Services on Demand

Journal

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

-

Cited by SciELO

Cited by SciELO

Related links

-

Similars in

SciELO

Similars in

SciELO

Share

Permalink

PermalinkJournal of Economics, Finance and Administrative Science

Print version ISSN 2077-1886

Journal of Economics, Finance and Administrative Science vol.18 no.34 Lima June 2013

ARTICLES

Perceptions of professionals interested in accounting and auditing about acceptance and adaptation of global financial reporting standards

Percepciones de profesionales interesados en contabilidad y auditoría acerca de la aceptación y adaptación de normas internacionales de información financiera

Orhan Bozkurt a,*, Mehmet İslamoğlu b,*, Yaşar Öz c,*

a Inegol Faculty of Business, Uludag University, Bursa, Turkey

b Department of Economics, Faculty of Economics and Administrative Sciences, Bartin University, Bartin, Turkey

c Department of Management, Faculty of Economics and Administrative Sciences, Bartin University, Bartin, Turkey

Abstract

Nowadays, one of the final aims of the institutions working on transparency and standardization of financial statements, and the publication of standards related to the profession of accounting & auditing has been to put into practice a uniform global set of standards which will be applicable in finance. Before 2000, in the case of a preference between IFRS & US GAAP regarding which should be internationally accepted uniform set of application, world public opinion used to accept U.S. Generally Accepted Accounting Principles (US GAAP) as reference. Today, great majority of the world takes IFRS as a reference. This study contains evaluations related to the results of research on the thoughts & perceptions of the professionals interested in accounting and auditing about application and development of international financial reporting standards as national financial reporting standards. As a result of the research, it was determined that those interested in accounting and auditing see significant advantages in the application of IFRS. Accountants and auditors think that in case IFRS is applied, comprehensibility and reliability of financial statements shall increase, at the same time accounting frauds shall decrease.

Keywords: International Financial Reporting Standards, Turkish Accounting Standards, Benefit, Interpretation, Perceptions of Standards, Responsibility, Advantage of Application of International Financial Reporting Standards.

Resumen

Hoy en día, uno de los objetivos finales de las instituciones que trabajan por la transparencia y la estandarización de los estados financieros y por la publicación de normas relacionadas con la profesión de la contabilidad y la auditoría ha sido poner en práctica un conjunto de normas internacionales uniformizadas que se aplicarán en el mundo financiero. Antes de 2000, cuando había que elegir entre las NIIF y los GAAP estadounidenses como conjunto uniforme, aceptado y de aplicación internacional, la opinión pública mundial tendía a admitir los principios estadounidenses de contabilidad generalmente aceptados (US GAAP) como referencia. Actualmente, en la mayoría de los lugares se toman como referencia las NIIF. En este estudio se incluyen evaluaciones relacionadas con los resultados de la investigación acerca de los pensamientos y las percepciones de los profesionales interesados en contabilidad y auditoría sobre la aplicación y el desarrollo de normas internacionales de información financiera como normas de información financiera nacionales. Como resultado de la investigación, se concluyó que las personas interesadas en contabilidad y auditoría observaron ventajas significativas en la aplicación de las NIIF. Los contables y auditores creen que, si se aplican las NIIF, aumentará la inteligibilidad y la fiabilidad de los estados financieros y, a su vez, se reducirán los fraudes contables.

Palabras clave: Normas internacionales de información financiera, Normas turcas de contabilidad, Beneficio, Interpretación, Percepciones de normas, Responsabilidad, Ventaja de aplicación de normas internacionales de información financiera.

1. Introduction

International Financial Reporting Standards (IFRS) is a set of principles published in order to establish a financial reporting discipline and an accounting rule to be adopted worldwide. As opposed to US GAAP, which is rule-based, IFRS is principle-based (Carmona & Trombetta, 2008, p. 455). While rules involve specific criteria, constraints or exceptions, a principle-based approach introduces fundamental ideas and evaluations about economic events and transactions. The basic goal behind publishing IFRS by IASB is to enable companies to present their financial information to persons or institutions that accept themselves as related parties in the most correct, reliable and transparent manner. In this sense, the mission of IASB is to ensure a common language in a financial platform by working on the worldwide application of IFRS. Another important feature of IFRS is to prevent related users, especially investors of the financial statements, to incur financial hardship due as a result of incomplete or deceptive information by allowing current financial data and other related company information which may influence a company's future financial position to be publicly known. Competitiveness and efficiency of international capital market depends on the ability of those who prepare financial statements with communicate well with investors through the channel of financial reports (Rezaeeet al., 2010, p. 142).

Today, companies carry out their activities in mutual interaction in the international arena together with fast improvements in communication and also with the abolition of borders in economic and commercial life. It is seen as ordinary and routine activity for companies in the same industry but in different countries to carry out commercial activity among themselves or a company secures a loan from a foreign financial institution. Smooth and prompt functioning of all these activities depends on putting into practice financial reporting standards which are to be adopted by all countries and which enables a correct, reliable and adequately enlightening financial information system. Regulatory bodies, investors and those who prepare financial statements started to work together for the solution -in the long term- of differences in accounting standards used in the process of creation of financial statements. These efforts focused on two different methods as IASB and the leading persons related to this issue worked. The methods in question are the use of IFRS directly instead of national accounting standards or indirectly, changing national financial reporting standards based upon IFRS (Tokar, 2005, p. 49). In fact, indirect method, i.e. adaptation of national financial reporting standards to IFRS, is to increase international comparability of financial statements by decreasing rules in national financial reporting standards contrary to IFRS (Choi et al., 2002, p. 291). In all over the world, in the adaptation process of IFRS, harmonization of national accounting standards and tax laws can be indicated among the most resisted issues (Baker & Barbu, 2007, p. 272). In Turkey, Turkish Accounting Standards Board (TASB), which has administrative and financial autonomy and responsible from determination of national accounting standards and harmonization of the said standards with those of international accounting, was established pursuant to Additional -1 Article added with law no. 4487 and date 18.12.1999 to Capital Market Law No. 2499. The Board commenced its activities by holding its first meeting on 07.03.2002. TASB translated IFRS prepared by IASB to Turkish and published as Turkey Financial Reporting Standards and the said standards became effective to be applied in companies on the same date.

The aim of this study is to determine the thoughts & perceptions of those preparing financial statements, auditors, investors and others interested in accounting and auditing about harmonization to IFRS of national financial standards which are binding during the process of preparation of financial statements and disclosure. In this way, the aim is also to make contribution to management of harmonisation period without problem and promptly.

There are some limitations to the study. Firstly, the study was conducted in West Black Sea region of Turkey where the number of accountants and auditors constitutes a limited part of all those in Turkey. For validation of the results, research should be conducted in all regions. Naturally, for those who deal with accounting and audit, IFRS applications are very important. In this regard, uncovering the differences in perception if any, will reduce the limitations of this study. Another limitation is that certain respondents had no comprehensive information or training about financial reporting standards at the time of the data collection. This limitation can be dealt with by national institutions taking responsibility. Another limiting factor is that most Turkish independent audit firms are newly established so are in the early phases of the professional process. Despite all these limitations, the results are reliable as the questionnaires with auditors and accountants involved in the research were conducted face-to-face. The rest of the paper is organized as follows.Section 2 briefly presents literature review of both foreign and domestic surveys. In Section 3, the method used in sample selection is described. Section 4 defines measurement model of the survey in detail. The results and discussions of the study are presented in section 5 and 6.

2. Literature review and research hypothesis

The difficulties of harmonization of international accounting standards experienced both between and within countries have been studied and documented in several studies. Different academic resources are utilized and reviewed in the study. The academic resources are classified in two groups, foreign and domestic studies, which are summarized below respectively. A survey was carried out by Joshi et al. (2008) about the perception of the profes sionals interested in accounting and auditing in Bahrain in regard to important issues about application and development of global (international) accounting standards. Whether or not being an auditor, participants of the questionnaire revealed that they tended to be optimist about the necessity of gradual but well implementation and completion of convergence process and that convergence project of IFRS and national financial reporting standards was a useful goal.

Another survey was conducted in Spain by Navarro-García and Bastida (2010) for determination of perception of national companies in order to analyze the results of adaptation of IFRS to national financial reporting standards. In the questionnaire conducted upon accounting and finance managers in 63 Spanish companies, IFRS is perceived as a very qualified regulation which is in conformity with decision making processes. At the same time, participants think that there are considerable differences between IFRS and Spanish Accounting Standards, IFRS is very exhaustive & challenging regulation and that in certain situations IFRS is insufficient about creating cost-efficiency in sales. According to the results of the questionnaire, participants do not think that application of IFRS is more convenient than that of national standards.

Rezaee et al. performed a survey (2010) bymaking use of questionnaire method to evaluate point of view of academicians and practitioners in USA about harmonization of US GAAP and IFRS, majority of the participants believe that an effective harmonisation based on globally adopted accounting standards will be useful for auditors, analysts, those who prepare financial statements and those who set up the standards. Harmonization related to accounting standards in USA is thought to necessitate comprehensive and costly changes in the formation of standards. The process of enhancing accounting standards entails investors, managers and auditors in USA and other countries to be subjected to a special training.

In South Pacific Region (Australia, New Zealand, Papua New Guinea and Fiji) in the process of convergence of IFRS and national financial reporting standards, the relation between the specific features of country and the selection of the proper method in the adaptation of IFRS to national financial reporting standards is searched. The factors that are determined to be inf luential upon the process of convergence to IFRS are the existence of a set of accounting standards used widely in the country during the selection of method, existence and experience of professional accountants, preparation of training and professional courses for professionals, existence of 4 big audit companies and the status of accounting-related-legislation. The results of the study indicate that even after adaptation of IFRS, it is difficult to ensure worldwide comparability of financial reports thoroughly (Chand & Patel, 2008, p. 83).

In Spain and England where contrasting national financial reporting standards and applications are in force, during the first compulsory adaptation of national financial reporting standards to IFRS, a research was realized by Callao Gastón et al. (2010) on the numerical effect of the adaptation activity in question upon the results of financial statements. In both countries the results of financial statements prepared in accordance with both IFRS and national accounting standards were compared and it was found out that numerical effect on the results of financial statements was high. Together with the application of IFRS, the quality of financial information increased especially from the standpoint of investors.

Timoşenko performed a study (2007) on the effectiveness of application of IFRS conducted in Kirghizstan where IFRS has been used officially since 2000 it was determined that the percentage of utilization of standards was high (90%) but it was seen that only a portion of the standards was used. In addition, the following results were found out; training was needed for the comprehension and application of standards (82.5%) and the use of standards was optional (65%).

In Turkey, a research in 2009 on determining Turkish accounting professionals' level of information about TAS, a questionnaire was carried out with 768 professionals from different geographical regions of the country. According to the result of the research, while 77% of sworn-in certified public accountant alleged to have knowledge about TAS, rate of those who had enough information was 54%. For certified public accountants, while rate of those having information was 67%, rate of those having sufficient information was 39%. In the case of public accountants having the lowest rates, rate of those who considered their level of information as sufficient was 34%. As the level of education decreased, rate of those having information also decreased (Erdoğan & Dinç, 2009, p. 154).

In 2011, Çankaya and Hatipoğlu prepared another study in which 406 professionals were involved, expectations of professionals on application and adoption of TAS/TFRS in Turkey were examined and the factors inf luencing expectations were determined as follows; education problem about standards (education factor), inappropriateness of existing set of standards for SMEs which constituted an important part of Turkish economy (factor of economic and legal framework), the standards' having some problems due to their very nature like the way of writing, translation (standard factors), the standards' possibility of being affected from cultural environment during their application (factor of culture) .

In a study conducted by Gonen and Ugurluel (2007), problems in the transition to IFRS applications were searched and 8 different problems were found out.These are technical and complex structure of IFRS, lack of trained personnel knowing IFRS, transition problems from rule-based accounting to principle-based accounting, problems of transparency, fair value approach's leading to complexities, application difficulties due to frequent revisions in IFRS, change in demand and expectancies of investors, and getting rid of tax-oriented model

Some part of other studies carried out in this field in Turkey can be summarized as follows:

In a study carried out among accounting professionals working in West Mediterranean Region, while members in general have positive attitude towards TAS, they demand both training in this field and amendment in laws for harmonization with TAS (Bekçi, 2007, p. 39). In the study conducted by Çankaya (2007), harmonization of Turkey, Russia and China with IFRS was investigated and it was seen that harmonization of Turkey would be relatively easier considering Turkey's infrastructure and regulations. In the postgraduate thesis prepared by Ulku in 2008, the perception of accounting professio nals about IFRS draft for SMEs was investigated and as a result it was understood that the information level of professionals working in Istanbul regarding set of entire IFRS together with the set of IFRS for SMEs was not enough. For the remedy, immediate and continuous training was proposed (Ülkü, 2008, p. 77). In a postgraduate thesis prepared by Ozdemir, as a result of a questionnaire upon those responsible from accounting of SMEs in the Lakes Region. However, practitioners have positive opinions about TAS/TFRS (Özdemir, 2007, p. 115-116). In the postgraduate thesis prepared by Evci, the problems with the application of TAS was investigated in the scale of provinces of Adana and Mersin, it was found out that while the percentage of professionals whose level of information was qualified as good was 44.8%, the percentage of those who knew TAS at application level was 3.4%. This study also indicated that the greatest problem was lack of education (48%). In addition to this, well trained human resource, IT infrastructure, the content of standards, laws, audit and internal structure problems of the companies were determined as other barriers to the application of problems (Evci, 2008, p. 168-170).

In the study of Akdoğan in 2007, the problems facing the application of TAS/TFRS, were recognized as the technical difficulty of comprehensiveness of the standards, application differences and lack of trained personnel

3. Sample selection

In the study, those interested in the professions of accounting and auditing were chosen from the Turkish accountants. The questionnaires were sent via mail and also they were filled in the office of the professionals -face to face.

4. Measurement model

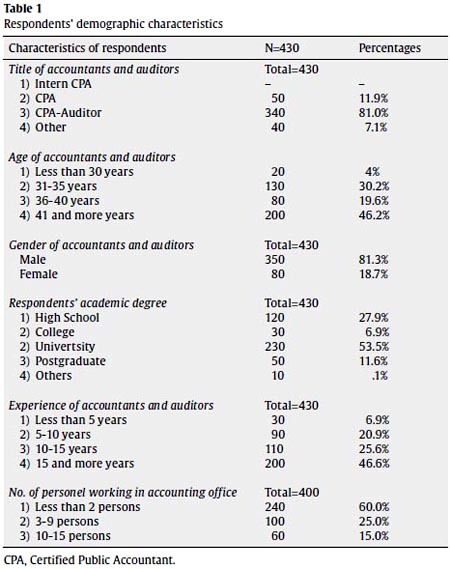

Turkey provided legal framework for accounting system and its applications within the context of Public Accountants and Financial Advisors Act adopted in 1989 in Turkey. During the last years of the twentieth century, Turkey became an important commercial center together with the opening to international markets. In this regard, along with increasing business volume and foreign trade structure, adaptation of national accounting system to developed countries' accounting standards became a compulsory application. Turkey as a member of International Federation of Accountants (IFAC) developed the Turkish Accounting Standards. The basis of these standards is made of international standards. Those who practice the said standards are Certified Public Accountants, Sworn-in Certified Public Accountants and independent audit firms. In Turkey there are 67.238 Certified Public Accountant. Moreover, the number of Sworn-in Certified Public Accountants having the authority of approval pursuant of Law No. 3568 is 3.944. Besides, 4 big international auditing firms carry out audit activities in Turkey. These firms play significant roles in the harmonisation of international accounting standards. For the purpose of the questionnaire, the questions were determined by investigating articles published in internationally recognized journals. For using in the questionnaire, questions were taken from Joshi et al. (2008) and adapted. Through the questions in this study, the opinions of Turkish Certified Public Accountants about accounting standards tried to be learned. In the questions of the questionnaire, 5 Likert Scale was used (1 to 5 was used5=strongly agree (SA); 4=agree (A) 3=neutral (N); 2=disagree (D); 1=strongly disagree (SDA). The answers to the questions of the research and the percentages are indicated in Table 1.

In the first question posed to those interested in accounting and auditing professions, titles of these professionals were asked as can be seen in Table 1. Distribution related to the answers indicates that significant part of the respondents is composed of Certified Public Accountants -auditor- with a percentage of 81%. The other part of the respondents is Public Accountants with a percentage of 11.9%. In Turkey, Independent Accounting (Public Accountant) was removed with an amendment dated 10.07.2008 in Public Accountants, Certified Public Accountants and Sworn-in Certified Public Accountants Law No.3568. However, this law recognized those working with title to work. Looking at the average ages of accountants and auditors in the research, 41 years of age and older (46.2%), 36-40 years of age (19,6%) and under-30 years of age (30.2%) are seen. In general, it is seen that half of the accountants and auditors are under-45 years of age. Significant part of professionals responding the questionnaire is composed of males (81.3%) This indicates that the profession has predominantly male-profile. When educational levels of the participants of the questionnaire are examined, it is seen that 53.5% of the respondents graduated from a 40-year-college (university) or a college and 11.6% of them attend a postgraduate programme. Interestingly, being a public accountant or financial advisor requires graduation from at least a 40-year college (university) or a college. It can be seen from the above table that 11.9% -50 persons- of the high school graduates with a percentage of 27.9% -120 persons- work only as accountant. The rest serves as accountant - financial advisor. It can be derived that 7 professionals acquired this title when Law No. 3568 entered into force. Another striking result in the study is that important part of the personnel working in the offices of accountants or auditors (240 persons, 60%) is composed of 2 or more personnel.

The summary of hypotheses

The Hypotheses subject to the research are listed below respectively.

-

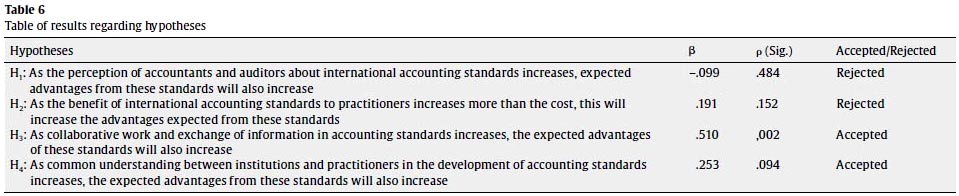

H1: As the perception of accountants and auditors about inter national accounting standards increases, expected advantages from these standards will also increase.

-

H2: The idea that benefits of international accounting standards are more than the cost will increase the advantages expected from these standards.

-

H3: As collaborative work and exchange of information in accounting standards increases, the expected advantages of these standards will also increase.

-

H4: As common understanding between institutions and practitioners in the development of accounting standards increases, the expected advantages from these standards will also increase.

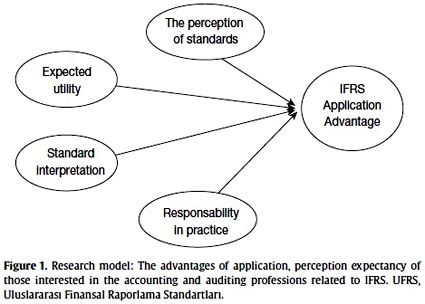

In this study, questionnaire was used as data collection method. For data evaluation, whether hypotheses are verified or not were tested with the help of statistical methods and SPSS by using SPSS for Windows 18.0 statistic packaged software. For this purpose, factor analyses of variables subjected to the research, reliability analyses, correlation analyses and regression analyses were carried out (Fig. 1).

4.1. Factor analysis results

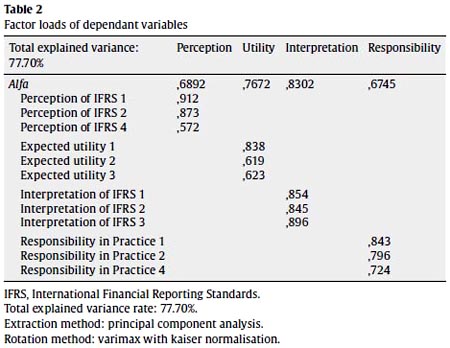

Data obtained from the application of Questionnaire was subjected to factor analysis in conformity with hypothesis structure. In this analysis, for the purpose of evaluation of perception of accountants and auditors about IFRS, the measurement of whether or not IFRS applications provide an advantage on factors like the perception and interpretation of standards, cost-benefit and accounting responsibility perception etc. was targeted. The perception of standards, cost-benefit, interpretation and accounting responsibility perception behaviors were subjected to analysis as independent variable, the advantages of IFRS applications were subjected to dependent variable as dependant variable. The results related to these variables can be seen in Table 2. Total explained variance was 77.70% as shown in table.

4.2. Reliability analysis

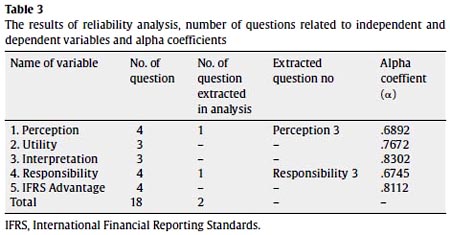

In accordance with the factor distribution resulting from as a result of factor analysis, alpha coefficients of every single variable were observed. Values resulting from factor analyses and provided below in Table 3 were quite satisfactory. It is stated that in the literature, for values resulting from reliability analysis to be considered as accepted level, alpha value must be minimum 0.6 (Bagozzi & Yougae, 1988).

4.3. Correlation analysis results

Table 4 covers correlation coefficients of variables of research subject, averages and standard deviation values. In the analysis process, independent variables were firstly listed then dependant variable was evaluated.

4.4. Regression analysis and hypothesis tests

Model 1: Y1 = β0+ β1· X1+ β2· X2+ β3· X3+ β4· X4+ β5· X5

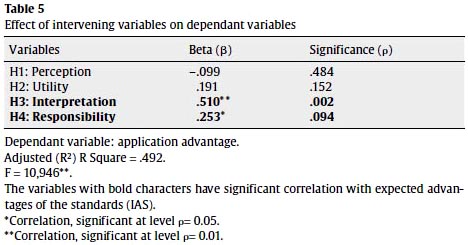

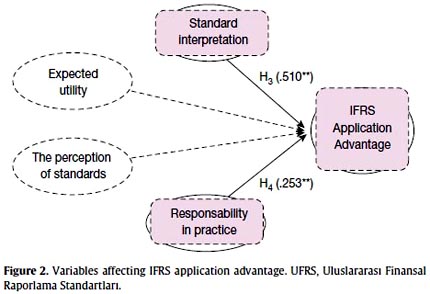

As can be seen from Table 5, dependant variable of TFRS application advantage together with independent variables which are perception, cost-benefit, interpretation and res pon sibility were subjected to analysis according to Model 1. In regression model, dependant variable application advantage was subjected to analysis. The values obtained as a result of analyses were R2 = .492 ve F = 10.946 ve ρ< 0.00. As a consequence of expressed regression analysis; positive significant correlation was found to be ρ< 0.00 between application advantage and interpretation and ρ< 0.05 between application advantage and responsibility. These results indicated that H3 and H4 were established as significant. When a comparison was made on variables with positive contribution, it was concluded that evaluation of IFRS was considered very important with respect to accounting and auditing professionals with high β value of 0.511 and at significant level of ρ< 0,00, and concluded that this perception contributed to professionals and their activities, therefore applying IFRS would be advantageous. On the other hand, it was seen that responsibility perception with significant level of ρ< 0.05 and with β value like 0.253 created value for accounting and audit professionals. In interpretation performed according to regression analysis of variables related to H1 perception and H2 utility, it was observed that these behaviors did not contribute to providing advantage. In the findings; apart from perception and utility behaviors, interpretation and responsibility perception variables provide advantageous in IFRS applications. Hence, while our hypotheses, perception and utility (H1 ve H2) did not provide advantage expected from IFRS applications, interpretation and increasing responsibility (H3 ve H4) will increase advantages expected from application of collaborative works & common understanding, IFRS applications (Table 6; Fig. 2).

5. Results

In this study, expectations of accountants and auditors related to accounting and auditing activities in regard to IFRS were taken up. The effect of utility, perception, interpretation and responsibility behaviours of those dealing with accounting and audi ting acti vities on IFRS application advantage to be obtained was tested. In the global world of today, facilitation of international capital movements caused accounting and auditing activities to be more important. Performing accounting records in accordance with international and national standards is of vital importance for those who will benefit from these records and reports. In this regard, audit; on the one hand meets needs of the management, on the other hand serves as a development protecting rights of investors which is one of the aims of external audit (Atkinson, 1946). This study is about learning the thoughts of those interested in accounting and audit professions regarding the adaptation of IFRS at national level. Additionally, this study explored how these practitioners' level of perception of IFRS, cost-benefit, interpretation and responsibility influenced application advantage.

In the findings obtained in the research, international financial reporting standards are considered as applicable standards in the country by accounting and auditing professionals. In order to increase application of the standards at national level, increase in collaboration and information f low among institutions are necessary. Especially respondents believe that for having a common interpretation of IFRS, the participation of the institutions like Capital Market Board (CMB), Turkish Accounting Standards Board (TASB) and Union of Chambers of Certified Public Accountants and Sworn-in Certified Public Accountants in Turkey (UCCPAT) is essential. In such a case, they expressed that they would agree on the idea of 'necessary for interpreting the standards' with a percentage of (Appendix b) 4.21. Respondents consider that standards are prepared according to certain principles. As shown in Table 5 and Table 6, respondents in the analysis of the research see a linear relationship between application and interpretation with high level of .510**. In this regard, as colla boration and information flow in accounting standards increase, these standards will be interpreted well and hence advantages expected from these standards will increase. These advantages can be viewed as facilitation of comparability of financial statements in the World, transparency and reliability of financial statements and reducing illegal activities especially frauds in preparation of financial statements. On the other hand accountants and auditors related the understanding of responsibility and the contribution from the application. The important result of this analysis is that majority of the respondents (Appendix b, average 4.23) agreed on the idea that application training of IFRS should be under the responsibility of state. Furthermore, the result obtained from other questions is that there are expectations from public institutions in IFRS adaptations. During analysis, it was derived from 3rd Analysis, from the questions related to responsibility variable. This is reverse question. In this question, respondents did not agree that IFRS application training should be ensured through personal efforts. In the other questions, the participants believe that public institutions (universities, standard boards, professional institutions etc.) should play role in the adaptation of IFRS. Then, as common understanding between institutions and practitioners in the development of accounting. On the other hand, it seems interesting that respon dents' IFRS perception levels have no effect on application advan tage. Nevertheless, respondents do not consider the utility thought to be provided by IFRS applications as an advantage. As a result of analysis, a linear relationship could not be found between these variables and application advantage. In this sense, on national basis, public institutions and professional organisations should make more efforts for extending IFRS. This effort should also be made by accountants and auditors. Internal auditor and practitioners should help each other for application of accounting (Janvrin et al., 2010). As a result, the basic conclusion provided from the study, by taking responsibility in IFRS applications, accounting and auditing professionals may increase accounting application advantage depending on cooperation. Another result is that in order to increase expected advantage it is necessary for auditing institutions and professional institutions to assume responsibility. Globally operating companies need applications with the same universal language. In this regard, there should not be applications which will cause confusion in interpretation of the financial statements (balance sheet and income statement). This is because those conducting business in financial markets pay importance to the reliability of financial statements. When those who prepare these statements manage to be professional in their business, public will be enlightened better and in turn this will make contribution to analyses of user of financial statement.

6. Discussion

This study is conducted to measure the views of professionals dealing with accounting and auditing activities about application of IFRS also in Turkey. The prepared questions are collected under four dependant variable and an independent variable. As a result of the conducted analysis, for accountants and auditors to take advantage of IFRS applications and for ensuring a common interpretation of IFRS, international regulatory institutions (IASB-IFRIC) should play regulatory role and also at the national level the institutions like CMB, TASB and UCCPAT should act as partners for these studies. The more corporate studies and application are conducted to consolidate the standards, the more the expected utility from the analysis of IFRS as basic standard increases proportionally. On the other hand, the more training at university and professional level for development of the standards and public sector assumes responsibility, the more advantages expected from IFRS applications increase proportionally. In the analysis of answers given to the research questions, as can be seen above, those interested in accounting and auditing consider the interpretation of standards in IFRS applications and institutions' assuming responsibility as a positive approach for the application advantage expected from the standards. Nonetheless, the same professionals consider cost-benefit analysis as significant for application advantage of IFRS. In other words, they hold that IFRS applications will be more costly when compared to the expected utility. Anyway, in the long run, both undertakings and users will gain significant benefits from these applications. Especially, ensuring uniform accounting records and consistency of reports (balance sheet, income statement etc.) obtained from these records will be available through comprehension of IFRS applications better. In this regard, this study is designed for the purpose of contribute to literature and to learn the views of Turkish accountants and auditors. For generalization of the study, if academic studies are con ducted from the perspective of other regions, this will provide positive results. In the final analysis, the contribution of this study may be limited. However, as based on scientific research, this study draws attention to the further studies to be conducted in Turkey related to this subject in the future.

Authors

Orhan Bozkurt has been working as a Assistant Professor in the Faculty of İnegöl Business at Uludag University, Turkey since 2012. He received a PhD degree in cost accounting field from the Gebze Institute of Technology (GIT), Kocaeli, Turkey, in 2004. His primary specialization is cost of production. His research interests are cost management and corporate performance.

Mehmet İslamoğlu completed his MS education at 1997 in Business Administration Department at Marmara University. In early 2002, he received a BS Degree in Financial Audit from University of Istanbul . He had a professional carrier in Turkish Banking Industry between 1998 and 2010. He received his PhD Degree from Finance and Banking Program of Kadir Has University, İstanbul at 2010. Since 2010, he has been working as an Assistant Professor of Finance at Bartin University. His research interests are financial reporting, valuation of fixed income securities and capital markets.

Yaşar Öz has been working as an Assistant Professor of Business Administration at Bartin University, Turkey since 2009. He completed his BS education in Business Administration at Atatürk University in 1996. He received MSc and PhD degrees in the same field from Atatürk University, Erzurum, Turkey respectively in 1999 and 2005. His primary concerns are financial accounting and auditing.

References

Akdoğan, N., 2007. Türkiye Muhasebe/Finansal Raporlama Standartlarinin Uygulanma Süreci: Sorunlar, Çözüm Önerileri. Mali Çözüm Dergisi 80, 101-117.

Atkinson, T.C., 1946. Significant contributions of modern internal auditing to manage ment. The Accounting Review 21 (2), 121-128. http://www.jstor.org/stable/239914.

Baker C.R., Barbu, E.M., 2007. Trends in research on international accounting harmonization. The International Journal of Accounting, 42 (3), 272-304. http://dx.doi.org/10.1016/j.intacc.2007.06.003.

Bagozzi R.P. & Yougae Y.I. (1988). "On the evaluation of structural equation Models" Journal of Academy of Marketing Science, 16 (Spring), 74-94.

Bekçi, İ., 2007. Muhasebe Meslek Mensuplarinin Türkiye Muhasebe Standartlari Hakkindaki Görüşlerinin Değerlendirilmesine Yönelik Bir Araştirma. Muhasebe ve Denetime Bakiş 22, 27-40.

Callao Gastón, S., Ferrer García, C., Jarne Jarne, J.I., Laínez Gadea, J.A., 2010. IFRS adoption in Spain and The United Kingdom: Effects on accounting numbers and relevance. Advances in Accounting, Incorporating Advances In International Accounting 26, 304-313.

Carmona, S., Trombettai, M., 2008. On the global acceptance of IAS/IFRS accounting standards: The logic and implications of the principles-based system. Journal of Accounting and Public Policy 27 (6), 455-461. http://dx.doi.org/10.1016/j.jaccpubpol.2008.09.003.

Chand, P., Patel, C., 2008. Convergence and harmonization of accounting standards in the South Pacific Region. Advances in Accounting 24 (1), 83-2. http://dx.doi.org/10.1016/j.adiac.2008.05.002.

Choi, F., Frost, C., Gary, K., 2002. International accounting (4th ed). Prentice-Hall, New Jersey, NJ.

Çankaya, F., 2007. An application towards the measurement of international accounting harmonization: a comparison of Russia, China and Turkey. Ulus lararasi Yönetim İktisat ve İşletme Dergisi 3 (6), 127-148.

Çankaya, F., Hatipoğlu, O., 2011. An investigation of the evaluation of the accounting profession towards the applicability of IAS/IFRS in Turkey. International Journal of Economic and Administrative Studies 3 (7), 61-88.

Erdoğan, M., Dinç E., 2009. Turkish accounting standards and an analysis to the perception of accountants. MUFAD Dergisi 43,154-169.

Evci, S., 2008. Turkish accounting standards (financial reporting) and problems faced in the application of it. Gazi University, Department of Business Administration, Ankara.

Gönen, S., Uğurluel, G., 2007. Türkiye'de Uluslararasi Finansal Raporlama Standartlari (UFRS) Uygulamalarina Geçişte Karşilaşilan Sorunlar ve Çözüm Önerileri. Vergi Dünyasi Dergisi 316, 229-236.

Janvrin, D., Caster, P., Elder, R., 2010. Enforcement release evidence on the audit confirmation process: Implications for standard setters. Research in Accounting Regulation 22 (1), 1-17. http://dx.doi.org/10.1016/j.racreg.2010.02.002.

Joshi, P.L., Bremser, W.G., Al-Ajmi, J., 2008. Perceptions of accounting professionals in the adoption and implementation of a single set of global accounting standards: Evidence from Bahrain. Advances in Accounting, 24 (1), 41-48. http://dx.doi.org/10.1016/j.adiac.2008.05.007.

Navarro-García, J.C., Bastida F., 2010. An empirical insight on Spanish listed companies' perceptions of International Financial Reporting Standards. Journal of International Accounting, Auditing and Taxation, 19 (2), 110-120. http://dx.doi.org/10.1016/j.intaccaudtax.2010.07.003.

Özdemir, O., 2007. Impacts of Turkish Financial Reporting Standards on financial statements and a research about SME's accounting managers in the lake district area. Suleyman Demirel University, Department of Business Administration, Isparta. Available at http://tez.sdu.edu.tr/Tezler/TS00590.pdf

Rezaee, Z., Smith, L.M., Szendi, J.Z., 2010. Convergence in accounting standards: Insights from academicians and practitioners. Advances In Accounting 26 (1), 142-154. Available at http://ssrn.com/abstract=1703584

Timoşenko, V., 2007. Uluslararasi Finansal Raporlama Standartlari ve Kirgizistan'da Uygulama Etkinliğine İlişkin Bir Araştirma. Kyrgyzistan Manas University, Depart ment of Business Administration, Bishkek.

Tokar, M., 2005. Convergence and the implementation of a single set of global standards: The real-life challenge. Accounting In Europe 2 (1), 49-68. http://www.tandfonline.com/doi/abs/10.1080/09638180500379079.

Ülkü, S., 2008. A research of accountants perception about IFRS for SMEs rough draft (Sample of İstanbul). Sakarya University, Department of Business Administration, Sakarya.

Article history:

Received December 9, 2012

Accepted February 14, 2013

* Corresponding author:

E-mail address: obozkurt@uludag.edu.tr (O. Bozkurt); mislamoglu@bartin.edu.tr (M. İslamoğlu); yasaroz@bartin.edu.tr (Y. Öz).