Services on Demand

Journal

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

-

Cited by SciELO

Cited by SciELO

Related links

-

Similars in

SciELO

Similars in

SciELO

Share

Permalink

PermalinkJournal of Economics, Finance and Administrative Science

Print version ISSN 2077-1886

Journal of Economics, Finance and Administrative Science vol.24 no.48 Lima July/Dic. 2019

http://dx.doi.org/https://doi.org/10.1108/JEFAS-11-2018-0120

ARTICLE

Internet financial reporting adoption: Exploring the influence of board role performance and isomorphic forces

Juma Bananuka1,*

Sadress Night1

Muhammed Ngoma1

Grace Muganga Najjemba 1

1Makerere University Business School, Makerere University, Kampala, Uganda

Corresponding author: *jbananuka@mubs.ac.ug

Abstract

Purpose: This study aims to examine the contribution of board role performance and isomorphic forces on internet financial reporting.

Design/methodology/approach: This study is cross-sectional and correlational. Data were collected through a questionnaire survey of 40 financial services firms. The study’s unit of analysis was a firm. Chief Internal Auditors and Chief Finance Officers were the study’s unit of inquiry. Data were analyzed through correlation coefficients and linear regression using Statistical Package for Social Sciences.

Findings: The results suggest that board role performance and isomorphic forces are significant predictors of internet financial reporting. However, board role performance is not a significant predictor of internet financial reporting in the presence of isomorphic forces. The control and strategic roles of the board are positively and significantly associated with internet financial reporting unlike the service role. Only the coercive isomorphism is positively and significantly associated with internet financial reporting unlike the normative and mimetic isomorphism.

Originality/value: This study provides initial empirical evidence on the contribution of board role performance and isomorphic forces on internet financial reporting using evidence from Uganda’s financial service firms. To the researcher’s knowledge, this is the first perception-based study on internet financial reporting.

Keyword: Internet financial reporting, Isomorphic forces

1. Introduction

The usage of internet in financial reporting is on the increase among firms around the world (Dolinšek and Lutar-Skerbinjek, 2018; Mokhtar, 2017; Siala et al., 2014; Ettredge et al., 2002). According to FASB (2000), firms prefer the internet for financial reporting because of its low cost of disseminating information, providing timely information, enhancing the extent and type of information disclosed and improving access to potential investors. The use of firm’s web site to disseminate information about its financial performance is termed as internet financial reporting (IFR) (Purba et al., 2013; Debreceny et al., 2002). IFR is thus preferred as compared to the manual (traditional) financial reporting because of its effectiveness in communication over a large group of people especially investors, lenders and other stakeholders at slightly a lower cost and in a timelier fashion (Dolinšek et al., 2014). Whereas there is an increased internet usage worldwide especially in the financial services firms, the usage of internet in emerging economies such as Uganda is still low. Internet usage in Uganda is at 31.4 per cent (about 13 million people) as compared to Africa’s 35.2 per cent (Internet World Stats, 2017). According to Belson (2016), Uganda and Ethiopia are some of those countries with the lowest internet connectivity and this implies that firms must invest more resources in internet infrastructure to be able to upload financial reports on a timely manner. In the presence of low internet connectivity, there are financial services firms such as Stanbic Bank whose financial statements can be found on their websites while other financial services firms do not upload their financial statements on their websites. Questions thus continue to rise on what exact mechanism can be employed to ensure all financial services firms’ financial statements are uploaded on their websites.

The current debate on IFR is on what determines its adoption. A number of studies have been conducted on the determinants of IFR but most of these studies have focused on firm specific characteristics (Aly et al., 2010; Dolinšek et al., 2014 Mokhtar, 2017), board independence (Abdelsalam and El-Masry, 2008), corporate governance efficiency (Botti et al., 2014) and Audit committee effectiveness (Bin-Ghanem and Ariff, 2016). The call for further studies by previous scholars is also common with the most recent being Mokhtar (2017) who called for further studies on the effect of corporate governance on internet reporting. In addition, Dolinšek and Lutar-Skerbinjek (2018) made a call for a study on IFR using perceptions since existent studies had relied on disclosure indices. In this study, a questionnaire survey is used to elicit views and opinions of chief internal auditors and chief finance officers. Mokhtar (2017) carried out a Meta analytic study on the determinants of IFR and his findings were that there is a significant positive association between firm size, profitability, leverage, auditor type and IFR. Mokhtar (2017) further found that investor protection, masculinity, economic development, construction of disclosure index and measurement proxies for independent variables moderate the association between profitability, leverage and IFR. In addition, Dolinšek et al. (2014) found that company size, ownership concentration, legal form and sector of operation have a significant relationship with IFR in Slovenia. Audit committee effectiveness was found to be significantly associated with internet financial reporting (Bin-Ghanem and Ariff, 2016).

There are hardly any studies that have linked board role performance and IFR. Available scant studies have linked board role performance in terms of strategic, control and service roles with internal controls over financial reporting (Nalukenge et al., 2017) and human capital (Nkundabanyanga et al., 2014). Nalukenge et al. (2017) found a positive significant association between board role performance and internal controls over financial reporting while Nkundabanyanga et al. (2014) found that board role performance is affected by prior decisions like investing in corporate social responsibility activities, targeting employees that augment firm characteristics like existence of appropriate human capital. Nkundabanyanga et al. (2014) argued that an improvement in the quality of human capital explains positive variances in board role performance. Studies that link isomorphic forces to IFR are uncommon. Isomorphic forces have been linked to voluntary disclosures by scholars such as Nyahas et al. (2017) who found that isomorphic forces are positively associated with voluntary disclosures of listed firms in Nigeria. DiMaggio and Powell (1983) categorize isomorphic forces into three: coercive, mimetic and normative. Given the scant literature on the contribution of board role performance and isomorphic forces using evidence from Uganda, this study aims to fill this gap. This is done through a questionnaire survey of 40 financial services firms in Uganda. Results suggest that, both board role performance and isomorphic forces (IF) are significant predictors of IFR and explain 23 per cent of the variance in IFR in Uganda.

The results in this paper are particularly important for several reasons. First, they contribute to existing literature by providing initial empirical evidence on the contribution of board role performance and isomorphic forces on IFR. This is important for regulators like the Bank of Uganda and Insurance Regulatory Authority to encourage financial services firms to disseminate financial performance information on their websites and for supervision purposes. Second, the results suggest to management of financial services firms to respond to pressures from various stakeholders, as this will enable them to enjoy the benefits of adoption of IFR. Finally, the results suggest that, the community and other external stakeholders can always demand for financial information via the internet as this saves the various stakeholders the cost of walking into bank premises to seek for information.

The rest of the paper is organized as follows. Section 2 reviews literature and develops hypotheses. This is followed by a discussion of the research methodology in Section 3. Section 4 presents results. Section 5 is discussion of findings while the final section is summary and conclusion.

2. Literature review

2.1 Theoretical foundation

IFR is the distribution of corporate financial performance information through the entity’s website to a wide range of users for timely decision making. IFR is a topical issue in the accounting arena, and we utilize the diffusion of innovation (DOI) theory and institutional theory to inform our study. The theory of DOI asserts that innovation diffusion is a general process not bound by the type of innovation studied, by whom the adopters are, or by place or culture (Rogers, 2003). Rogers (1995, p. 5) defined diffusion as the process by which an innovation is communicated through various channels overtime among the members of a social system. In accounting literature, DOI has been used in IFR and integrated reporting. In the context of accounting, diffusion refers to the spreading of new accounting procedures to and within organizations where they had not previously been present (Mellett et al., 2009, p. 747). Rogers’ DOI theory is the most appropriate for investigating the diffusion of IFR among financial services firms since IFR is still new in the accounting arena especially in developing countries. Sahin (2006) further suggests that, for one to adopt an innovation, he or she will have the knowledge of what should be adopted, persuaded to adopt an innovation and a decision to adopt an innovation will be taken. Rogers (2003) further argues that uncertainty curtails the speed of adopting innovation but suggests that the adopters of a given innovation should be alerted on the benefits and dangers of such an innovation. DOI theory recognizes that the fact that in any firm, there should be those individuals who may spearhead an innovation and those individuals have been termed as change agents. DOI identifies managers or heads of institutions to spearhead an innovation among a social system. Management and board of directors who are the internal stakeholders will make decisions that aim at ensuring that the new accounting system is adopted and used if it can be beneficial to the entity. In the context of this study, the board can be the propagators of IFR if they perform their control, service and strategic roles.

The institutional theory is based on the key idea that the adoption and retention of many organizational practices are often more dependent on social pressures for conformity and legitimacy than on technical pressures for economic performance (Kessler, 2013; DiMaggio and Powell, 1983). The institutional theory is the most influential theory in recent decades addressing issues of institutional development (DiMaggio and Powell, 1983; Meyer and Rowan, 1977). This theoretical approach was developed in connection with the study of organizations (DiMaggio and Powell, 1983) but has since been expanded to cover the analysis of institutional change (Meyer and Rowan, 1977). The institutional theory suggests that organizations respond to pressures arising from both their external and internal business environments and adopt structures and practices that are accepted as appropriate organizational choices and considered legitimate by other organizations in their fields (DiMaggio and Powell, 1983; Meyer and Rowan, 1977). Similarly, Hoffman (1999) urges that institutional theory deals with how organizations are affected by external and internal forces which locate beyond their own control. These forces cause them to adopt similar structures and practices. Hence over time, the organizations tend to become similar or isomorphic (Hoffman, 1999; Meyer and Rowan, 1977). However institutional isomorphism is a useful tool for understanding events that encompass organizational life (DiMaggio and Powell, 1983) such as adoption of IFR. According to Mizruchi and Fein (1999), firms constantly aim at maintaining and increasing legitimacy through agreeing with pressures that arise from their institutional environment. These pressures could be classified into three types that guide organizations toward isomorphism, namely coercive pressure stemming from power exerted by the clients and the regulators, mimetic pressure arise from mimicking reporting behaviors of successful competitors, peers and collaborators in the uncertain environment (Dingwerth and Pattberg, 2009) and normative pressure which describes the effect of cultural beliefs, professional standards and the influence of professional communities on organizational characteristics (Ashworth et al., 2007). Thus, isomorphic forces have an upper hand in explaining the adoption of IFR.

Having considered the theoretical framework, it is thus a worthwhile endeavor to explore the empirical literature and develop hypotheses for this study.

2.2 Board role performance and internet financial reporting

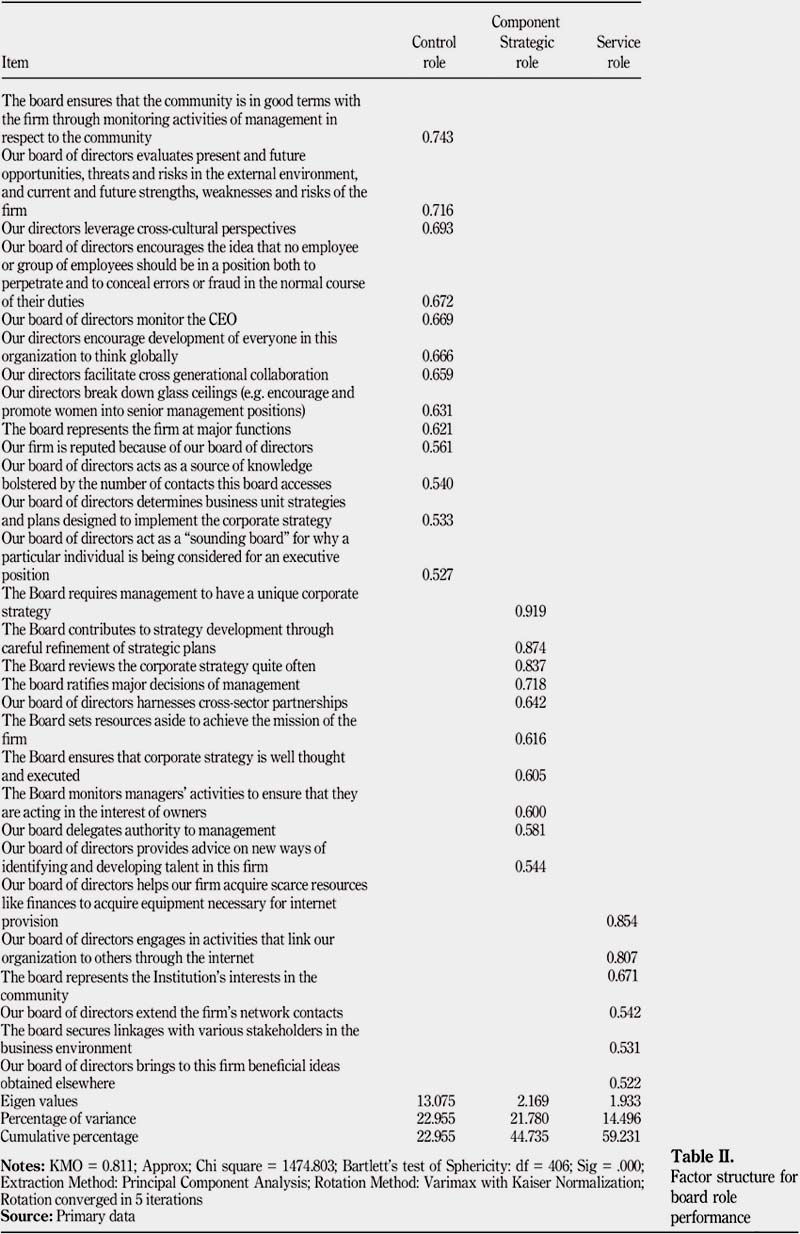

A review of existent literature reveals that board roles include control, service and strategic (Nalukenge et al., 2017; Nkundabanyanga et al., 2014; Zahra and Pearce, 1989; Maassen, 1999 and Levrau and Van den Berghe, 2007). The control role originates from agency theory where the board is supposed to monitor managers to ensure there is protection of the shareholder’s wealth (Halme and Huse, 1997) while the strategic role involves aspects of defining business, developing the mission, scanning the environment, and selecting and implementing a choice of strategies (Pearce and Zahra, 1991). The service roles involve coopting external influences, realizing contacts between board members and relevant individuals to ensure availability of resources, enhancement of the company’s reputation and also advising management in decision-making. Prior studies have examined the influence of board role performance on earnings management, financial reporting and internal control system among others. However, these studies have used proxies such as proportion of NEDs, ownership by directors and Chief Executive Officer (CEO) dominance to imply board monitoring and control (Nalukenge et al., 2017; Vicknair et al., 1993; Peasnell et al., 2005; He, Labelle Piot and Thornton, 2009 and Michelon et al., 2015). Unlike these previous studies, the study uses a perception-based measure of board role performance where respondents were asked to rate the performance of the board.

We thus reason that board role performance encompasses the board executing all the three roles (service, control and strategic role) which will influence IFR adoption among financial services firms. By boards performing their roles, they can help organizations acquire resources and offer management with knowledge and skills (Hillman and Dalziel, 2003) which should improve IFR process. Pearce and Zahra (1991) note that a powerful board ensures organizational effectiveness. Regarding IFR, a board is expected to establish strong processes of operational planning, budgeting, monitoring and reporting progress (Culica and Prezio, 2009). To perform the above roles, the board is expected to ensure that the right persons are selected (Eisenberg, 1997) which will enhance the practice of IFR. Bananuka et al. (2018) found that board role performance is one of those governance factors for the adoption of IFR in Uganda. Nalukenge et al. (2017) found a significant relationship between board role performance and internal controls over financial reporting. This implies that if board role performance is significant in predicting internal controls over financial reporting, it is highly probable that board role performance can as well predict IFR. Therefore, a board that puts in place mechanisms that promote financial oversight, provides strategic direction, vigilant in resource mobilization will lead to better IFR. In this study, it can be hypothesized that:

H1. There is a significant positive relationship between board role performance and IFR.

2.3 Isomorphic forces and internet financial reporting

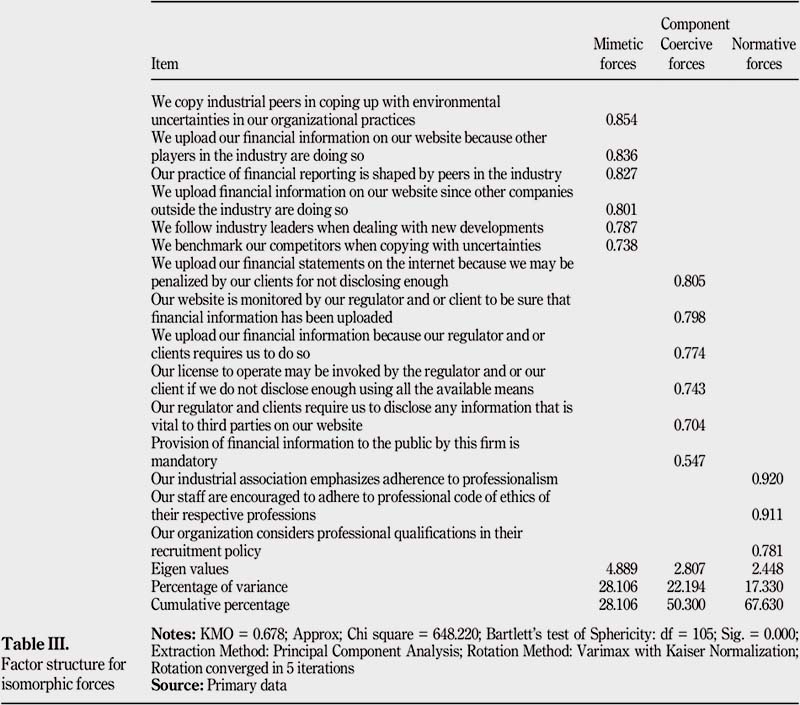

Isomorphism is the notion that firms in similar positions in a field encounter similar circumstances, and so they often construct similar responses to each other on these fronts (Amoako et al., 2017, p. 190). Isomorphism can be understood as a process of socialization in terms of which aspects of everyday life are codified, formalized and institutionalized, ensuring their general acceptance and rendering alternate practices unimaginable (Louw and Maroun, 2017; Meyer and Rowan, 1977). For this study, isomorphism is the constraining process forcing management and those charged with governance to behave like others facing the same set of environmental conditions. The institutional theory recognizes that firms operate within a social arena and considers the social, rather than purely economic influences on firm practice. The theory recognizes that firm practices are influenced by the existence and operation of institutions in their industry or country. These institutions include the legal system (coercive isomorphism), other players in the same industry (Mimetic isomorphism) and cultural and professional norms (Normative isomorphism). DiMaggio and Powell (1983) categorize isomorphic forces into three: coercive, mimetic and normative. Coercive isomorphism refers to companies being forced into a course of action. DiMaggio and Powell (1991, p. 67) asserts that coercive isomorphism results from both the formal and informal pressures exerted by other organizations on which an organization may be dependent, as well as cultural expectations in which the organizations operate. Coercive isomorphism results from political influence and problems of legitimacy (Amoako et al., 2017). Mimetic isomorphism is a response in which corporations imitate other firms that are viewed as more legitimate and successful (DiMaggio and Powell, 1983). In such situations, companies follow early adopters from the same sector if they are uncertain about new technology, often resulting in diffusion as a "fashion" (Xiao et al., 2004). Normative isomorphism refers to the professionalization of norms, that is to say, the collective struggle of members of an occupation to define their conditions and methods of work (DiMaggio and Powell, 1983). DiMaggio and Powell (1983) explain that there are two features of professionalization: through formal education (e.g. in universities), which advocates the DOI, and through the establishment and expansion of professional networks across which new models might diffuse rapidly.

There are minimal studies that link isomorphic forces to internet reporting except for Bananuka et al. (2018) who identified industry pressures, client related pressures, regulatory pressures and employee-related pressures as some of those pressures that once imposed on the management and those charged with governance of financial institutions in Uganda to adopt IFR, then it will be adopted. Isomorphic forces have been linked to voluntary disclosures (Nyahas et al., 2017), adoption of international financial reporting standards (Aboagye-Otchere and Agbeibor, 2012; Nurunnabi, 2017; Louw and Maroun, 2017), auditing environmental matters (Chiang, 2010) and sustainability reporting (Amoako et al., 2017). The use of the internet in financial reporting can be explained by the various pressures from regulators and shareholders who are always demanding for detailed information about what takes place in an organization (Mokhtar, 2017). Nyahas et al. (2017) found out that isomorphic forces are positively associated with voluntary disclosures of listed firms in Nigeria. AboagyeOtchere and Agbeibor (2012) note that significant isomorphic pressures such as legal requirements are brought to bear on them to adopt the IFRS for SMEs. Nurunnabi (2017) suggests that isomorphism especially coercive isomorphism should be more proactive to ensure a successful implementation of IFRS. Further, Louw and Maroun (2017) argue that isomorphic pressures are an important means for demonstrating how corporate reporting requirements can be enforced and are, therefore, more than just symbolic. Chiang (2010) conducted a study on Insights into current practices in auditing environmental matters and found that isomorphic forces are significant in planning an audit and this has to do with deciding on whether to audit environmental matters. Chiang (2010) points out that if management is interested in the audit of environmental matters, auditors will have no option but to do so (normative isomorphism). Relatedly, Amoako et al. (2017) signpost that institutional isomorphism relates to sustainability reporting. Given the foregoing discussion, it can be hypothesized that:

H2. There is a significant positive relationship between isomorphic forces and IFR.

2.4 Control variables

The works of Bartov et al. (2000) suggest that failure to control for confounding variables could lead to falsely rejecting the hypothesis when in fact it should be accepted. For this reason, the researcher controls for firm size using number of branches and capital structure. Prior scholars found that firm size is positively associated with IFR (Dolinšek and Lutar-Skerbinjek, 2018; Dolinšek et al., 2014 Abdelsalam and El-Masry, 2008). Ashbaugh et al. (1999) noted that economies of scale suggest that large firms are more likely to post-financial reports on web sites. This is because larger firms usually have more products and more complex distribution networks, which require larger and more complex management information systems and databases for management control purposes. In this study, it is expected that largesized firms will disclose their financial performance information on their websites than the small firms. Large financial services firms in Uganda are those that have 20 branches and above (Senyonyi, 2017). There are minimal studies that have linked capital structure with IFR. Studies have documented a positive significant association between capital structure and firm performance (Al-Kayed et al., 2014; Shyu, 2013). Using the data obtained from the Taiwan Economic Journal regarding listed manufacturing firms, capital structure was found to have a significant positive effect on performance in group-affiliated firms. Al-Kayed et al. (2014) found that Islamic banks that use more equity than debt perform better than those that rely on majorly debt financing. In this study, it is expected that capital structure will be associated with IFR.

3. Methodology

3.1 Design, population and sample

This study’s research design is cross-sectional and correlational. The study population is 53 financial services firms (Bank of Uganda, 2017; IRA, 2017). A sample of 47 firms was generated using Yamane’s formula of 1973 that guides sample selection. According to Yamane, sample size is given by n = N/(1+N(e)2 where n is a sample size, N is the total population and e is tolerable error. Based on Yamane’s approach with a total population (N) 53 and tolerable error (e) 5 per cent. Proportionate sampling was employed first to select 21 commercial banks out of 24 and second, to select 26 insurance firms out of 29. This was followed by simple random sampling method without replacement. Of the 47 firms, completed questionnaires were received from 40 firms indicating a response rate of 85 per cent. The response rate was high for a survey of this type considering that previous studies involving such surveys are known to generate lesser percentage response rates. The higher percentage response rate was possible because respondents were given 3 months to complete the questionnaire and several callbacks were made. This study’s unit of analysis was a firm and the unit of inquiry was the Chief Internal Auditors (CIAs) and the Chief Finance Officers (CFOs). For the unit of inquiry, the male respondents were 38 (or about 65 per cent) and the female respondents were 20 (or about 35 per cent). About 62 per cent had completed university education (bachelor’s degree) and 38 per cent had master’s degree. In all, 43 per cent were members to the Institute of Certified Public Accountants of Uganda, 48 per cent were members to Association of Chartered Certified Accountants (ACCA) and 5 per cent were members of other professional bodies. This means that the respondents were able to comprehend the questions asked in the questionnaire and it also implies that chief finance officers and chief internal auditors are professional accountants. In total, 58 per cent of the respondents had a work experience in the same firm for a period of more than five years and this means that they had the necessary experience for this study.

3.2 The questionnaire and measurement of variables

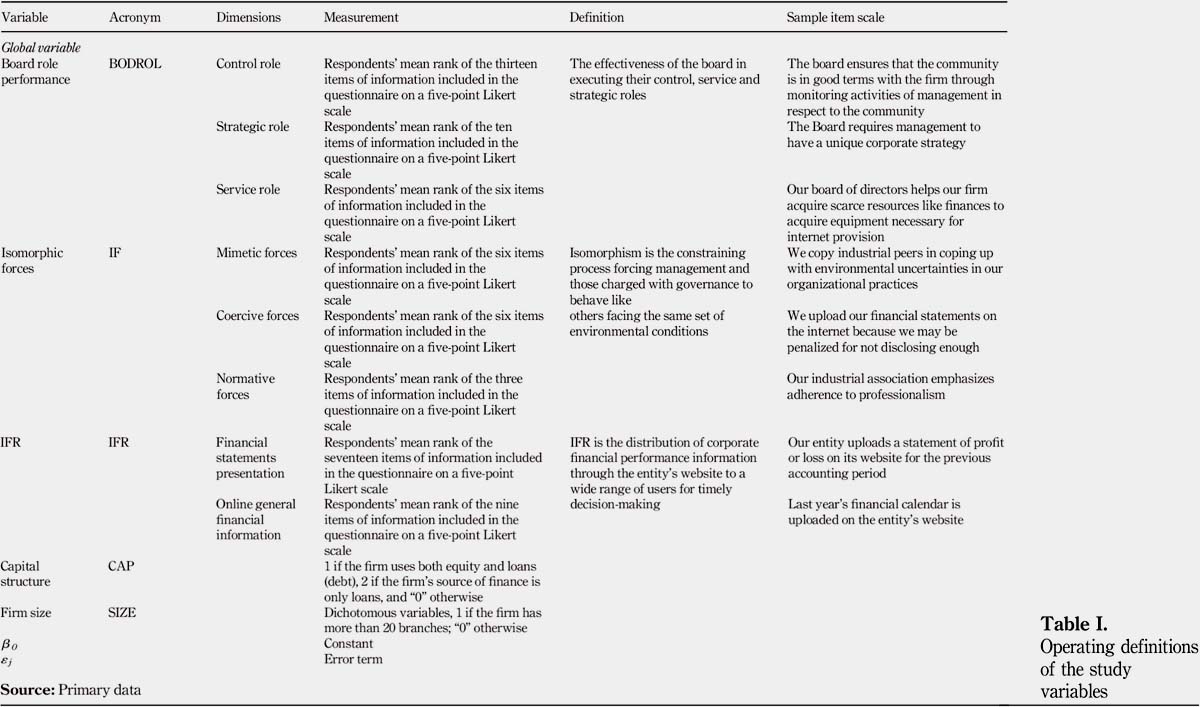

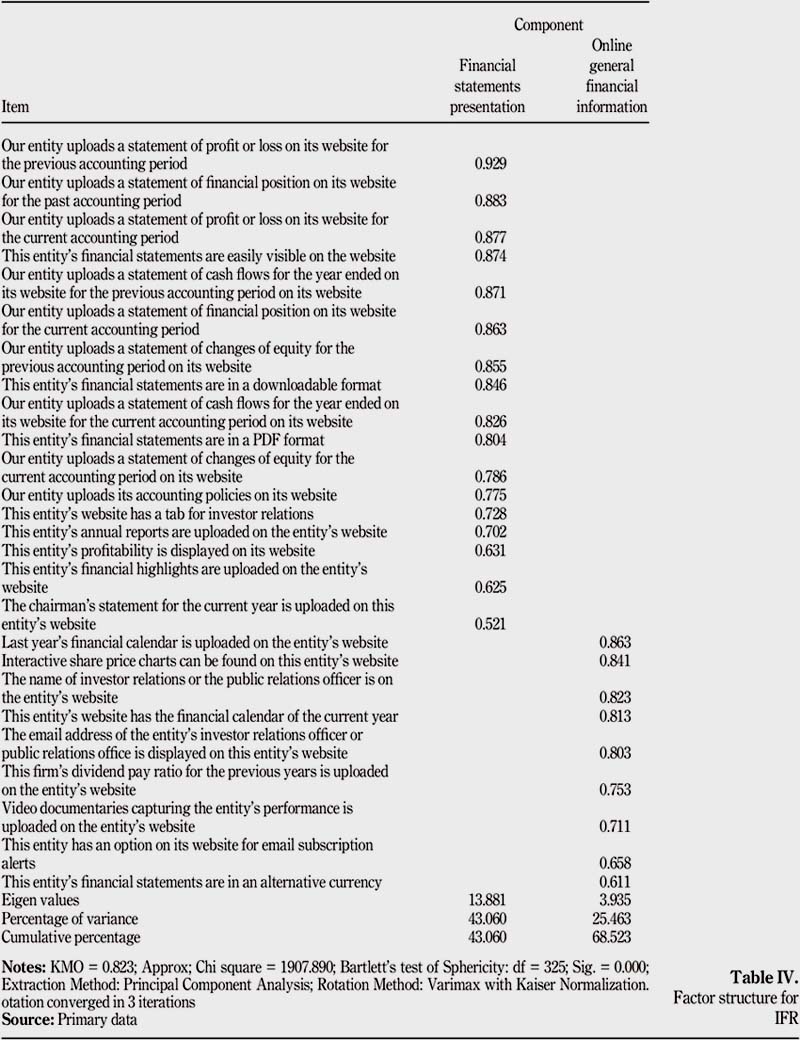

A five-point Likert scale questionnaire ranging from strongly disagree to neutral to strongly agree designed to measure the opinion of a respondent was used. Questionnaires may contain close-ended questions and open-ended questions. According to Sudman and Bradburn (1982), open-ended questionnaires encourage respondents to give their opinion fully and with as much nuance as they are capable. However, this approach was not applicable. This study uses a questionnaire with close-ended questions, as it is aimed at calculating the mean ratings of the extent of agreement with the statements given. The fact that this is the first study to explore the relationship between intellectual capital, isomorphic forces and IFR using perceptions, a questionnaire was considered more appropriate. The questionnaire design is based on reviewing the existing literature on intellectual capital, isomorphic forces and IFR. The dependent variable for this study is IFR. IFR is a function of online general financial information and financial statement presentation (Dolinšek and Lutar-Skerbinjek, 2018; Ahmed et al., 2017; Bin-Ghanem and Ariff, 2016; Dolinšek et al., 2014 Uyar, 2011; Bozcuk et al., 2011; Aly et al., 2010). IFR was operationalized in terms of financial statements presentation and online general financial information. Previous scholars have used disclosure indices to assess IFR but have called for a perception-based study where financial information users’ opinions are sought. In this study, the disclosure indices of scholars such as Dolinšek and Lutar-Skerbinjek (2018), Ahmed et al. (2017), Bin-Ghanem and Ariff (2016), Dolinšek et al. (2014), Uyar (2011), Bozcuk et al. (2011) and Aly et al. (2010) are turned into statements where respondents indicate their degree of agreement with such statements. This approach is helpful in equipping those firms that are not mindful or even aware of IFR to understand what it is all about. Therefore, the perception-based approach plays an important role in disseminating information to management and those charged with governance in those firms that are slow at adoption of IFR. Board role performance was operationalized in terms of control, strategic and service roles and this is in line with previous scholars (Nalukenge et al., 2017; Nkundabanyanga et al., 2014; Nkundabanyanga and Ahiauzu, 2012; Maassen, 1999; Zahra and Pearce, 1989). Isomorphic forces were studied in terms of mimetic, coercive and normative isomorphism/forces (Louw and Maroun, 2017; Nurunnabi, 2017; Nyahas et al., 2017; Aboagye-Otchere and Agbeibor, 2012; DiMaggio and Powell, 1983; Meyer and Rowan, 1977). (Table I)

3.3 Validity and reliability of the research instrument

Content validity index and Cronbach’s (1951) a were used to test the validity and reliability of the scales as measures of the study notions. The overall content validity index for this study is 0.85 while Cronbach’s reliability index for board role performance, isomorphic forces and IFR was 0.950, 0.852 and 0.973, respectively. The results affirm that all the components of the instrument had an acceptable Cronbach’s alpha greater than 0.7 which indicates that the instrument was reliable (Field, 2009; Kline, 1999). To establish convergent validity, the principal components for each variable were extracted by running principal component analysis using Varimax rotation method and factor loadings below 0.5 coefficients were suppressed to avoid extracting factors with weak loadings. Prior to performing the principal component analysis for scales, we assessed the suitability of the data for factor analysis based on sample size adequacy, the Kaiser–Meyer–Olkin (KMO) and Bartlett tests. The results show the KMO values for board role performance, isomorphic forces and IFR are 0.811, 0.678 and 0.823 respectively (Table II-IV). According to Field (2009), the KMO statistic varies between 0 and 1. Field (2009) further explains that a value of 0 indicates that the sum of partial correlations is large relative to the sum of correlations, indicating dispersion in the pattern of correlations (hence, factor analysis is likely to be inappropriate). However, a value close to 1 indicates that patterns of correlations are relatively compact and so factor analysis should yield distinct and reliable factors (Field, 2009). KMO values of 0.5 and above are acceptable. Kaiser (1974) recommends accepting values greater than 0.5 as barely acceptable (values below this should lead the researcher to either collect more data or rethink which variables to include). Furthermore, values between 0.5 and 0.7 are mediocre, values between 0.7 and 0.8 are good, values between 0.8 and 0.9 are great and values above 0.9 are superb (Hutcheson and Sofroniou, 1999). The KMOs for the study variables are all above 0.5 which is acceptable. Bartlett’s test of Sphericity in all scales reached statistical significance (p < 0.05) (significant value was 0.00 for each scale). The major reason for carrying out factor analysis is to reduce the data into a manageable size (Field, 2009).

3.4 The model

The study uses a hierarchical regression model in investigating the contribution of intellectual capital and isomorphic forces on IFR among financial services firms in Uganda. Specifically, the model below was tested:

4. Results

4.1 Descriptive statistics

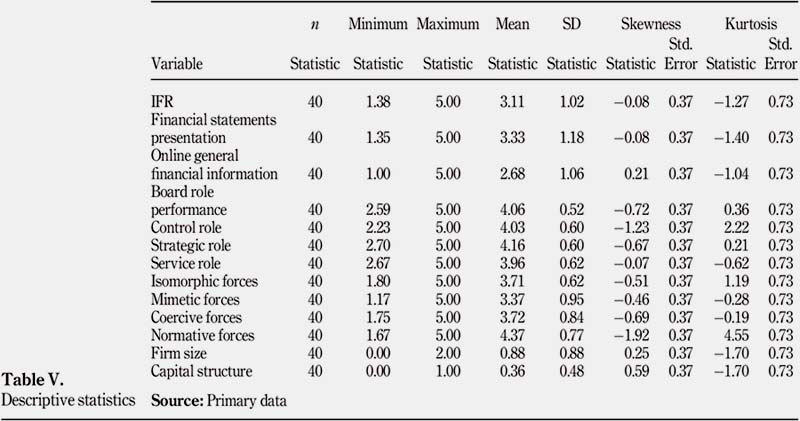

Means and standard deviations were generated to summarize the observed data. These are presented in Table V. The statistics show that the mean rating for the dependent variable (IFR) is 3.11 with a maximum of 5.00 and minimum of 1.38. This implies that the usage of internet in financial reporting is not fully adopted across all financial services firms. The existence of a minimum score of 1.38 implies that there are firms that completely have not yet adopted IFR while the existence of a maximum score of 5 means that there are firms that have adopted IFR. For the independent variables (BODROL and IF), the mean for board role performance is 4.06 with a minimum score of 2.59 and a maximum score of 5. The mean for isomorphic forces is 3.71 while the minimum score is 1.8 and the maximum score is 5. The standard deviations are small as compared to the means especially for the independent variables and this implies that the calculated means highly represent the observed data (Field, 2009; Saunders et al., 2007).

We further present skewness and kurtosis values for assessing normality of the data since Pearson correlation coefficient requires data to be normal. Nkundabanyanga et al. (2014) and Tabachnick and Fidell (2007) maintain that normality of variables enhances the solution and such normality tests are done using measures of variation and specifically skewness and kurtosis whose values should be zero. According to Garson (2012), a skew should be within +2 to -2 range when the data are normally distributed and a skew of +1 to -1 is also acceptable. Garson (2012) further explains that once kurtosis is within the range of +2 to -2, the data set are normally distributed. Field (2009) explains that, normal data will have values of skewness and kurtosis ranging from 3.29 to -3.29. Field (2009) further demonstrates that, positive values of skewness indicate a pile up of scores on the left of the distribution whereas negative values indicate a pile up on the right. Field (2009) further explains that positive values of kurtosis indicate a pointy and heavily tailed distribution, whereas negative values indicate a flat and light-tailed distribution. Table V results indicate that our data set is normally distributed with values falling into the range of 3.29 to -3.29.

4.2 Correlation analysis results

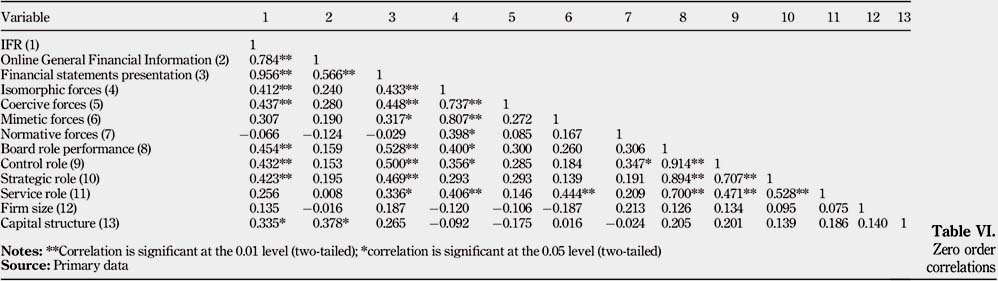

Table VI shows correlation analysis results. The correlation analysis results reveal that board role performance has a significant positive relationship with IFR (r = 0.454**, p < 0.01). This finding implies that a positive change in board role performance will lead to a positive change in IFR. In terms of BODROL constructs, the control and strategic roles of the board are positively and significantly associated with IFR unlike the service role. Further, correlation analysis results reveal that isomorphic forces is positively and significantly associated with IFR (r = 0.412**, p < 0.01). These results confirm H2. For isomorphic forces dimensions of mimetic forces, coercive forces and normative forces, coercive forces are positively and significantly associated with IFR. Mimetic and normative isomorphism are not significantly associated with IFR. For the control variables, capital structure is significantly associated with IFR adoption. We can thus temporarily say our research hypotheses are supported. H1 and H2 are preliminarily supported. Given that correlation analysis results cannot form a basis for the conclusion on whether our hypotheses are supported, we further carry out a regression analysis to confirm our hypotheses.

4.3 Regression analysis results

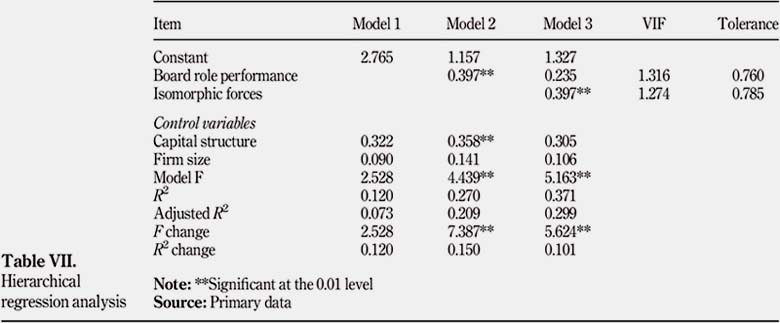

After obtaining preliminary results from the bivariate correlations between the independent and the dependent variable, a regression analysis was run to further substantiate the study hypotheses. Regression results as presented in Table VII indicate that both board role performance and isomorphic forces explain 22.9 per cent of the variance in IFR (Adjusted R2 = 0.229). However, board role performance is a significant predictor of IFR in the absence of isomorphic forces. A hierarchical regression analysis tool was used to establish the contribution of independent variable on IFR. In a hierarchical regression, predictors are selected based on past work and one decides in which order to enter the predictors into the model but most preferably based on their level of importance in predicting the outcome variable (Field, 2009). The hierarchical regression analysis is powerful in testing which independent variable contributes more to the variances in the dependent variable and also indicates the incremental power of an additional independent variable to the already existing variable(s) in explaining the dependent variable (Sekaran, 2003; Field, 2009).

Control variables were therefore entered first (in Model 1) in order to eliminate the noise, they may have in the final model. Model 1 in Table VII is the starting model with only control variables and results indicate that control variables do not explain any significant variance in IFR, and this also means that the research models are not sensitive to confounding factors and the models are highly credible. The standardized β values were used in this study and not the unstandardized β because, the later takes on real values with no common measurement and yet this study had control variables which were measured differently from the study variables. In Model 2, board role performance was entered and found significant (standardised β = 0.397). However, in Model 3, both board role performance and isomorphic forces were entered, and only isomorphic forces were found significant. In the absence of isomorphic forces, board role performance predicts 20.9 per cent of IFR.

5. Discussion

Based on the present study results, both board role performance and isomorphic forces contribute to IFR though in the presence of isomorphic forces, the predictive power of board role performance is subsumed. Under IFR, the following information is expected on an entity’s website:

-

statement of profit or loss for both the current and previous accounting period;

-

statement of financial position for both the current and the previous accounting period;

-

statement of changes in equity for both the current and the previous accounting period;

-

statement of cash flows for both the current and the previous accounting period;

-

financial statements in a downloadable format;

-

financial statements are clearly visible;

-

firm’s accounting policies;

-

firm’s profitability;

-

tab for investor relations;

-

entity’s annual reports;

-

entity’s financial highlights;

-

chairman’s statement for the current year;

-

firm’s financial calendar of the current and previous years;

-

interactive share price charts;

-

video documentaries capturing the entity’s performance;

-

the name and email of the investor relations officer;

-

financial statements in an alternative currency; and

-

option for email subscription alerts.

IFR among financial services firms in Uganda is more associated with board role performance than isomorphic forces. IFR being a new tool for disclosing financial information, it is important that the board performs its roles. According to Maassen (1999) and Zahra and Pearce (1989) board roles are strategic, service and control. These roles need to be performed in order for firms to adopt IFR. Further, the study results in terms of isomorphic forces are in line with those of the previous studies for example, Nyahas et al. (2017) found out that isomorphic forces are positively associated with voluntary disclosures of listed firms in Nigeria. The present results support the notion that external pressures force the organization to adjust its ways of operation and fit into those pressures.

The present study findings signpost that the board is expected to perform control roles such as ensuring the community is good terms with the firm through monitoring management’s activities in respect to the community, monitor the CEO, encourage the idea that no employee or group of employees should be in a position both to perpetrate and to conceal errors or fraud in the normal course of their duties, determining business unit strategies and plans designed to implement the corporate strategy, contributing to strategy development through careful refinement of strategic plans, engaging in activities that link the entity with others through the internet, acquiring scarce resources like finances to acquire equipment necessary for internet provision among others. It should be noted that, management and those charged with governance should ensure that financial statements of the entity are uploaded on the entity’s website since it is a clear indicator that, financial statements have been provided to the public.

Therefore, board role performance and isomorphic forces are critical for improvement of IFR among financial services firms. The results of this study thus make it obvious that once board roles are not performed and management is not mindful of responding to external pressures especially those from clients and regulators, it is possible that IFR among firms will remain low.

6. Summary and conclusion

This paper aimed to establish the contribution of board role performance and isomorphic forces on IFR. To achieve this, a questionnaire survey of 40 financial services firms was used. The Pearson correlation coefficient and ordinary least square multiple regression analysis to analyze the data was used. Results of the study indicate that board role performance and isomorphic forces contribute significantly to IFR to the extent of 23 per cent. The results in this paper are particularly important for several reasons. First, they contribute to existing literature providing initial empirical evidence on the contribution of board role performance and isomorphic forces on IFR. This is important for regulators like the Bank of Uganda and Insurance Regulatory Authority to encourage financial services firms to disseminate financial performance information on their websites. Second, the results suggest to management of financial services firms to respond to pressures from various stakeholders, as this will enable them to enjoy the benefits of adoption of IFR. Finally, the results suggest that the community and other external stakeholders can always demand for financial information via the internet as this helps them in terms of reducing costs of accessing information from the respective financial services.

As with any study, our study has a number of limitations, for example, the study was crosssectional. This implies that changes in behavior over time were not monitored. Further, the study did not allow respondents to freely express their feelings on IFR since the study used close-ended questionnaires. Future studies may focus on other determinants of IFR in emerging economies and elsewhere using perceptions. In addition, the same study may be carried out in other national settings. Future studies may also employ mixed methods design and or a purely qualitative research approach. Nevertheless, the present study provides initial empirical evidence on the contribution of board role performance and isomorphic forces on IFR.

References

Abdelsalam, O. and El-Masry, A. (2008), "The impact of board independence and ownership structure on the timeliness of corporate internet reporting of Irish-listed companies", Managerial Finance, Vol. 34 No. 12, pp. 907-918. [ Links ]

Aboagye-Otchere, F. and Agbeibor, J. (2012), "The international financial reporting standard for small and medium-sized entities (IFRS for SMES): suitability for small businesses in Ghana", Journal of Financial Reporting and Accounting, Vol. 10 No. 2, pp. 190-214. [ Links ]

Ahmed, A.H., Burton, M.B. and Dunne, T.M. (2017), "The determinants of corporate internet reporting in Egypt: an exploratory analysis", Journal of Accounting in Emerging Economies, Vol. 7 No. 1, pp. 35-60. [ Links ]

Al-Kayed, L.T., Zain, S.R.S.M. and Duasa, J. (2014), "The relationship between capital structure and performance of Islamic banks", Journal of Islamic Accounting and Business Research, Vol. 5 No. 2, pp. 158-181. [ Links ]

Aly, D., Simon, J. and Hussainey, K. (2010), "Determinants of corporate internet reporting: evidence from Egypt", Managerial Auditing Journal, Vol. 25 No. 2, pp. 182-202. [ Links ]

Amoako, K.O., Lord, B.R. and Dixon, K. (2017), "Sustainability reporting: insights from the websites of five plants operated by newmont mining corporation", Meditari Accountancy Research, Vol. 25 No. 2, pp. 186-215.

[ Links ]

Ashbaugh, H., Johnstone, K. and Warfield, T.D. (1999), "Corporate reporting on the internet", Accounting Horizons, Vol. 13 No. 3, pp. 241-257. [ Links ]

Ashworth, R., Boyne, G. and Delbridge, R. (2007), "Escape from the iron cage? Organizational change and isomorphic pressures in the public sector", Journal of Public Administration, Research and Theory, Vol. 19 No. 1, pp. 165-187. [ Links ]

Bananuka, J., Kaawaase, T.K., Musimenta, D. and Namusobya, Z. (2018), "A qualitative inquiry into the determinants of internet financial reporting in Uganda", Makerere Business Journal, Vol. 14 Nos 1/2, pp. 88-105. [ Links ]

Bank of Uganda (2017), List of licensed commercial banks as at 13 March 2017, available at: www.bou.or.ug (accessed 13 April 2018). [ Links ]

Bartov, E., Gul, F.A. and Tsui, J.S.L. (2000), "Discretionary-accruals models and audit qualifications", Journal of Accounting and Economics, Vol. 30 No. 3, pp. 421-452. [ Links ]

Belson, D. (2016), Akamai’s state of the internet, Q1 2016 Report, (accessed 29 May 2017).

Bin-Ghanem, H. and Ariff, A.M. (2016), "The effect of board of directors and audit committee effectiveness on internet financial reporting: evidence from Gulf co-operation council countries", Journal of Accounting in Emerging Economies, Vol. 6 No. 4, pp. 429-448. [ Links ]

Botti, L., Boubaker, S., Hamrouni, A. and Solonandrasana, B. (2014), "Corporate governance efficiency and internet financial reporting quality", Review of Accounting and Finance, Vol. 13 No. 1, pp. 43-64.

[ Links ]

Bozcuk, A.E., Aslan, S. and Arzova, S.B. (2011), "Internet financial reporting in Turkey", EuroMed Journal of Business, Vol. 6 No. 3, pp. 313-323.

[ Links ]

Chiang, C. (2010), "Insights into current practices in auditing environmental matter", Managerial Auditing Journal, Vol. 25 No. 9, pp. 912-933. [ Links ]

Cronbach, L.J. (1951), "Coefficient alpha and the internal structure of tests", Psychometrika, Vol. 16 No. 3, pp. 297-334. [ Links ]

Culica, D. and Prezio, E. (2009), "Hospital board infrastructure and functions: the role of governance in financial performance", International Journal of Environmental Research and Public Health, Vol. 6 No. 3, pp. 862-873. [ Links ]

Debreceny, R., Gray, G.L. and Rahman, A. (2002), "The determinants of internet financial reporting", Journal of Accounting and Public Policy, Vol. 21 Nos 4/5, pp. 371-394. [ Links ]

DiMaggio, P.J. and Powell, W.W. (1983), "The iron cage revisited: institutional isomorphism and collective rationality in organizational fields", American Sociological Review, Vol. 48 No. 2, pp. 147-160. [ Links ]

DiMaggio, P.J. and Powell, W.W. (1991), Social Structure, Institutions, and Cultural Goods: The Case of the US Social Theory for a Changing Society, Westview Press, Boulder, CO. [ Links ]

Dingwerth, K. and Pattberg, P. (2009), "World politics and organizational fields: the case of transnational sustainability governance", European Journal of International Relations, Vol. 15 No. 4, pp. 707-744. [ Links ]

Dolinšek, T. and Lutar-Skerbinjek, A. (2018), "Voluntary disclosure of financial information on the internet by large companies in Slovenia", Kybernetes, Vol. 47 No. 3, pp. 458-473.

Dolinšek, T., Tominc, P. and Skerbinjek, A.L. (2014), "The determinants of internet financial reporting in Slovenia", Online Information Review, Vol. 38 No. 7, pp. 842-860.

Eisenberg, M.A. (1997), "The board of directors and internal control. 19 cardozo L. Rev. 237", available at: http://scholarship.law.berkeley.edu/facpubs/364 [ Links ]

Ettredge, M., Richardson, V.J. and Scholz, S. (2002), "Dissemination of information for investors at corporate websites", Journal of Accounting and Public Policy, Vol. 21 Nos 4/5, pp. 357-369.

[ Links ]

FASB (2000), Electronic Distribution of Business Reporting Information, Financial Accounting Standards Board (FASB), New York, NY. [ Links ]

Field, A. (2009), Discovering Statistics Using SPSS, Sage publications, London. [ Links ]

Garson, G.D. (2012), Testing Statistical Assumptions, 2012 ed., Statistical Associates Publishing, Asheboro. [ Links ]

Halme, M. and Huse, M. (1997), "The influence of corporate governance, industry and country factors on environmental reporting", Scandinavian Journal of Management, Vol. 13 No. 2, pp. 137-157.

[ Links ]

He, L., Labelle, R., Piot, C. and Thornton, D.B. (2009), "Board monitoring, audit committee effectiveness, and financial reporting quality: review and synthesis of empirical evidence", Journal of Forensic and Investigative Accounting, Vol. 1 No. 2, pp. 1-41. [ Links ]

Hillman, A. and Dalziel, T. (2003), "Boards of directors and firm performance: integrating agency and resource dependence perspectives", Academy of Management Review, Vol. 28 No. 3, pp. 383-396. [ Links ]

Hoffman, A.J. (1999), "Institutional evolution change: environmentalism and the US chemical industry", Academy of Management Journal, Vol. 42 No. 4, pp. 351-371. [ Links ]

Hutcheson, G. and Sofroniou, N. (1999), The Multivariate Social Scientist, Sage Publications, London. [ Links ]

Internet World Stats (2017), "Internet usage statistics", available at: www.internetworldstats.com/stats.Htm (accessed 22 November 2017). [ Links ]

Insurance Regulatory Authority (2017), "List of Licensed insurance companies for the year 2018", available at: https://ira.go.ug (accessed 31 December 2017).

[ Links ]

Kaiser, H.F. (1974),"An index of factorial simplicity", Psychometrika, Vol. 39 No. 1, pp. 31-36.

[ Links ]

Kessler, E.H. (2013), Encyclopedia of Management Theory, Sage Publications, London. [ Links ]

Kline, P. (1999), The Handbook of Psychological Testing, 2nd ed., Psychology Press, London. [ Links ]

Levrau, A. and Van den Berghe, L. (2007), "Corporate governance and board effectiveness: beyond formalism", Vlerick Leuven Gent Working Paper Series 2007/3. [ Links ]

Louw, A. and Maroun, W. (2017), "Independent monitoring and review functions in a financial reporting context", Meditari Accountancy Research, Vol. 25 No. 2, pp. 268-290. [ Links ]

Maassen, G.F. (1999), An International Comparison of Corporate Governance Models, Spencer Stuart, Amsterdam. [ Links ]

Mellett, H., Marriott, N. and Macniven, L. (2009), "Diffusion of an accounting innovation: fixed asset accounting in the NHS in Wales", European Accounting Review, Vol. 18 No. 4, pp. 745-764. [ Links ]

Meyer, J.W. and Rowan, B. (1977), "Institutionalized ceremonies: formal structure as myth and ceremony", American Journal of Sociology, Vol. 83 No. 2, pp. 340-363. [ Links ]

Michelon, G., Bozzolan, S. and Baretta, S. (2015), "Board monitoring and internal control system disclosure in different regulatory environments", Journal of Applied Accounting Research, Vol. 16 No. 1, pp. 138-164. [ Links ]

Mizruchi, M.S. and Fein, L.C. (1999), "The social construction of organisational knowledge: a study of the uses of coercive, mimetic, and normative isomorphism", Administrative Science Quarterly, Vol. 44 No. 4, pp. 653-683. [ Links ]

Mokhtar, E.S. (2017), "Internet financial reporting determinants: a meta-analytic review", Journal of Financial Reporting and Accounting, Vol. 15 No. 1, pp. 116-154. [ Links ]

Nalukenge, I., Tauringana, V. and Mpeera Ntayi, J. (2017), "Corporate governance and internal controls over financial reporting in Ugandan MFIs", Journal of Accounting in Emerging Economies, Vol. 7 No. 3, pp. 294-317. [ Links ]

Nkundabanyanga, S. and Ahiauzu, A. (2012), "Board role performance in Uganda’s services sector firms", Journal of Public Administration and Policy Research, Vol. 4 No. 5, pp. 115-124.

Nkundabanyanga, K.S., Balunywa, W., Tauringana, V. and Ntayi, J. (2014), "Board role performance in service organisations: the importance of human capital in the context of a developing country", Social Responsibility Journal, Vol. 10 No. 4, pp. 646-673. [ Links ]

Nurunnabi, M. (2017), "Auditors’ perceptions of the implementation of international financial reporting standards (IFRS) in a developing country", Journal of Accounting in Emerging Economies, Vol. 7 No. 1, pp. 108-133.

Nyahas, S.I., Munene, J.C., Orobia, L. and Kaawaase, T.K. (2017), "Isomorphic influences and voluntary disclosure: the mediating role of organizational culture", Cogent Business and Management, Vol. 2017 No. 4, pp. 1-18. [ Links ]

Pearce, J.A. and Zahra, S.A. (1991), "The relative power of GEOs and boards of directors: associations with corporate performance", Strategic Management Journal, Vol. 12 No. 2, pp. 135-153. [ Links ]

Peasnell, P., Pope, P. and Young, S. (2005), "Board monitoring and earnings management: do outside directors’ influence abnormal accruals?", Journal of Business Finance and Accounting, Vol. 32 Nos 7/8, pp. 1311-1346.

Purba, L., Medyawati, H., Silfianti, W. and Hermana, B. (2013), "Internet financial reporting index analysis: an overview from the state-owned enterprises in Indonesia", Journal of Economics, Business and Management, Vol. 1 No. 3, pp. 281-284. [ Links ]

Rogers, E.M. (1995), Diffusion of Innovation, 4th ed., Free Press, New York, NY. [ Links ]

Rogers, E.M. (2003), Diffusion of Innovations, 5th ed., Free Press, New York, NY. [ Links ]

Sahin, I. (2006), "Detailed review of rogers’ diffusion of innovations theory and educational technologyrelated studies based on rogers’ theory", The Turkish Online Journal of Educational Technology, Vol. 5 No. 2, available at: http://files.eric.ed.gov/fulltext/ED501453.pdf

Saunders, M., Lewis, P. and Thornhill, A. (2007), Research Methods for Business Students, FT/PrenticeHall, London. [ Links ]

Sekaran, U. (2003), Research Methods for Business, John Willey and Sons, New York, NY. [ Links ]

Senyonyi, T.W. (2017), Exclusive: Uganda’s Largest Banks by Assets Revealed, Business focus, Kampala.

Shyu, J. (2013), "Ownership structure, capital structure, and performance of group affiliation: evidence from Taiwanese group-affiliated firms", Managerial Finance, Vol. 39 No. 4, pp. 404-420. [ Links ]

Siala, H.G., Sellami, Y.M. and Fendri, H.B. (2014), "Determinants of voluntary web-based disclosure: a comparison of the United Kingdom and its former colony, New Zealand", International Journal of Accounting and Economics Studies, Vol. 2 No. 2, pp. 100-110. [ Links ]

Sudman, S. and Bradburn, N.M. (1982), Asking Questions: A Practical Guide to Questionnaire Design, 3rd ed., Jossey-Bass, San Francisco, CA. [ Links ]

Tabachnick, B.G. and Fidell, L.S. (2007), Using Multivariate Statistics, 4th ed., Allyn and Bacon, Needham Heights, MA. [ Links ]

Uyar, A. (2011),"Determinants of corporate reporting on the internet: an analysis of companies listed on the Istanbul stock exchange (ISE)", Managerial Auditing Journal, Vol. 27 No. 1, pp. 87-104. [ Links ]

Vicknair, D., Hickman, K. and Carnes, K.C. (1993), "A note on audit committee independence: evidence from the NYSE on ‘grey’ area directors", Accounting Horizons, Vol. 7 No. 1, pp. 53-57.

Xiao, J.Z., Yang, H. and Chow, C.W. (2004), "The determinants and characteristics of voluntary internetbased disclosures by listed Chinese companies", Journal of Accounting and Public Policy, Vol. 23 No. 3, pp. 191-225. [ Links ]

Zahra, S.A. and Pearce, J.A. (1989), "Board of directors and corporate financial performance: a review and integrative model", Journal of Financial Management, Vol. 15, pp. 291-334. [ Links ]

Further reading

Financial Institutions Act (2016), The Uganda Gazette, Vol. CIX No. 6, Entebbe.

Krejcie, R.V. and Morgan, D.W. (1970), "Determining sample size for research activities", Educational and Psychological Measurement, Vol. 30 No. 3, pp. 607-610.

Citation

Bananuka, J., Night, S., Ngoma, M. and Najjemba, G. (2019), "Internet financial reporting adoption: Exploring the influence of board role performance and isomorphic forces", Journal of Economics, Finance and Administrative Science, Vol. 24 No. 48, pp. 266-287. https://doi.org/10.1108/JEFAS-11-2018-0120

Received: 24 November 2018

Accepted: 27 November 2018