grupo Nutresa, it is evident that both companies manage multiple work fronts with a wide variety of initiatives based on the conditions of the company, the region, and the country to which they belong. In contrast, Colbún declares the benefits it grants to different groups of stakeholders: a minimum wage of CLP 500,000 (approximately USD 583) for permanent contractors, entrepreneurship centers, gender equity plans, initiatives for the inclusion of people with disabilities, and safety leadership programs (Colbún, 2021, p. 55).

Fulfillment of SDG 9: Industry, Innovation, and Infrastructure

Grupo Bancolombia declares that it contributes to the technological reconversion of industries, helping them to be more productive and efficient. Likewise, they promote sustainable industrialization through a sustainable line of credit for companies committed to increasing their positive impacts on the environment and society (Bancolombia, 2021, p. 118).

In UNACEM Ecuador’s annual report, SDG 9 stands out by the creation of a platform called “Simbiosis Industrial EC” (Industrial Symbiosis EC) with Consorcio Ecuatoriano para la Responsabilidad Social (CERES, Ecuadorian Consortium for Social Responsibility). In this way, its contribution is related to investment in research for the development of products that contribute to reliable, sustainable, resilient, and quality infrastructures (UNACEM Ecuador, 2021, p. 18).

Fulfillment of SDG 12: Responsible Consumption and Production

SDG 12 was mentioned by nine of the 12 companies in relation to their scope, actions, as well as ecological and sustainable aspects. In this area, it was found that many of the companies focus on the production of their products and services, giving priority to internal processes; however, they are also interested in the communication with external stakeholders, management of responsible consumption of resources, and especially responsible consumption of products by users and customers.

In its sustainability report, Sodimac Chile points outs that it leads a number of initiatives to protect the planet, including its almost 4,700 sustainable products and services; the decision not to deliver single-use bags in its stores since the beginning of 2018; its “Red Nacional de Puntos Limpios” (National Network of Clean Points); the “Haciendo ECO” (Creating an Echo) campaigns; its special catalogs; the “Hágalo Usted Mismo” (Do It Yourself) e-learning pills to promote recycling and reuse of unused items; the advances in the use of clean energy with solar panels in its facilities; the increasing incorporation of electromobility in operations; and the eco-efficiency measures in homes. In addition, the company, which in 2018 joined the Ellen MacArthur Foundation’s Circular Economy 100 (CE100) and adhered to Fundación Chile’s “Pacto Chileno por los Plásticos” (Chilean Pact for Plastics), together with its suppliers, proposed to double the offering of eco- sustainable items and services in its stores in 2019, and that 100% of the containers and packaging of the products it sells be recyclable, starting with its own brands (Sodimac Chile, 2021, p. 30).

Fulfillment of SDG 13: Climate Action

Cementos Argos’s sustainability report shows contributions to SDG 13 by acknowledging that, as an industry with a2 emissions footprint, it remains commited to CO delivering carbon neutral concrete through the 2050 Climate Ambition Plan (Argos, 2021, p. 7). Since climate actions are complex in the construction industry, the company states its commitment to advance its research processes, in addition to taking measures to mitigate the effects of its products.

CONCLUSIONS

The SDGs have become a tool for private sector companies and public sector organizations to be clear about their contributions toward the fulfillment of the goals established in the 2030 Agenda.

Based on the theoretical framework, it is concluded that the sustainability reports of companies show a significant increase in research and include the actions they take under the SDG guidelines. Companies are more interested not only in publishing their reports- which is an important contribution in terms of sustainability-but also in complying with unified criteria that follow the SDGs. This makes it possible to speak a common language about the SDGs to which the companies adhere and the specific actions deemed urgent for their stakeholders. The companies selected for this study have sustainability reports and strategic actions aimed at meeting at least three SDGs.

Among the previously referenced studies, the one by Carrillo-Punina and Galarza- Torres (2022) stands out as it contains complementary and divergent elements with respect to this study. Their analysis covers sustainability reports of Latin American companies from a social responsibility perspective without focusing on the SDGs. The authors also use the GRI reporting methodology as a starting point and note that the sectors with the highest production of sustainability reports are energy, finance, and food and beverage. Although Carrillo-Punina and Galarza-Torres (2022) use a quantitative approach, they focus on the companies with more publications and the sectors and countries with the largest number of companies reporting their sustainability activities. Therefore, the present study complements previous research because it broadens the focus on sustainability efforts in relation to the SDGs.

Given the characteristics and conditions of the Latin American region, the three countries’ reports share considerable similarities. In response to the first research question, the most prevalent SDGs are “decent work and economic growth,” “gender equality,” and “responsible consumption and production.” The overlaps between the researched companies regarding these goals are evidence of how they are taking the lead on issues deemed a priority for the community in general and for specific stakeholders.

In response to the second research question, each company’s efforts toward the development of the SDGs, regardless of their business activities or economic situation, is clearly linked to eliminating poverty and hunger, improving working conditions, and working toward gender equality: issues that require a significant amount of work in Ecuador, Colombia, and Chile. Companies seek to solve not only problems posed by their business activities-such as the case of energy and cement companies-but also other issues of interest to their stakeholders.

In addition to focusing on “gender equality” and “decent work and economic growth,” there is also evidence of concern for the fulfillment of other important SDGs. For example, a company in the energy sector is not only involved in affordable and clean energy actions; it also develops strategies and activities in favor of other aspects such as ending poverty, enhancing quality education, or achieving gender equality, to give just three examples.

Although the results of this analysis are specific to the sample of 12 large companies from three South American countries, which may be a limitation, the information is a reference to the existing dynamics in terms of sustainability reports and their relationship with the SDGs. The fact that these large corporations are aligning their social responsibility actions with the 2030 Agenda shows a positive and optimistic trend regarding the initiatives undertaken by multilateral organizations with the support of the public and private sectors, which has facilitated the creation of an institutional framework.

Certainly, the implementation and communication of the SDGs met by the companies studied through their sustainability reports enable verifying the alignment with the global goals of their respective countries’ institutional frameworks. At the same time, they make it possible to highlight the contributions made by the companies in relation to the 5 Ps of sustainable development: people, planet, prosperity, peace, and partnerships.

It can also be claimed that the importance given to the communication of sustainability reports has been understated. In some cases, companies carry out isolated sustainability actions that are not disclosed to their audiences. Today, more organizations have come to understand the importance of managing sustainability reports, applying methodologies such as the GRI, and sharing the results of these actions. At present, it is evident that company managers invest time and money in communicating initiatives to fulfill the SDGs. At the same time, they highlight their contributions in the cover letters of the reports addressed to their stakeholders.

RECOMMENDATIONS

Companies may roll out activities that aim to meet the 17 SDGs, but they should focus on those deemed most important and valued by their stakeholders and according to their ability to implement them.

Given that “decent work and economic growth” and “gender equality” are highly prevalent in the sustainability efforts of the companies in the three analyzed countries, it would be appropriate for both public and private organizations to develop actions that favor their stakeholders on this matter.

Companies should be aware that SDG implementation should not only address aspects related to their own business but also achieve a diversity that impacts on more communities and stakeholders. Companies should also join forces and develop collaborative projects with public entities, nonprofit organizations (NGOs), and third-sector organizations, such as foundations and nonprofits, to become more familiar with the needs of different communities.

Latin American countries will always have problems directly related to regional development. Therefore, actions that favor education, ending poverty, and the reduction of inequalities will always be welcome and will allow progress of society. Likewise, although the countries analyzed have ample biodiversity and favorable ecosystems, it never hurts to have organizations working on sustainability to mitigate the effects of planetary limits.

As a final recommendation, companies should properly manage their resources and continue to grow in terms of research and development of sustainable products and services that better meet the needs of their communities.

Recommendations for Further Research

Finally, in terms of future lines of research and in a post-pandemic context, it may be of interest, on the one hand, to understand how SMEs and universities are incorporating the SDGs in their activities. On the other hand, delving deeper into the communication tools and channels used to disseminate these actions would also be a useful object of analysis, bearing in mind that communication can help ensure a greater understanding of the sustainable model and raise society’s awareness of the actions of the organizations that surround them, their impacts and their work aimed at the continuous improvement of business practices. It would also be desirable to extend the analysis of sustainability reports focused on the SDGs to other countries in the region. This can be done through a qualitative approach to better understand the needs of the communities that will ultimately benefit from companies’ product and service sustainability programs in the future.