Servicios Personalizados

Revista

Articulo

Inglés (pdf)

Inglés (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Enviar articulo por email

Enviar articulo por emailIndicadores

-

Citado por SciELO

Citado por SciELO

Links relacionados

-

Similares en

SciELO

Similares en

SciELO

Compartir

Permalink

PermalinkJournal of Economics, Finance and Administrative Science

versión impresa ISSN 2077-1886

Journal of Economics, Finance and Administrative Science v.15 n.28 Lima jun. 2010

ADR Effects on Domestic Latin American Financial Market

Los efectos adr en los mercados domésticos financieros de Latinoamérica

Alfredo Mendiola1

1. Professor Alfredo Mendiola is Ph. D. in Management Finances from Cornell University, USA. He also holds a MBA from the University of Toronto, Canada; a MBA from Esan Business School, Peru. He is a B.of Sc. in Systems Engineer from the Universidad Nacional de Ingeniería del Peru.

Abstract

The purpose of this paper is to revisit and extend previous research work that examines the ADR-listing effects on the trading process of all the domestically-listed stocks in the main Latin American exchanges. The most important result is consistent with the idea of a greater isolation (from global markets) of the singly-listed stocks in the post-cross-listing period. These results persist over the cross-listing months. As expected, the cross-listed stocks become more integrated in the post-cross listing period.

Keywords: International finance, economic integration.

Resumen

El propósito de este artículo es revisar y extender trabajos de investigación en que se examinan los efectos de emitir ADRs en el proceso de negociación de las acciones listadas en los mercados de valores latinoamericanas. El resultado más importante es consistente con la idea de un mayor aislamiento (de mercados financieros internacionales) de las acciones listadas únicamente en el mercado doméstico en el período posterior a la emisión de los ADRs. Estos resultados son persistentes en el tiempo. Como era de esperarse, las acciones sobre las que se han emitido ADRs se encuentran más integradas con mercados financieros internacionales en períodos posteriores a la emisión de este.

Palabras claves: Finanzas internacionales, integración económica.

Research has established that cross listing significantly affects the ADRs underlying share1 trading process in the domestic exchange. Examples of these effects include higher valuations and improvements in an investors appreciation of the firms information (Coffee, 1999; Reese & Weisbach, 2002; Doidge, Karolyi, & Stulz, 2003); declines in cost of capital (Errunza & Miller, 2000; Foerster & Karolyi, 1993, 1999; Domowitz, Glen, & Madhavan, 1998); positive abnormal stock returns in the pre-cross-listing period (Foerster & Karolyi, 1993, 1999; Jayaraman, Shastri, & Tandon, 1993; Viswanathan, 1996; Miller, 1999; Errunza & Miller, 2000; Kim & Singal, 2000); improvement in firm visibility and information environment (Baker, Nofsinger, & Weaver, 2002; Lang, Lins, & Miller, 2003; Bailey, Karolyi, & Salva, 2006); spillover of cross-listing effects to singly-listed stocks (Fernandes, 2003; Melvin & Valero-Tonone, 2003; Lee, 2003); a migration of trading volume (Smith & Sofianos, 1997; Pulatkonak & Sofianos, 1999; Levine & Schmukler, 2003; Domowitz, Glen, & Madhavan, 1998). The purpose of this paper is to revisit and extend previous research work that examines the ADR-listing effects on the stock returns of all domestically-listed stocks in Latin American exchanges. Initially, the analysis is done considering the singly- and cross-listed stocks separately; next, all the information of the domestically-listed stocks is pooled to determine possible differences in the trading process across the two groups of securities.

This approach builds on previous research work2 and, additionally, takes into consideration three important factors affecting ADR listings. First, including only Latin American stocks ensures that the time zone differences across local and US exchanges are, at most, two hours.3 Second, to facilitate the identification of spillovers4, the examination of ADR-listing effects is done separately on singly- and cross-listed stocks; in a subsequent step, all the information (from the singly- and cross-listed stocks) is pooled to determine whether differences exist across these two groups of securities. Third, Heckmans (1979) procedure is used to control for the differences in the characteristics of the firms with cross- and singly-listed stocks; without this procedure, a non random sample selection occurs given that the behavior of cross- and singly-listed stocks is examined separately.

The main results of this paper are as follows: ADR-listing effects on the domestically-listed stocks are significant and affect singly- and cross-listed stocks in different ways. As expected, ADR-listing results in an increase in the importance of the world exchange index in explaining the behavior of cross-listed shares. However, for the singly-listed shares, ADR-listing induces a significant increase in the importance of the domestic exchange variables to explain the trading behavior of this group of stocks. I interpret this finding as an increase in the isolation (from international markets) of singly-listed shares in the post-cross-listing period.

This paper is organized as follows: The first section includes a summary of the sources and characteristics of the data used for empirical tests. Section two presents a discussion of Heckmans technique and its empirical implementation to determine the Inverse Mills Ratio (probability of cross-listing) for each stock. The behavior of the stock returns is included in the third section.

DATA

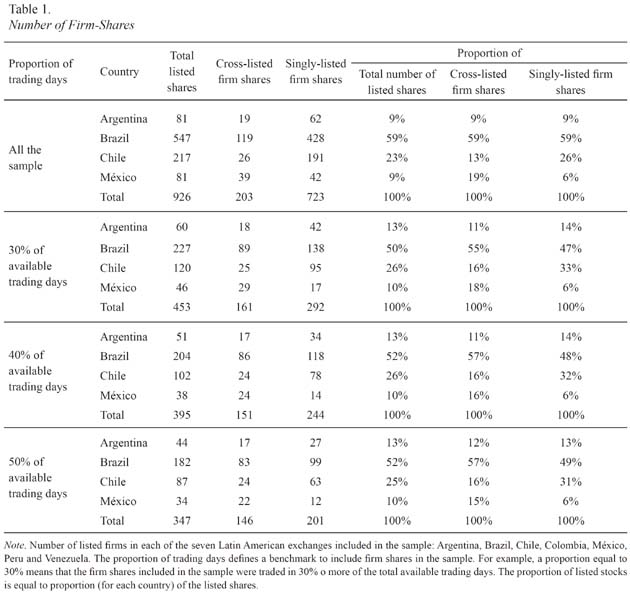

The information collected includes firm and exchange related information from four Latin American countries: Argentina, Brazil, Chile and Mexico.5 The period analyzed extends from January 1, 1992 to December 31, 20026. The total number of firm / shares considered in the sample is 926, of which 203 (22%) have cross-listed securities (See Table 1).

To minimize the possibility of a non-synchronous trading bias, I exclude the securities that trade in less than 30% of the available trading days.7 As Campbell, Lo and MacKinlay (1997) indicate the non-synchronous trading or non-trading effect arises when time series, usually asset prices, are taken to be recorded at time intervals of one length when in fact they are recorded at time intervals of other, possibly irregular, lengths... (p. 84). For example, this problem may occur if it is assumed that daily closing prices are recorded at the end of the trading day. As Campbell et al. specifically indicate, this effect may introduce biases in the moments and co-moments of asset returns such as their means, variances, betas and autocorrelations (p. 84). Scholes and Williams (1977) examine this problem and show that for actively traded stocks, any adjustment to control for non-trading effects are generally small and unimportant. Consequently, limiting the sample to include only the most liquid stocks minimizes the possibility of biasing the results due to non-trading effects, improving the quality of the empirical results.8

If we exclude the securities traded in less than 30% of the available trading days, the total number of firm-shares drops from 926 to 453 (51% reduction in the sample size). Furthermore, with this control the number of singly-listed firm-shares included in the sample decreases from 723 to 292 (60% reduction); for the cross-listed firm-shares the sample size decreases from 203 to 161 (21% reduction). When trading in, more than 40% and 50% of the possible days is considered as a benchmark, the total sample size is reduced to 395 and 347 firm-shares, respectively. The proportion of singly- and cross-listed firm-shares excluded from the sample is in line with the previously indicated information (see Table 1).

Daily stock information has been collected from DataStream and includes closing prices, traded volume, and market capitalization. This information was collected in the countrys domestic currency and then converted to US Dollars to facilitate cross-sectional analysis9. The firms accounting information, necessary for the implementation of Heckmans procedure, was obtained from the WorldScope database available through DataStream. All information has been collected in home country currency. Exchange related information has also been collected from DataStream and includes the domestic stock exchange index and the MSCI World Stock exchange index. To facilitate the cross-sectional analysis across exchanges, all the information has been converted to US dollars.

HECKMAN S PROCEDURE TO CONTROL FOR SAMPLE SELECTION BIASES

The firms that cross list stocks are believed to be the largest and most successful organizations in their home countries. As such, examining the behavior of the singly- and cross-listed stocks separately induces a sample selection bias. To control for this possibility, the implement Heckmans procedure has been implemented.10

This sample selection problem can be summarized as follows11: Consider a random sample of I observations. For each observation i the following equations can be defined:

where Xji is a (1 x Kj) vector of regressors and βj is a (Kj x 1) vector of parameters. Suppose that data is available for Y1i if Y2i ≥ 0; if Y2i = 0 then there are no observations for Y1i. The general idea is to develop a two-stage estimator to overcome any possible bias related to the non random sample selection due to limitations in the information on Y1i. In this dissertation, Y2i = 0 (1) if the stock is singly- (cross-) listed.

Heckmans procedure is implemented as follows:

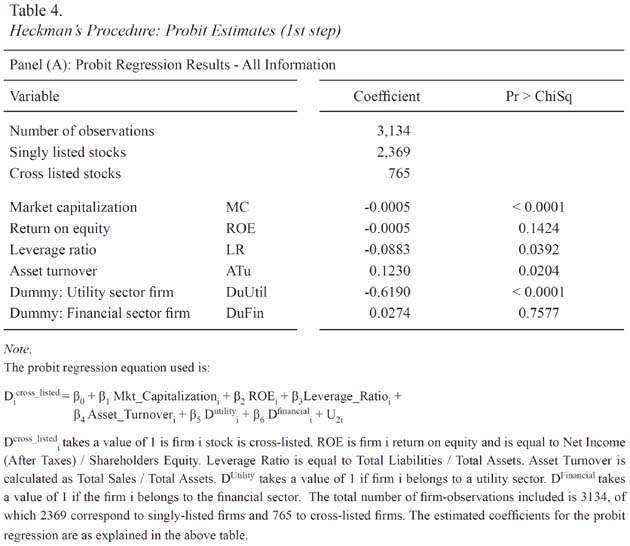

1. Use the full sample of listed stocks to estimate a probit regression to determine the probability that Y2i ≥ 0 (the stock is cross-listed or singly-listed). The independent variables included in this regression represent the general characteristics of all the domestically-listed firms such as market capitalization, leverage ratio, asset turnover and return on equity.

2. Following Heckmans notation, define φ() as the density function and Φ() as the distribution function of a standard normal variable. Using the coefficients estimated in the probit regression and assuming that h(U1i,U2i) (error-terms of equations 1 and 2) is bivariate normal, the following parameters (for each of the domestically-listed stock) can be estimated:

where λi is known as the inverse of Mills ratio. This ratio is a correction term that is used to control for the bias that arises from the non-random sample selection. As the probability of being in the sample (i.e. cross-listed share) increases, the cumulative density function approaches one and the probability density function approaches zero, so the Inverse Mills ratio approaches zero.

3. For the estimation of equation 1 coefficients, the Inverse Mills ratio (λi) is included as one of the independent variables. Heckman demonstrates that under the previously indicated assumptions the regression estimators (coefficients of X1i and λ1 in equation 1) are consistent. Puhani (2000) conducts different Monte Carlo exploratory studies around Heckmans procedure. His results show that, in the absence of collinearity, a full information maximum likelihood estimator is preferable to the limited-information two-step method of Heckman If, however, collinearity problems prevail, subsample OLS (or the two-part model) is the most robust amongst the simple-to-calculate estimators (p. 54).

As previously indicated, Heckmans procedure is a two-stage procedure. In this sub-section, the first step is implemented (i.e. the estimation of the Inverse Mills ratio for each stock). This ratio is included as one of the independent variables in different regressions to be implemented in later sections of this chapter.

To implement step 1 probit regression, the following independent variables that characterize the domestically-listed firms (X2i in equation 2) are included:

-

Market capitalization (MC) to proxy for firms size. Larger firms are believed to be the most important in their home countries and should tend to be cross-listing targets.

-

Return on equity (ROE) as a profitability measure of a shareholders investment12. Profitable firms should tend to be cross-listing targets. Another possible argument is that firms with a low ROE cross list to force an improvement in their performance.

-

Leverage ratio (LR) to proxy for the firms financial risk13. The rationale is that a higher leverage ratio should lower cross-listing possibilities. Another possible interpretation of this factor is that highly levered firms will cross list to redefine their capital structure.

-

Asset turnover (ATu) to measure the firms operational efficiency14. The most efficient firms should tend to be cross-listing targets. Another (opposite) argument is that inefficient firms will cross-list to precipitate changes that will improve asset turnover.

-

Dummy for utility firms (Dutility). A significant proportion of the cross-listed firms correspond to this economic sector (electricity and telecommunication firms).

-

Dummy for financial sector (DFinancial). Banks are believed to be important cross-listing targets.

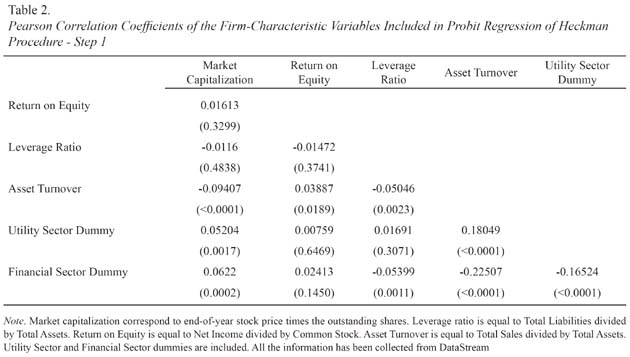

The Pearson Correlation Coefficients across the previously indicated variables are presented in Table 2. The general picture is consistent with the idea that no strong correlations are observed across these variables.

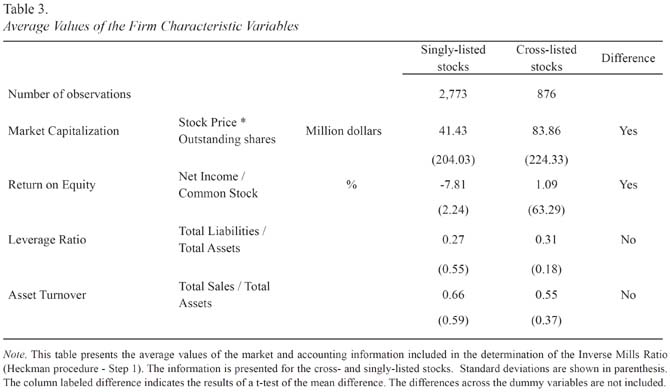

Table 3 presents the average values of the firm characteristic variables that are included in the determination of probit regression of Heckmans procedure (Step 1). The information is subdivided across singly- and cross-listed stocks. As expected, the firms with cross-listed shares are bigger and more profitable, if measured by the return of equity ratio.

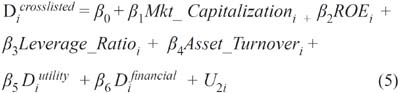

Finally, to implement Step 1 of the Heckmans procedure, the following probit regression equation is estimated:

Regarding the implementation of the Heckmans procedure two final points must be noted. Firstly, as demonstrated by Heckman, including the Inverse Mills Ratio as an independent variable in subsequent regression estimations should control for any possible differences across singly- and cross-listed stocks that may bias the results. In other words, including this ratio as one of the independent variables will control for the previously indicated differences in size and profitability across singly- and cross-listed stocks. Secondly, in the paper the implementation of Heckmans procedure is neither directed toward examining any differences in the firms with singly- and cross-listed shares nor in the characteristics of the firms that cross-list shares. Instead, this procedure is implemented to estimate a variable (Inverse Mills Ratio) that will be used to control for possible differences across the firms with singly- and cross-listed stocks.

Table 4 - Panel A reports equation (5) estimated coefficients after pooling all the information from the four exchanges included in the sample: Argentina, Brazil, Chile and México. The total number of firm-year information is 3,134, of which 765 correspond to firms with cross-listed shares. The Market Capitalization coefficient is significantly negative. The return on equity (ROE) coefficient is non-significant. The coefficients for the Leverage Ratio and Asset Turnover are significant and evidence that the firms financial risk and operational efficiency are taken into consideration to the define the possibility of ADR-listing15. The utility sector dummy coefficient (Dutility) is significant and negative. The coefficient for the financial sector dummy (DFinancial) is not significant. These results are included in equations 3 and 4 to determine the Inverse Mills Ratio of each firm.

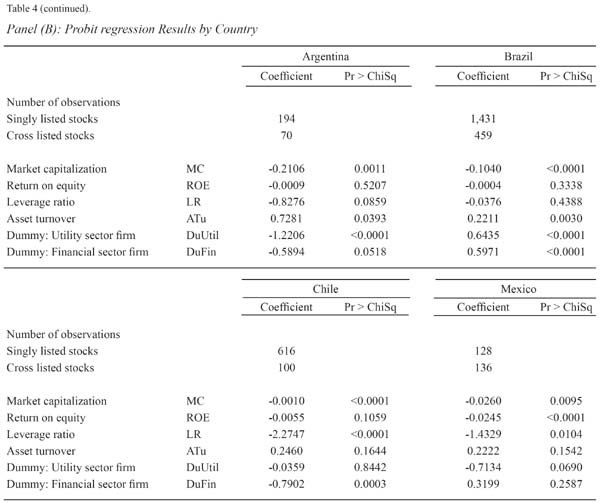

Similarly, Table 4 - Panel B reports equation (5) estimated coefficients for each of the four countries included in the sample. Even though most of these coefficients have the same sign and significance as the ones presented in Table 4 – Panel A, some differences can be appreciated. For example, for Chile and Brazil, the asset turnover and leverage ratio coefficients respectively are not statistically significant from zero.

Taking into consideration the country differences in the estimation of the probit regression (equation (5)) coefficients, Table 4 – Panel B coefficients will be used to estimate the Inverse Mills Ratio for each firm (Equations (3) and (4)). These ratios will be used in the regression analysis described in latter sections.

STOCK RETURNS

Research has established that there are significant differences in the pre- and post-cross-listing excess returns of the ADRs underlying shares. Miller (1999) reports significant cross-sectional differences across pre- and post-cross-listing ADR-stock returns; at the same time, he argues that these results are consistent with the idea that ADR-listing limits the negative effects of trading barriers, facilitates risk diversification and, consequently, reduces the investors required returns. Errunza and Miller (2000) report a significant decline in buy-and-hold ADR-stock returns across the ADRs pre- liberalization period (months -36 to -7 before cross-listing) and the post liberalization period (months +7 to +36).

Foester and Karolyi (1999) state that the reduction in the ADRs underlying share returns for the post-cross-listing period are explained by a decrease in the risk perceived by investors, as they have access to better information about the ADR issuer. These arguments are consistent with Mertons (1987) incomplete information asset pricing model, Amihud and Mendelsons (1986) liquidity analysis, and Kladec and McConnells (1994) examination of the reactions in the stock trading process to changes of trading venue.

Fernandes (2003) uses a sample of individual firms from 27 emerging markets to examine the spillover effects of the first ADR-listing. He finds a spillover effect (as predicted by Alexander et al. (1985) asset pricing model) that results in a decrease in the expected returns across all domestically-listed stocks. Melvin and Valero-Tonone (2003) report that rivals of an ADR-issuing firm that list in the local market are negatively affected by cross-listing: there is a reduction in the rival firms excess return around the announcement and listing day16.

To implement the empirical tests, when necessary, the daily stock information is summarized into weekly periods17. For each week, the last available daily price is considered to be the end-of-the-week closing price (CP). The weekly stock return (Ri,t) for stock i in week t is defined as:

To estimate weekly stock excess returns (ri,t), the US T-Bill (30 day maturity) return (Rft) is considered to be risk-free, such that:

The procedure used to calculate the end-of-the-week index returns is similar to that used for stock returns.

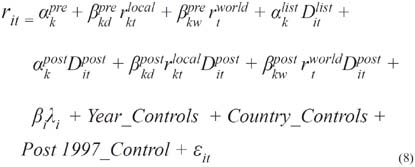

The international asset pricing model (IAPM) implemented by Foerster and Karolyi (1999) is used to determine whether there are cross-sectional differences across the pre- and post-cross-listing weekly excess returns of the singly- and cross-listed stocks.18 This model relates the excess returns on the stocks, domestic market exchange index, and world exchange index for the pre-, during and post-cross-listing weeks, such that:

where rit refers to the weekly excess returns of stock i in period t. The variables rktlocal and rtworld correspond to the weekly excess return of the kth domestic stock exchange index (where stock i is listed) in period t and the world stock exchange index, respectively. Ditlist and Ditpost are dummy variables to control for the listing and post-cross-listing periods, respectively. λi is stock i average Inverse Mills ratio, and it is included to control for any possible problem related to non-random sample selection. To control for potential country-differences and time trends, the corresponding dummy variables are included. Additionally, a post-1997 dummy variable is included to control for possible differences across the pre- and post-Asian crisis.19

As previously indicated, the examination of ADR-listing effects on singly- and cross-listed stocks is done separately for each. For the cross-listed stocks, equation (8) estimates coefficients using 24 months of stock and exchange information around the ADRs cross-listing date.20 To examine the cross-listing spillover effects on singly-listed stocks, equation (8) estimates coefficients considering 24 months of information around the first three ADR-listing days.21 The statistical significance of αkpost, αkpost, βkdpost and βkwpost coefficients is used to examine the ADR-listing effects.

To examine whether the cross-listing effects spread uniformly to the singly- and cross-listed stocks, all the information (of singly- and cross-listed stocks) is pooled to estimate the IAPM coefficients (Equation (8)). In this case, the dummy variables Ditlist and Ditpost are equal to 1 for the ADR-stocks in the cross-listing and post-cross-listing periods, respectively. Similarly, the statistical significance of αklistαkpost, αkpostαkpost, βkdpost and βkwpost will provide evidence of the existence of the previously indicated differences.

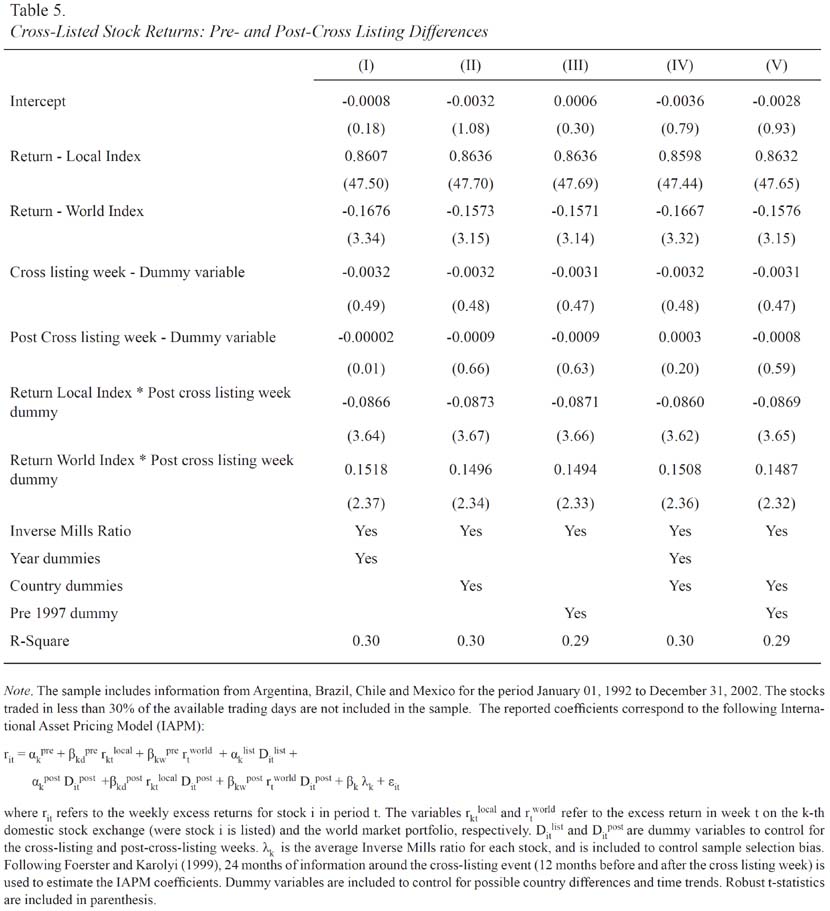

Table 5 reports the equation (8) estimated coefficients for the cross-listed stocks traded in more that 30% of the available trading days. The reported regression coefficients correspond to five different combinations of the year, country and post-1997 control variables. In all five regressions, the coefficients of the interactive terms22 are significant, have the expected sign, and are consistent with the idea that cross-listing determines an increase (decrease) in the importance of the world (domestic) stock exchange index to explain the ADRs underlying stock returns in the post-cross-listing period23.

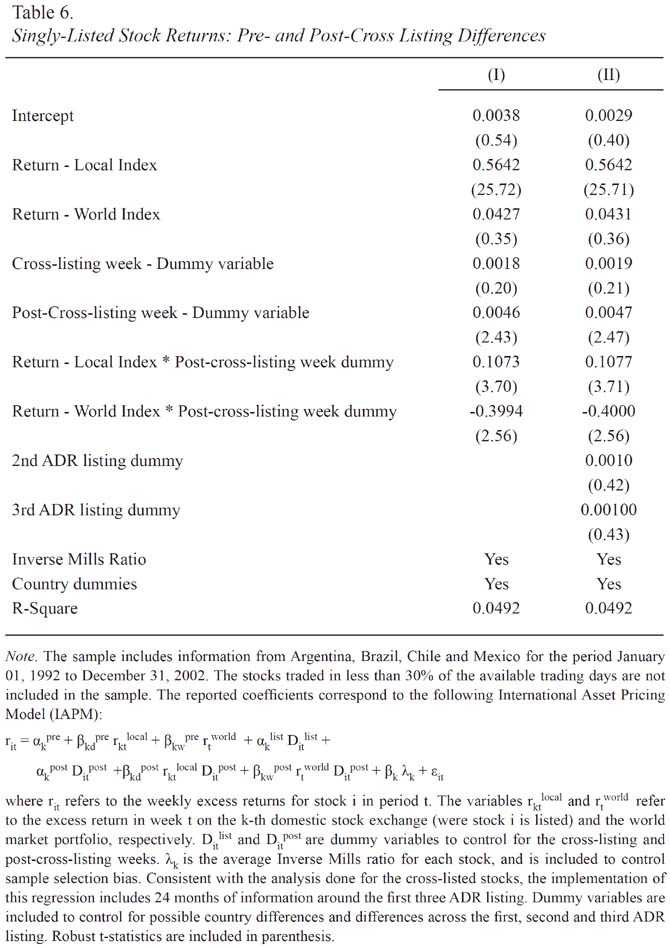

Table 6 reports the equation (8) estimated coefficients for the singly-listed stocks traded in more that 30% of the available trading days. Dummy variables are included to control for possible country differences. In addition, dummy variables are included to control for possible differences across the first, second and third ADR listing effects. As all the first three ADR-listings occurred before 1997, the inclusion of this control variable is not relevant. Similarly, year dummies are not included as they are strongly correlated with the first, second and third ADR-listing dummy. The results highlight significant positive abnormal returns for the post-cross listing period. In addition, the coefficients of the interactive terms emphasize that the singly-listed stocks become more isolated from world markets for the post-cross-listing period (i.e. the importance of the world index returns to explain the stock returns decreases for the post-cross-listing period)24.

Given the nature of the results (i.e. isolation of singly-listed stocks) it is important to examine the long-run persistence of these effects. To examine this possibility the following regression is estimated:

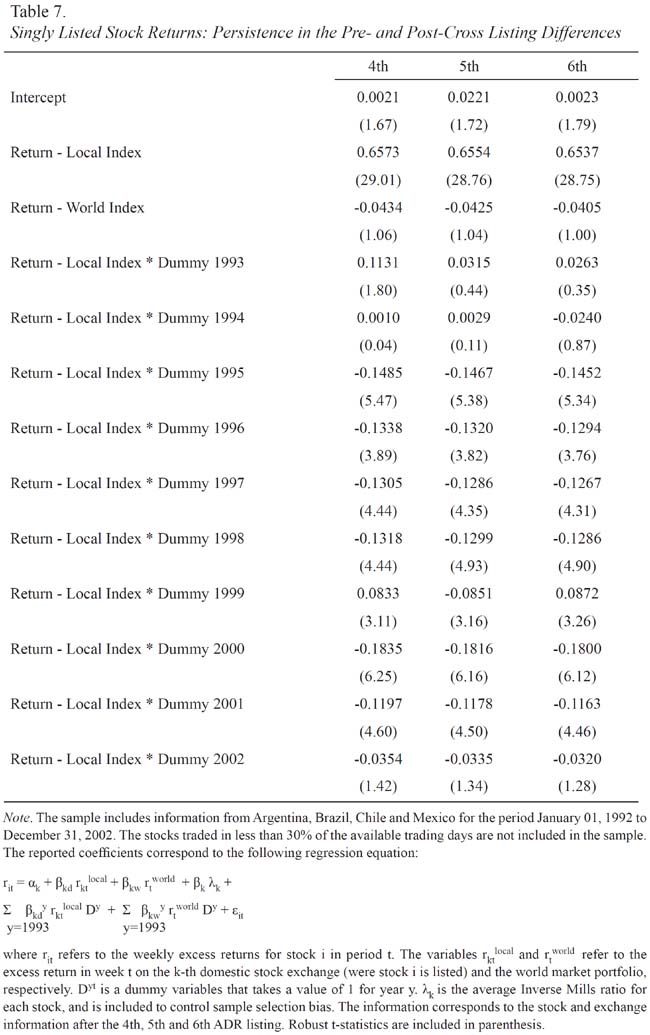

where rit refers to the weekly excess returns for singly-listed stock i in period t. The variables rlocal and rworld refer to the excess return in week t on the k-th domestic stock exchange (were stock i is listed) and the world market portfolio, respectively. Dy is a dummy variable that takes a value of 1 for year y. λk is the average Inverse Mills ratio for each stock, and is included to control sample selection bias. The information corresponds to the stock and exchange information after the fourth, fifth and sixth ADR listing.

Table 7 reports equation (9) estimated coefficients considering the singly-listed stocks traded on more than 30% of the available trading days. The results indicate that the return on the local index, if compared with the 1993return on the world index, explains a larger portion of the singly-listed stock return. From 1995 to 2001, all the local index return coefficients are significant; for the same period only two world index return coefficients are significant. An F-Test is implemented to determine if the local index and world index return coefficients were significantly different from zero. Although the results indicate that both sets of coefficients25 are significantly different from zero, the results for the local index return coefficients are much stronger. All of this evidence is consistent with the idea that in the long-run, a significant portion of the singly-listed returns can be explained by changes in the local index returns that provides evidence for a continuous isolation of this type of stock from global markets26.

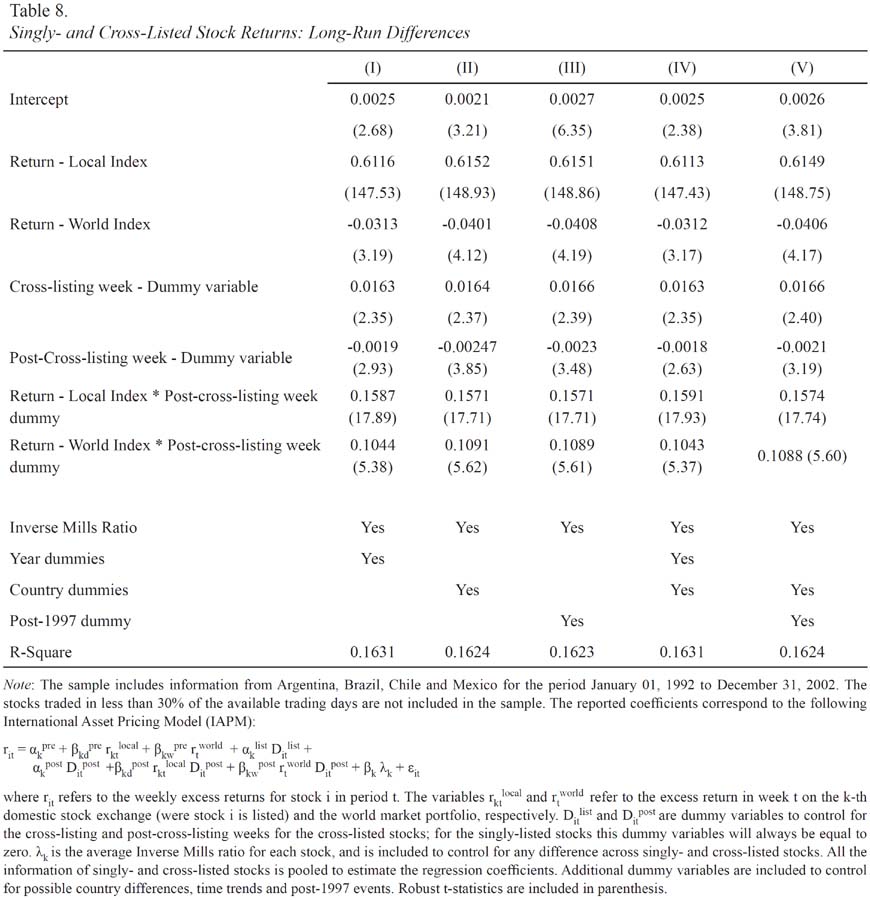

Table 8 reports equation (8) estimated coefficients that correspond to the long-run differences in the returns of the singly- and cross-listed stocks traded in more than 30% of the available trading days. The coefficients for five different regressions are reported and correspond to different combinations of the year, country and post-1997 control variables. These results provide evidence of significant differences in the excess returns behavior of these two groups of securities. As expected, cross-listed stocks returns are larger (smaller) for the cross-listing (post-cross-listing) week if compared with singly-listed stock returns. The coefficient for the cross-listing (post-cross-listing) week dummy variable is significant and positive (negative); this is evidence that the cross-listed stock returns increase (decrease) during (after) this period. The interactive term Return on World Index * Post-Cross-listing week dummy (significant and positive) provides evidence of a greater integration of cross-listed stocks with world financial markets as compared to singly-listed stocks. In a somewhat unexpected result, in all five regressions, the interactive term Return on Local Index *

Post-cross-listing dummy is significant and positive. This result could be related to a greater integration of the exchange with world markets. This possibility will be addressed in future research work27.

CONCLUSIONS

Overall, these results are consistent with the idea that ADR-listing significantly affects the returns of the domestically-listed stocks. The evidence supports the assertion that cross- listed stocks become more integrated with world markets. However, in contrast, there is a significant decrease in the importance of world market returns to explain the behavior of singly-listed stock returns. Consequently, as singly listed stocks become more isolated from world market, investors will demand a return-premium to compensate for additional risk28. These results contradict those of Alexander et al. (1987), as they reveal that cross listing effects do not evenly spread to all domestically-listed stocks29.

References

Alexander, G., Eun, C., & Janakiramanan, S. (1987). Asset Pricing and Dual Listing on Foreign Capital Markets: A Note. Journal of Finance, 42(Mar), 151-158. [ Links ]

Amihud, Y. (2000). Illiquidity and stock returns: cross section and time series effects. New York University Stern School of Business. Working Paper N° FIN-00-041. [ Links ]

Amihud, Y., & Mendelson, H. (1986). Asset Pricing and the Bid-Ask Spread. Journal of Financial Economics. 17(2), pages 223-249. [ Links ]

Bae, K., Bailey, W., & Mao, C. (2006). Stock Market Liberalization and the Information Environment. Journal of International Money and Finance, vol.25, issue 3, pages 404-428. [ Links ]

Bailey, W., & Chung, P. (1995). Exchange Rate Fluctuations, Political Risk and Stock Returns: Some Evidence from an Emerging Market. Journal of Financial Quantitative Analysis, vol. 30(4), 541-561. [ Links ]

Bailey, W., Karolyi, A., & Salva, C. (2006). The Economic Consequences of Increased Disclosure: Evidence from International Cross-listings. Journal of Financial Economics, 81, 175-213. [ Links ]

Baker, K., Nofsinger, J., & Weaver, D. (2002). International Cross-listing and Visibility. Journal of Financial and Quantitative Analysis, 37(3), 495-521. [ Links ]

Campbell, J., Lo, A., & Mackinlay, A. C. (1997). The Econometrics of Financial Markets. Princeton, NJ: Princeton University Press. [ Links ]

Coffee, J. (1999). The Future as History: The Prospects for Global Convergence in Corporate Governance and its implications. Northwestern University Law Review, 93, 641-708. [ Links ]

Doidge, C., Karolyi, A., & Stulz, R. (2004). Why are Foreign Firms Listed in the US Worth More? Journal of Financial Economics, 71, 205-238. [ Links ]

Domowitz, I., Glen, J., & Madhavan, A. (1997). Market Segmentation and Stock Prices: Evidence from an Emerging Market. The Journal of Finance, vol.52, issue 3, pages1059-1085. [ Links ]

Domowitz, I., Glen, J., & Madhavan, A. (1998). International Cross Listing and Order Flow Migration: Evidence from an Emerging Market. The Journal of Finance, LIII(6), 2001-2027. [ Links ]

Errunza, V., & Losq, E. (1985). International Asset Pricing under Mild Segmentation: Theory and Test. Journal of Finance, 40(March), 105 – 124. [ Links ]

Errunza, V., & Miller, D. (2000). Market Segmentation and the Cost of Capital in International Equity Markets. Journal of Finance and Quantitative Analysis, 35(4), 577-600. [ Links ]

Fernandes, N. (2003). Market Liberalization: Spillovers from ADRs and implications for local markets. Barcelona: IESE Business School. [ Links ]

Foerster, S., & Karolyi, A. (1993). International Listings of Stocks: The Case of Canada and the US. Journal of International Business Studies, 24, 763 – 784. [ Links ]

Foerster, S. & Karolyi, A. (1998). Multimarket Trading and Liquidity: A Transaction data analysis of Canada-US interlistings. Journal of International Financial Markets, 8 [ Links ]

Foerster, S., & Karolyi, A. (1999). The Effects of Market Segmentation and Investor Recognition on Asset Prices: Evidence from Foreign Stocks Listing in the United States. Center for Research Financial Economics, working paper N° 98-11. [ Links ]

Heckman, J. (1979). Sample Selection Bias as a Specification Error. Econométrica, 47(1), 153-161. [ Links ]

Henry, P. B. (2000). Do Stock Market Liberalization Cause Investment Booms? Journal of Financial Economics, 58, 301-334. [ Links ]

Jayaraman, N., Shastri, K., & Tandon, K. (1993). The impact of International cross listings on risk and return: Evidence from American Depositary Receipts. Journal of Banking and Finance, 17, 91-103. [ Links ]

Karolyi, A. (2006). The World of Cross Listing and Cross Listings of the World: Challenging Conventional Wisdom. Oxford Journals: Review of Finance, 10, 99-152. [ Links ]

Kim, E., & Singal, V. (2000). Stock market openings: experience of emerging economies. Journal of Business, 73(1), 25-66. [ Links ]

Kladec, G., & McConnell, J. (1994). The Effect of Market Segmentation and Illiquidity on Asset Prices: Evidence from Exchange Listings. The Journal of Finance, XLIX(2 June), 611-636. [ Links ]

Lang, M., Lins, K., & Miller, D. (2003). ADRs, Analysts and Accuracy: Does Cross Listing in the US Improve a firms information environment and Increase Market Value?. Journal of Accounting Research, 41(2), 317-345. [ Links ]

Lee, D. (2003). Why does shareholder wealth increase when NON-US firms announce their listing in the U.S.?. Korea University Business School. Available at SSRN: <hhtp://ssrn.com/abstract=422960>. [ Links ]

Levine, R., & Schmukler, S. (2003). Migration, Spillovers and Trade Diversion: The Impact of Internalization on Stock Market Liquidity (Working Paper 9614). Cambridge, MA: NBER. [ Links ]

Melvin, M., & Valero-Tonone, M. (2003). The Effects of International Cross-Listing on Rival Firms. Tempe: Carey School of Business, Arizona State University. [ Links ]

Merton, Robert C. (1987). A Simple Model of Capital Market Equilibrium with Incomplete Information. Journal of Finance, 42, 483-510. [ Links ]

Miller, D. (1999). The market reaction to international cross-listings: evidence from Depositary Receipts. Journal of Financial Economics, 51, 103-123. [ Links ]

OHara, M. (2001). Designing Markets for Developing Countries. International Review of Finance, vol. 2, issue 4, pages 205-215. [ Links ]

Parkinson, M. (1980). The Extreme Value Method for Estimating the Variance of the Rate of Return. Journal of Business, 53(1), 61-65. [ Links ]

Puhani, P. (2000). The Heckman Correction for Sample Selection and its Critique. Journal of Economic Surveys, 14(1), 53-68. [ Links ]

Pulatkonak, M., & Sofianos, G. (1999). The Distribution of Global Trading in NYSE-listed Non-US stocks (Working Paper w99-03). New York: NYSE. [ Links ]

Reese, W. A., & Weisbach, M. (2002). Protection of Minority Shareholder Interest, Cross-listing in the United States and Subsequent Equity Offerings. Journal of Financial Economics, 66, 65-104. [ Links ]

Scholes, M., & Williams, J. (1997). Estimating Betas from Nonsynchronous Data. Journal of Financial Economics, 5, 309-327. [ Links ]

Smith, K., & Sofranos G. (1997). The Impact of an NYSE Listing on the Global Trading of Non-US Stocks. (Working Paper w97-02). New York: NYSE. [ Links ]

Stultz, R. (1981). On the Effects of Barriers to International Investment. Journal of Finance, 36(4), 923-934. [ Links ]

Viswanathan, K. G. (1996). Listing in the U.S. Markets by Foreign Firms: Evidence on Return and Risk. Advances in International Banking and Finance, 2, 99-113. [ Links ]

Notas de pie

1 The underlying share refers to the ADRs share traded in the local (non-US) exchange. For example, Teléfonos de México (Telmex) traded in the Mexican stock exchange.

2 For example, you may refer to Foerster and Karolyi, 1999; Miller, 1999; Lee, 2003; Fernandes, 2003; Karolyi, 2004.

3 The rationale behind this argument follows from Pulatkonak and Sofianos (1999). These authors find a strong relation between time zone differences (across domestic and US exchanges) and the strength of volume migration associated with stock cross-listings. Given the fact that the time zone difference across Latin American and US exchanges is, at the most, two hours, the cross-listing effects across these exchanges would tend to be similar.

4 The direction of these spillover effects are believed to be from the cross-listed to the singly-listed stocks.

5 Information from Colombia, Peru and Venezuela stock exchanges was collected. The small market capitalization and limited liquidity of these markets determined their exclusion from the sample.

6 This sample period is consistent with post-liberalization periods included in Blair (2000) in all four countries.

7 The empirical implementation of the different tests is done considering 40% and 50% as benchmark. The final conclusions are not significantly affected.

8 A similar control was implemented by Bailey and Chung (1995).

9 DataStream provides the following definitions for each data item:

-

Closing price (CP): latest price available to us (Datastream) from the appropriate market in primary units of currency.

-

Traded volume (Vol): number of shares traded for a stock on a particular day. The figure is always expressed in thousands.

-

Market capitalization (MCap): Share price multiplied by the number of ordinary shares in issue displayed in millions of units of local currency.

10 Refer to Heckman (1979) and Puhani (2000).

11 This summary is from Heckman.

12 Return on equity = ROE = After tax net income / Shareholders equity

13 Leverage ratio = LR = Total liabilities / Total assets

14 Asset turnover = ATu = Total sales / Total assets.

15 The Pearson correlation coefficient across these two variables is small and significant.

16 Melvin and Valero-Tonone argue that this situation may evidence that investors see rivals as less transparent, less informative and with poorer growth prospects relative to the listing firm. (Working Paper, Tempe, Arizona State University).

17 The IAPM coefficients were also estimated using monthly information. The statistical significance of the results was low. A possible explanation for this situation refers to the high price variability that is observed in these exchanges. Apparently, Foerster and Karolyi (1999) had a similar problem, as they used weekly information to estimate a similar IAPM.

18 Fernandes (2003) uses monthly information to implement a similar IAPM. Foerster and Karolyi (1999) use weekly returns.

19 Levine and Schumukler (2003) find evidence that the intensity of information flows across Asian and US exchanges increased after the 1997 Asian crisis. OHara (2001) considers that there are significant changes in the performance of Latin American exchanges after 1994.

20 12 months before and after the cross-listing week.

21 For the singly-listed stocks, additional dummy variables are included to control for the 2nd and 3rd ADR listing.

22 Return Domestic Exchange Index * Dummy for the post-cross-listing period, and Return World Exchange Index * Dummy for the post-cross-listing period.

23 Similar regressions considering the cross-listed stocks traded in more than 40% and 50% of the available trading days were estimated. The previously indicated conclusions are not affected by this sample change.

24 Similar regressions considering the singly-listed stocks traded on more than 40% and 50% of the available trading days were estimated. The conclusions previously indicated are not affected by this sample change.

25 Local index return coefficients and world index return coefficients.

26 Similar regressions considering the singly-listed stocks traded on more than 40% and 50% of the available trading days were estimated. The previously indicated conclusions are not significantly affected by this sample change.

27 Similar regressions considering all the domestically-listed stocks traded on more than 40% and 50% of the available trading days were estimated. The conclusions previously indicated are not affected.

28 See Stulz (1981), Errunza and Losq (1985).

29 A possible explanation for these differences is that the assumptions behind Alexander et al. model are not satisfied in Latin American exchange markets. In particular, short sales and fixed exchange rates are not available in Latin American markets.