Services on Demand

Journal

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

-

Cited by SciELO

Cited by SciELO

Related links

-

Similars in

SciELO

Similars in

SciELO

Share

Permalink

PermalinkJournal of Economics, Finance and Administrative Science

Print version ISSN 2077-1886

Journal of Economics, Finance and Administrative Science vol.24 no.48 Lima July/Dic. 2019

http://dx.doi.org/https://doi.org/10.1108/JEFAS-04-2018-0032

ARTICLE

"Fool me once, …": deception, morality and self-regeneration in decentralized markets

Orlando Gomes1

João Frade1

1Instituto Politecnico de Lisboa, Instituto Superior de Contabilidade e Administracao de Lisboa, Lisboa, Portugal

Corresponding author: *omgomes@iscal.ipl.pt

Abstract

Purpose: This paper aims to provide an overall review and assessment of the virtues and flaws of decentralized self-regulated markets, discussing in particular the extent to which deceiving attitudes by some market participants might be potentially diluted and contradicted.

Design/methodology/approach: To approach deception and morality in markets, the paper follows two paths. First, the relevant recent literature on the theme is reviewed, examined and debated, and second, one constructs a simulation model equipped with the required elements to discuss the immediate and long-term impacts of deceiving behaviour over market outcomes.

Findings: The discussion and the model allow for highlighting the main drivers of the purchasing decisions of consumers and for evaluating how they react to manipulating behaviour by firms in the market. Agents pursuing short-run gains through unfair market practices are likely to be punished as fooled agents spread the word about the malpractices they were allegedly subject to.

Research limitations/implications: Markets are complex entities, where large numbers of individual agents typically establish local and direct contact with one another. These agents differ in many respects and interact in unpredictable ways. Assembling a concise model capable of addressing such complexity is a difficult task. The framework proposed in this paper points in the intended direction.

Originality/value: The debate in this paper contributes to a stronger perception on the mechanisms that attribute robustness and vitality to markets.

Keywords: Markets, Deception, Morality, Purchasing decisions, Preferences, Rumour spreading

Introduction

Markets are one of the most robust forces in nature and society. Even after the most calamitous tragedy, market relations will recover with an exceptional vitality as individuals engage again in trading relations that are crucial for their survival and wellbeing. To gain the confidence of the other players, market participants must avoid dishonest and deceiving attitudes, and therefore, one might infer that stable and long-lasting market equilibrium is inseparable from morality and honesty. Nevertheless, as insistently pointed out by non-orthodox thinking in economics, equilibrium is more an exception than the rule, implying that in many market circumstances, manipulation and deception might pay off. The aim of this paper is to discuss first through a brief literature review and second by assembling a straightforward simulation model, the ability markets have to self-regenerate, albeit they are systematically hit by individual behaviour that disrupts confidence and trustworthiness.

Fool me once, shame on you; fool me twice, shame on me. From the perspective of market interactions, this popular saying reflects well the kind of defences markets possess to self-regulate and to regenerate themselves. Often, people are tempted to pursue unfair and deceiving trading practices, especially in the absence of strong regulation and enforcement of penalties by the proper authorities. But markets have the capacity to circumvent less honourable and righteous practices, namely, when the trade relation allows for repeated interaction. Transactions presuppose mutual gain, and this implies that those willing to trade with us expect us to have a fair behaviour and vice-versa. Reciprocity will imply that honest behaviour is a stable equilibrium toward which the market outcome is likely to converge. In this sense, deception may be viewed as a disturbance or an anomaly that eventually sets in particular circumstances, which might repeat themselves with a relatively high frequency (e.g. when an inexperienced player enters the market or when someone forgets how she was fooled sometime in the past).

Some recent literature (Akerlof and Shiller, 2016; Basu, 2016; Perri, 2016) points out that uneven and unfair market relations are pervasive; in fact, they become in many cases the rule rather than the exception. If people consume goods that are bad to their health, or if they spend more than what they will be able to pay without compromising their future well-being, it is because they are lured to act in that way. Impulses, urges and emotions which are inseparable from human nature are often perceived by market players as vulnerabilities that are available to be exploited. For instance, people’s choices are susceptible to intertemporal inconsistences (preferences are contingent on temporal distance) and this is the reason why an individual may accept today a financial deal that brings an immediate reward but that implies relevant future discommodities.

Rationality, taken to the extreme, appears to have a dark side. Rational agents in the market are focussed on pursuing their own interests, sometimes taking to the limit their will to persuade others. Firms spend large sums of money in marketing and advertising, and although these are useful activities, in the sense, they allow for the dissemination of information about the attributes of the goods and services firms sell, they are many times used as an instrument to exploit the emotional vulnerabilities and weaknesses of people. Markets are, in this perspective, an uneven platform of interaction where some players act as ruthless optimizers, while others are caught off guard being at the mercy of those endowed with the ability to control and manipulate. This view takes us away from the idea of markets as instruments that promote economic and social harmony, i.e. as entities where equilibrium outcomes are the inevitable consequence of the self-interested behaviour of all the participants.

The paper discusses the extent of manipulation practices in a wide array of markets, the capacity they have to self-regenerate and the evolutionary nature of the market participants. This is done by pursuing, in a first moment, a general discussion and literature review on the pros and cons of free market relations (second section). In the second stage, a simulation model is assembled to highlight and explore the dynamics of deception, morality and self-regeneration in markets. Rational and emotional determinants of purchasing decisions are systematized (third section); transmission channels of manipulation over the motivation to buy are put into perspective (fourth section); and natural and intuitive defence mechanisms that balance market relations, as morality, empathy and sympathy, are equated (fifth section). All the mentioned features are put together in a modelling structure that allows, through simulation, to identify trends concerning the survival and expansion of firms and the changes on consumer preferences. The final section concludes.

Markets: dangerous arenas or cooperation forums?

To reflect on the intrinsic and general properties of markets is a first fundamental step in the effort to understand how they benefit or penalize those who engage in exchange relations. An influential perspective on the nature of markets is Friedrich von Hayek’s view about spontaneous orders. Bowles et al. (2017) reminisce that Hayek interpreted markets as complex systems where individuals endowed with a limited knowledge on the structure and dynamics of the market would compete to serve their own interests, allowing for the emergence of a coherent whole. In this view, markets need no regulation because free enterprise would be the best form to coordinate individual actions in a large scale.

Markets have the ability to self-regulate because events that affect business relations, although perceived only by few in a first moment, rapidly propagate through bargaining mechanisms and the respective adjustment in prices. Although individuals have no capacity to take a comprehensive view over markets, their fields of vision sufficiently overlap, meaning that all relevant information ends up by being communicated to all.

Hayek’s view is consistent with an agent-based approach to market dynamics, as the one we will sketch later in the paper. This approach takes agent heterogeneity and decentralized interaction to simulate aggregate outcomes. In this type of models, as in observable market relations, markets do not converge to equilibrium positions. Disequilibria tend to persist. Systematic learning and diffusion place the economy in a state of recurrent evolution.

Besides the dominance of out-of-equilibrium outcomes, another fundamental feature of the dynamics of markets is the heterogeneity of agents, given the position they momentarily occupy. Markets are uneven and heterogeneous by nature. Agents may enter the market with different degrees of information and perception of market conditions and, therefore, perform identical transactions accepting different deals[1].

Since the seminal work of Akerlof (1970) on asymmetric information, many economists believe that the main issues one should worry about when dealing with market anomalies are those related with the position’s agents occupy and that make them have access to a higher or lower degree of information. Signalling and screening are two forms of approaching the information asymmetries problem. Signalling concerns, the process through which the informed party provides relevant information for the decision screening is associated with the idea of searching for the required information. Dosis (2016) proves that in a strategic interaction scenario, the combination of signalling and screening may allow to find an efficient equilibrium result.

Despite the importance of asymmetric information, however, there are other profound problems in the functioning of markets, with less straightforward solutions. In Akerlof and Shiller (2016), a systematic enumeration of situations of manipulation and deception in markets are identified and described. The main strong idea of the "phishing for fools" arguments of these authors is that agents, in the particular context of a market relation, may assume one of two roles: some agents are vulnerable and gullible, while others are hyper-rational and able to impose their perspective on others. The position of agents is contingent on personality traits and transaction scenarios: in some circumstances, the same individual may be susceptible to be taken as a fool, while in other settings, he/she can be the agent better equipped to take advantage of the transaction.

It is frequent to find an explosive combination of gullible behaviour of unearned buyers and optimality-oriented and self-centred attitude of those who produce and sell (although the opposite may also be true). But market relations are not necessarily a zero-sum game where those who have the ability to deceive win at the expenses of the vulnerable and distracted. Frequently, the forces in the market better equipped to act upon it have advantage in behaving righteously, altruistically and obeying to moral principles. This creates an environment of trust and confidence that fosters business relations. Furthermore, even when manipulation and deception may have undisputable economic advantages, agents may disregard such advantage if their actions are guided by moral principles that prevent them from cheating others.

As suggested by Basu (2016), it would be interesting to analyse market relations considering three types of agents: the deceivers, those susceptible of being deceived, and those who behave as guardians of morality, even when this morality does not allow to maximize economic gains. A model with these features would necessarily be an evolutionary framework, where agents could transcend from an eventual state of neutrality to any of the categories highlighted above and where agents might also change positions as trade circumstances are modified (e.g. someone who is vulnerable may evolve to a position of market predator as she learns with experience). The formalization of a theory of market relations and of decision-making with these features, where individual agents are endowed with distinct abilities to develop business transactions, could allow for important insights to understand how agent heterogeneity leads to the formation of prices and to the fulfilment of transactions that depart from standard market results. It is in this direction that the model to construct in the next sections will proceed.

A "phishing for fools" theory, designed over the just described guidelines, must be pervasive and general, but it should also account for the diversity and specificity of markets. For instance, financial markets have their own specificities, and manipulation and deception may acquire, in these, unique features. In fact, finance is a field where market anomalies have been thoroughly studied (Ramiah and Moosa, 2015). In financial markets, it is clear that agents do not always act rationally, adopting heuristics and being subject to biases. There is a wide range of possible deviations from rational behaviour that a detailed and careful analysis of this kind of markets should consider, from herding behaviour to loss aversion, conservatism and others.

By developing a theory of manipulation and deception, economists must also account for the respective policy implications. The main question, according to Basu (2016), is whether it is possible to design an institution capable of guaranteeing that manipulation and deception are corrected without harming efficiency. Moreover, regulatory institutions are not immune to manipulation themselves, and their existence and interference might lead to outcomes where the distortion is stronger than the one provoked by market participants when these do not follow elementary rules of social conduct.

Deception in markets is not a linear reality. As Gruss and Piotti (2010) highlight, deception is related to the distortion or manipulation of the reality with the intention of making people to act in ways that are not beneficial to their own interests. According with the mentioned authors, two forms of deception may emerge:

1. strategic deception, which arises from the opportunistic nature of people; and

2. deception emerging from rationality failures, which can be associated to the idea of self-deception.

This last kind of deception is in part explained by psychological factors, although it is also socially determined; often, people adopt behaviours in markets that are harmful to themselves to comply with some informal social norms (e.g. when someone chooses to smoke to be accepted by a group of people).

In fact, self-deception is an important human trace, with important implications for market relations (Gerschlager, 2007). People might be disappointed with market outcomes because they always expect their own interests to be fulfilled. People conceive, for themselves, the most favourable scenarios, but these do not necessarily occur; as a result, self-deception becomes relevant and it conditions decisions and actions. There might exist a gap between human ambitions and human capabilities, which leads to self-deception and frustration in market transactions, what may be as harmful for the functioning of the markets as manipulation from a third party.

Economics and the analysis of markets are based on the idea of self-interest: people do what best serves their own interests. Does this mean that people are not driven by moral values and altruism? Zak (2011) argues that the two things are not incompatible. It is possible to pursue individual interests and simultaneously to follow a righteous moral conduct. The view of this author is that market exchange requires morality, and that markets reinforce morality. Morality is required for market relations because these are expected to be win-win situations, where all the involved parties draw some benefit. Excessive greed hinders trade. Morality arises naturally because people seek honesty and trustworthiness and avoid dishonest behaviour. In short, moral values facilitate exchange.

One important issue is whether morality can be measured and how it can be incorporated in economic models. For instance, the utility function in the standard intertemporal optimization model might be modified to include concern with others. Empathy can be translated in a utility function where the consumption of others is an argument of the individual function. While some moral values are universal, others are contingent on the specific social scenario in which economic relations take place. In any case, moral behaviour is a natural mechanism of imposing fair market relations knowing that the alternative would be large enforcement costs.

Altruistic behaviour, although absent from conventional economic theory, is an important feature of human action. Moreover, altruism may have an evolutionary advantage; societies where altruistic behaviour dominates may more easily build and maintain the institutions required to thrive and guarantee prosperity (Manner and Gowdy, 2010). Free riding and the tragedy of the commons are less intense problems where altruistic punishment is strong. Altruistic punishment is related to the sacrifices people are willing to make to punish those who do not comply with accepted norms of behaviour.

The notion that morality is essential to economic relations to thrive goes back to Adam Smith’s Theory of Moral Sentiments (White, 2010; Paganelli, 2010; Witztum, 2010). Because trade means interacting with strangers, it facilitates moral development: relatively to strangers, one has to establish a kind of relation where emotions are contained. The invisible hand exists and has a coordinating power that allows for the division of labour and for the interdependency among strangers.

The main conclusion, when observing how people effectively act in business transactions, is that although actions of agents are primarily driven by self-interest, individuals are in no circumstance completely amoral. They experience moral emotions that regulate their behaviour. Such moral emotions include guilt and virtue. Actions that benefit others tend to be self-reinforced in the spirit of individuals, as they are perceived as virtuous. Actions that harm others are actions that individuals refrain to take as they may experience guilt. These ideas might be incorporated in an economic model to address the extent to which moral sentiments may influence behaviour and welfare (Kaplow and Shavell, 2007).

To close this section, we mention three additional notes that are relevant for the discussion on the perils of free markets:

1. Unregulated markets, even if admittedly non-manipulated, may generate extreme unfair results. Kaplan and Rauh (2013) discuss the impact of strong income concentration in global markets. Top earners obtain rents from their global reach that are becoming progressively higher. Markets have many subtleties that must be carefully weighted. One strong idea is that markets are not fair in the way they distribute income. Some people, because of the position they occupy, because of their natural talents or because they were capable to contribute with a relevant innovation, tend to concentrate income. Inequalities in market income generation are a relevant topic of analysis that should be carefully addressed and correlated with eventual deceiving behaviour.

2. Are aggressive marketing and advertising strategies necessarily harmful for less skilful or prepared market participants? Not necessarily. Lindstrom (2008) argues that the more consumers know about the tactics of advertisers the better they will be able to react to them; there is a process of learning through contacting with advertising. Moreover, market studies are important for firms to explore the desires and needs of people, which is not necessarily bad because this may help firms in producing and delivering to the market the goods and services that people enjoy, need and want to buy.

3. Brands, labels and certification are means through which information in markets might be increased, which allows for improved competition and less potential manipulation, and thus, they also bring benefits for all market participants. Bonroy and Constantatos (2015) argue that labelling may have some undesirable side effects over market competition. They might allow for increased transparency, but they can also promote market concentration and some possible predatory lobbying favouring those with a stronger position in the market. A labelling system must be credible and efficient to avoid possible distortions. Labelling is one of the possible mechanisms to fight manipulation and deception, although in an economy with weak institutions, the opposite may indeed occur.

Drivers of individual purchasing decisions: price and variety matching

Markets are complex systems with multiple heterogeneous agents engaging in systematic interactions. Thus, as suggested by Bowles et al. (2017), agent-based computational models might constitute an adequate framework to approach market dynamics, when one wants to account for deceit, morality, gullibility, sympathy and related phenomena. Zhang and Zhang (2007) propose a model of this kind, where a motivation function for purchasing a variety of a good is presented. Motivation to buy depends on the price, on the preference for a given variety, on advertising and on the influence exerted by other consumers. Price and a matching with the intended variety are the structural factors leading an agent to acquire some good from a given firm, suggestion or manipulation through advertising or other factors might distort the expected outcome. Once eventual deceit is perceived, consumers and other market players may penalize the firms that do not follow a correct conduct both directly and by influencing the decisions of other consumers.

The first step in assembling our market interaction model consists in building a motivation function, i.e. a function through which a given consumer i evaluates conditions offered by suppliers and selects the firm from which to buy the good. The motivation function to consider will be inspired in the reasoning presented by Zhang and Zhang (2007) where, as mentioned above, four main determinants of purchasing decisions are assumed: price, quality matching, advertising intensity and the influence of others. We modify this original motivation function by taking, besides price and quality matching, a purchasing driver attached to the propensity of firms to manipulate and deceive and another purchasing driver linked with how society (the other consumers) react to deceiving behaviour.

Consider that at a given time moment, J firms are present in the market, and that each firm j = 1, 2,…, J supplies a different variety of the good. The motivation function of consumer i, at date t, regarding the variety of the good supplied by firm j, will be:

In equation (1), Pj(t) is the price of variety j at date t, Qj(t) is a measure of the qualitative features of the variety j, Dj(t) quantifies the extent in which firm j acts with the objective of manipulating consumer i and Sj(t) stands for the degree of disapproval of other consumers about hypothetical dishonest practices by suppliers. The variables denoted by Greek letters represent the sensitivity of an individual’s choice to each of the purchasing motivation determinants mentioned above.

The purchasing decision of consumer i is undertaken after evaluation of equation (1) for each of the available suppliers. The chosen j corresponds to the firm for which condition  is satisfied. Firms which sell more are those for which the presented condition is met more frequently given the array of assumed consumers.

is satisfied. Firms which sell more are those for which the presented condition is met more frequently given the array of assumed consumers.

Next, we must characterize each element of equation (1). Let us start by assuming that the price is given by the following standard mark-up rule:

Value η < 0 is the reciprocal of the price elasticity of demand and CMj(t) stands for the marginal cost, which is assumed to be an inverse function of productivity. Productivity, in turn, varies across firms, but, for reasons of simplification, it is considered to be constant over time (and randomly assigned to firms). Letting Θj represent productivity, we take  . In this specification, the price charged by each firm remains constant over time, given that marginal costs are also constant, but different productivity levels imply different prices across firms.

. In this specification, the price charged by each firm remains constant over time, given that marginal costs are also constant, but different productivity levels imply different prices across firms.

The term translating consumer’s price sensitivity to variety j is adapted from a similar expression in Zhang and Zhang (2007) and takes the form:

with α > 1, ki > 0 and â > 0; Pe is the expected price of the good. Note that  must be negative, because the motivation to buy necessarily falls with a higher price. Parameter k will possibly possess different values for different consumers, which reflects their heterogeneity, in this case regarding their socio-economic status; a larger k will indicate that people are less sensitive to price (e.g. rich individuals will be less sensitive to price). The expected price might be conceived as the average of the prices of all varieties, which is also constant:

must be negative, because the motivation to buy necessarily falls with a higher price. Parameter k will possibly possess different values for different consumers, which reflects their heterogeneity, in this case regarding their socio-economic status; a larger k will indicate that people are less sensitive to price (e.g. rich individuals will be less sensitive to price). The expected price might be conceived as the average of the prices of all varieties, which is also constant:

Note that under the chosen specification, the price term in the motivation equation  is constant over time basically because of the constant over time productivity, although it varies across firms, also because they are endowed with distinct productivity levels; it also varies across consumers because of different price sensitivity values.

is constant over time basically because of the constant over time productivity, although it varies across firms, also because they are endowed with distinct productivity levels; it also varies across consumers because of different price sensitivity values.

Consider an illustrative example where 100 consumers are in the market and eight firms supply the good. Take the following admissible parameter values: η= −0.75, z = 0.25, α = 1.25, â = 0.01 and assume that the array of productivity levels of firms is such that θj+1 = θj × (1.02), with θ1 = 1. The sensitivity of individuals to price will be randomly given by an exponential distribution[2]; the parameter of the distribution is set at λ= 20 (the higher the value of this parameter, the more high values of k depart from the average value).

In this purely static setting, where the price is the only motivating force for purchasing the good, every consumer will select firm j = 8 to materialize the purchase, as this is the firm with the highest productivity and, thus, the firm that is able to sell at the lowest price. Although sensitivity to price matters, rational consumers will always select the lowest price, when this is the single criteria involved in the purchasing decision. A simulation exercise allows to find, in our 100 consumers’ environment, a minimum value of k equal to 5.0584 × 10−8 and a maximum value of 15.9684; for these, Φ8P8 = −0.8583 in the first case and Φ8P8 = −0.7193 in the second case; although the motivation to buy is lower in the first case (the consumer is more sensitive to price, because her income is lower); in both cases, the choice of firm j = 8 is the best choice.

Thus far, purchasing decision is rather simple. Only price matters, and consumers pick the firm with the lowest marginal cost to buy the good, as this is the one delivering it to the market at the lowest price. We now introduce a second relevant term of the motivation equation, which is the one regarding the matching between the preferences of the consumer and the variety supplied by each firm. Assume that all varieties of the good are equally good from a qualitative point of view and normalize Qj(t) = 1, ∀j. Varieties are not indifferent to the consumer because they have different tastes or preferences; let preferences be defined in the interval (0,1) and let ρi(t) be a random variable quantifying these preferences; let also σj(t) be the quality index of the variety in the same interval. The quality sensitivity to variety j is, then, measured by the following term:

with β є (0,1) and ℓ є R a calibrating parameter. Because β is lower than 1, the better the match between preferences and what the firm has to offer, the larger will be the value of  and, thus, the stronger the motivation to adhere to the purchase of this variety.

and, thus, the stronger the motivation to adhere to the purchase of this variety.

In the presence of constant preferences and constant variety supply, value  will not change over time. If we ignore the manipulation and morality components of the problem, we have, so far, a static problem where only price and preferences matter for the choice of the consumer.

will not change over time. If we ignore the manipulation and morality components of the problem, we have, so far, a static problem where only price and preferences matter for the choice of the consumer.

Recover the price example. We now add to this example the variety-preferences deliberation. Assume, for the sake of simplicity, a good that is identical in every possible characteristic except colour (for example, a toothbrush or a personal agenda). Take the RGB colour code, which generates a wide array of colours by combining red, green and blue in tones that can be classified in the integers range from 0 to 255. In this system, 16,777,216 possible colours can be generated. Assume that the eight existing firms produce the good with a different RGB colour, and that the available colours are: black (firm j = 1), RGB = (0,0,0); white (firm j = 2), RGB = (255, 255, 255); red (firm j = 3), RGB = (255, 0, 0); green (firm j = 4), RGB = (0, 255, 0); blue (firm j = 5), RGB = (0, 0, 255); yellow (firm j = 6), RGB = (255, 255, 0); cyan (firm j = 9), RGB = (0, 255, 255); and magenta (firm j = 10), RGB = (255, 0, 255). Consumers, in turn, will have preferences uniformly distributed over the whole pallet of possible colours, and they will choose the supplied colour that is closer to their preferences. Consider that the difference between preferences and available varieties is expressed in the interval (0, 1) according to the following equation:

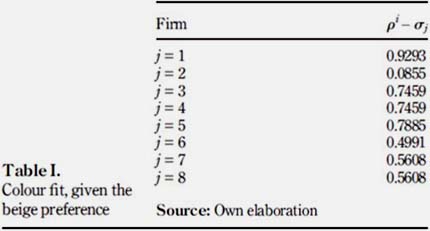

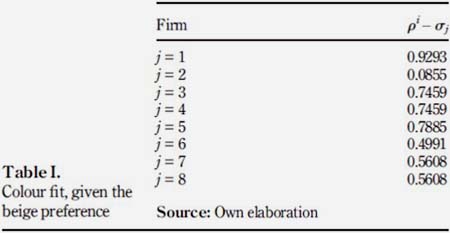

where  represent the red, green, blue preferences, respectively, and σR, σG, σB represent the red, green, blue varieties, respectively. Given equation (6), if a consumer prefers white and firm j supplies white, then │ρi – σj│ = 0; if the same consumer is faced with a firm supplying black, then │ρi – σj│ = 1. Consider a less extreme example, where the consumer prefers a light beige RGB = (245, 245, 220). Table I indicates the value of the term in equation (6) that reflects matching with what each firm supplies.

represent the red, green, blue preferences, respectively, and σR, σG, σB represent the red, green, blue varieties, respectively. Given equation (6), if a consumer prefers white and firm j supplies white, then │ρi – σj│ = 0; if the same consumer is faced with a firm supplying black, then │ρi – σj│ = 1. Consider a less extreme example, where the consumer prefers a light beige RGB = (245, 245, 220). Table I indicates the value of the term in equation (6) that reflects matching with what each firm supplies.

Because one is searching for the minimal distance between preferences and available varieties, Table I clearly indicates that the best consumer choice is to buy white, and that, at some distance, the second-best option is yellow, the two colours closer to the manifested preference.

Let β = 0.5 and ℓ = –0.75; with these values,  i.e. when the intended colour is exactly the one supplied by the firm, the motivation to buy is positive and adds a value of 0.25 to the motivation function; if the supplied colour is the exact opposite of the preferred one, then the motivation to buy receives a negative contribution of −0.25.

i.e. when the intended colour is exactly the one supplied by the firm, the motivation to buy is positive and adds a value of 0.25 to the motivation function; if the supplied colour is the exact opposite of the preferred one, then the motivation to buy receives a negative contribution of −0.25.

Return to the simulation exercise. Now, the price is not the only seller selection criterion. Choices are also driven by preferences. This disturbs the outcome, making some buyers to choose other than the cheapest variety. Table II presents the obtained results for ten simulations (recall that results differ because there is a couple of random variables, namely, the price sensitivity k, and the consumer preference index, ρi).

Table II highlights the relevance of price in the choice of consumers, with the cheapest varieties being the ones with higher demand; nevertheless, preferences and variety matching obscure the price effect as in every case, there are consumers willing to buy the most expensive variety given their strongest preference for it: if consumers want black, they may end up buying black even if this is the most expensive variety of the good.

Not so fair play: business manipulation and deception

So far, by maintaining productivity, preferences and production technologies constant, our analysis of the motivation to buy is static. We now introduce dynamics by attaching the main idea of our analysis: the possibility of manipulation by firms and, posteriorly, moral behaviour by consumers.

Imagine that at period t, a given firm j adopts a manipulating behaviour (Dj(t) = 1), while the others maintain the fair play (Dj(t) = 0). This will imply, in the short-run, that consumers will be artificially more motivated to purchase that variety of the good. In moment t, the agent is receptive to the new information received, and its sensitivity parameter will take a value  We assume that deception continues to have an effect and grows over the next periods, but at a given point in time, the consumer perceives that he/she is being manipulated, and as a result, the value of the sensitivity parameter sharply declines to negative values: under the principle fool me once shame on you, fool me twice shame on me, the attempt to maintain the deceiving behaviour will not have everlasting effects. Over time, and after the negative reaction to manipulation, the consumer will progressively forget the deceiving behaviour and the value of

We assume that deception continues to have an effect and grows over the next periods, but at a given point in time, the consumer perceives that he/she is being manipulated, and as a result, the value of the sensitivity parameter sharply declines to negative values: under the principle fool me once shame on you, fool me twice shame on me, the attempt to maintain the deceiving behaviour will not have everlasting effects. Over time, and after the negative reaction to manipulation, the consumer will progressively forget the deceiving behaviour and the value of  will converge to 0 in the long-run (if no other attempt to manipulate is undertaken by the same firm).

will converge to 0 in the long-run (if no other attempt to manipulate is undertaken by the same firm).

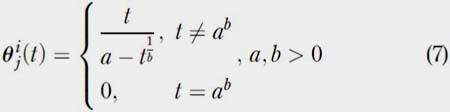

To reflect the above reasoning, consider the following function of sensitivity to manipulation:

According to equation (7), time period t = ab will correspond to the threshold when the consumer realizes that he/she is being fooled and changes drastically his/her behaviour from strongly accepting the communication of the firm to strongly rejecting it. Therefore, in the proposed framework, manipulation has a positive short-run effect for the firm, but after a few periods, the deceiving firm will start losing clients as the motivation to buy falls, given the consumers’ perception that they might be again deceived.

Return, once again, to the example. Assume that firm j = 5 (the "blue" firm) adopts a deceiving behaviour at date t, and that, for all consumers, the sensitivity to manipulation is given by equation (7), with a = 101 and b = 1/3. With these values, if the moment of the change in the firm’s behaviour is t = 1, then Θ5</(1) = 0.01; this value will rise until Θ5(4) = 0.1081 and, then, will suddenly fall to Θ5(5) = –0.2083. After t = 5, the value of the sensitivity term will progressively converge to 0.

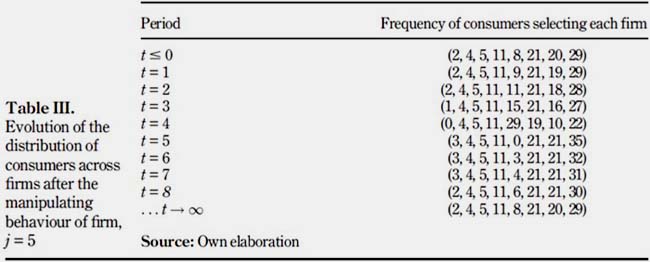

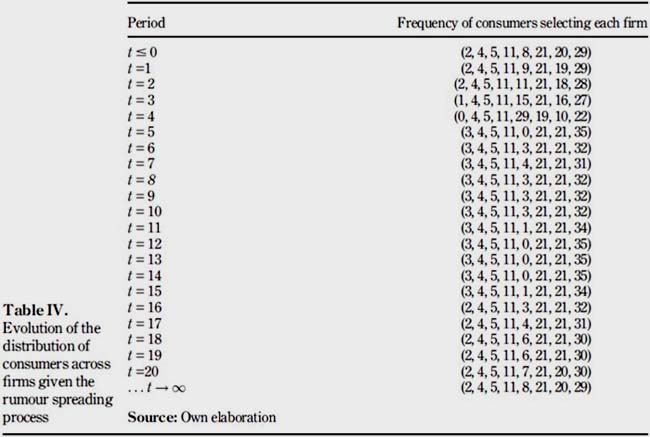

Let us apply this deceiving behaviour to the last example in Table II and consider that the respective distribution of consumers is the one effectively observed at t ≤ 0. Given the deceiving behaviour of firm j = 5 at t = 1, the distribution of firms will evolve as indicated in Table III.

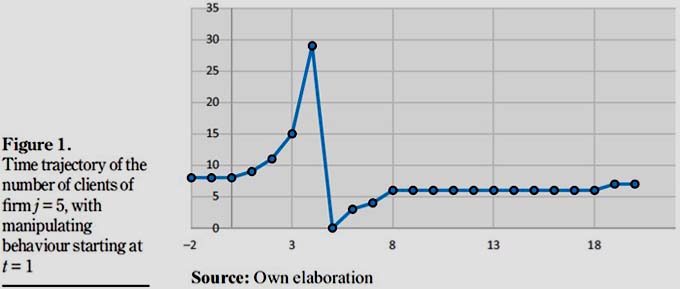

The changes of consumer choice presented in the table reveal that in this specific example, firms j = 2, j = 3 and j = 4 are not affected by the manipulating behaviour of firm j = 5; they maintain in all periods the same costumers. The remaining firms lose clients to firm j = 5 in a first phase and then, after t = 4, they recover those clients. Firm j = 5 gains a significant number of customers in the initial phase, and, once perceived the manipulating behaviour, all clients are lost, although they are progressively recovered in the next periods until the initial equilibrium is finally restored. Figure 1 shows the time trajectory of the number of costumers associated with firm j = 5.

Morality strikes back: consumers spread the word

Besides the direct impact analysed in the previous section, the deceiving behaviour of firm j might have reputational damages as well. Imagine that a single consumer considers that the deceiving behaviour of firm j is, in a first moment, worth being denunciated. The disapproval on the deceiving behaviour will then be eventually passed on to the other consumers, implying a transitory phase of pervasive resentment toward the firm with a less honourable behaviour. The action of consumers in this context is solely driven by the empathy toward others; this action contains no direct economic gain, and it is grounded in strict moral principles (not wanting others to suffer from the firm’s misbehaviour that the consumer that spreads the word had to endure).

To formalize the propagation of the news on the firm’s manipulating action, we consider a spreading mechanism like the rumour spreading dynamics studied in the scientific literature (Zanette, 2002; Nekovee et al., 2007; Huo et al., 2012; Wang et al., 2013). Let xi(t) be the share of consumers that, at date t, have no knowledge on the deviant behaviour of the firm. Share yi(t) represents the share of consumers who are knowledgeable on that behaviour and spread this information; finally, share zi(t) are those who know that the firm has misbehaved but are no longer engaged in spreading the news (these are frequently known as the stiflers). These three types of consumers compose the whole universe of agents in the demand side, xi(t) + yi(t) + zi(t) = 1. Individual consumers meet randomly with one another with a single other consumer per period and the following rules, common to the rumour propagation literature, apply:

-

When a spreader meets an ignorant, the second becomes a spreader as well with a probability ω є (0,1).

-

When a spreader meets another spreader or a stifler, both individuals become stiflers with a probability ζ є (0,1).

These rules may translate in the following set of difference equations:

Equation (8) might be reduced to a two-equation system with two unknowns:

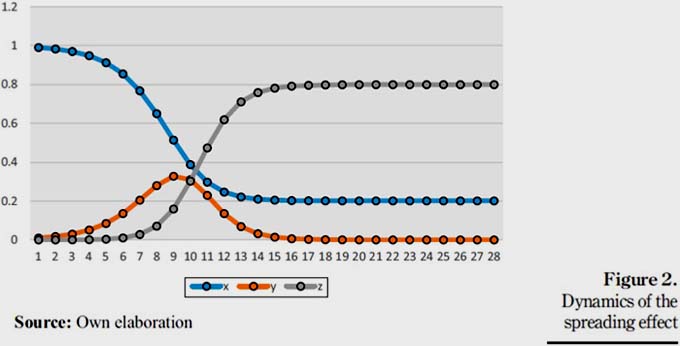

The pair of equation (9) characterizes a spreading mechanism such that a single consumer may adopt, in an initial phase, an indignation attitude toward the manipulating behaviour of the firm. This sentiment of disqualification of the firm will then be passed on, through a gradual spreading process, to a significant share of the other firms, which first become spreaders and then, in the long-run, all end up as stiflers. Figure 2 shows the spreading dynamics for ω = 0.75 and ζ = 0.9. In the long run, there is no spreader, but around 20 per cent remains unwilling to disseminate compromising information about the deceiving practices of the firm (this group includes individuals for which the respective moral conduct does not compel them to alert others about the observed misconduct).

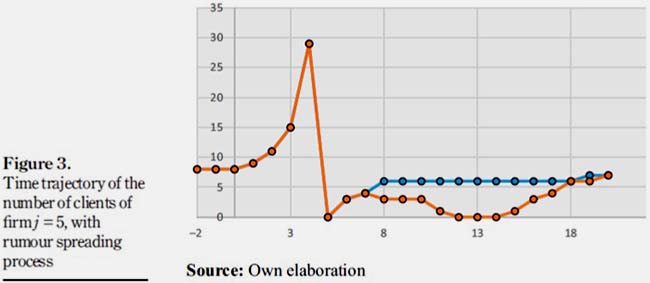

To simulate the evolution of the distribution of consumers in the presence of a deceiving behaviour from a firm, recover the scenario of the previous section where firm j = 5 engages in dissimulation in period t = 1. Consumers will react to the absence of fair play following rule [equation (7)], although an additional effect is now added; this is the effect of consumer communication as presented in equation (1). Let  (the effect of negative rumours over the motivation to buy is, obviously, negative) and let Sj(t) be the number of spreaders in each period following the perception that the firm is adopting an ethically questionable behaviour. This number of spreaders evolves over time following equation (9). Because the number of spreaders first increases and then declines, there is a period of 10 to 15 periods where the number of costumers of firm j = 5 persists very low, before the initial equilibrium is restored.

(the effect of negative rumours over the motivation to buy is, obviously, negative) and let Sj(t) be the number of spreaders in each period following the perception that the firm is adopting an ethically questionable behaviour. This number of spreaders evolves over time following equation (9). Because the number of spreaders first increases and then declines, there is a period of 10 to 15 periods where the number of costumers of firm j = 5 persists very low, before the initial equilibrium is restored.

Table IV. indicates what happens in this scenario, taking into account the same starting point as in the no spreading the word case.

Figure 3 represents the number of consumers associated with firm j = 5 under the rumour spreading mechanism. The lighter trajectory represents the outcome with the spreading word effect, in contrast with the initial pure manipulation effect (darker line). One observes that consumers’ communication makes it more sluggish the return to the original scenario: a moral social penalty is imposed to the one who deludes.

Conclusion

Markets are complex entities where agents endowed with distinct capabilities, preferences, moral codes and views of the world co-exist and co-evolve. To capture such heterogeneity in a straightforward, comprehensive and manageable analytical framework is a difficult and cumbersome task. In this paper, market relations were approached focussing the attention on deceiving behaviour, morality and the capacity markets have to self-regenerate after being disturbed by eventually opportunistic and deviant behaviour of some of the market participants.

After a brief literature review on deception and morality, the study offers a compact analytical framework capable of synthesizing the most relevant determinants of the consumers’ purchasing decisions. These necessarily include price and preferences, but deception and morality can also be integrated in the framework. Specifically, it is assumed that manipulation gives place to a fast increase in the preference by the variety of the good sold by the manipulating firm, which is followed by a sharp decline in the motivation to buy such good’s variety once buyers understand they are being fooled. In the long term, the pre-manipulation equilibrium is restored; the velocity with which this occurs is contingent on the communication between consumers, which can delay the restauration of the confidence in the deceiving agent.

References

Akerlof, G.A. (1970), "The market for ‘lemons’: quality uncertainty and the market mechanism", Quarterly Journal of Economics, Vol. 84 No. 3, pp. 488-500.

Akerlof, G.A. and Shiller, R.J. (2016), Phishing for Phools – The Economics of Manipulation and Deception, Princeton University Press, Princeton, NJ. [ Links ]

Banerjee, A., Yakovenko, V.M. and Di Matteo, T. (2006), "A study of the personal income distribution in Australia", Physica A, Vol. 370 No. 1, pp. 54-59. [ Links ]

Basu, K. (2016), "Markets and manipulation: time for a paradigm shift?", World Bank Policy research working paper N° 7653. [ Links ]

Bonroy, O. and Constantatos, C. (2015), "On the economics of labels: how their introduction affects the functioning of markets and the welfare of all participants", American Journal of Agricultural Economics, Vol. 97 No. 1, pp. 239-259. [ Links ]

Bowles, S., Kirman, A. and Sethi, R. (2017), "Retrospectives: Friedrich Hayek and the market algorithm", Journal of Economic Perspectives, Vol. 31 No. 3, pp. 215-230. [ Links ]

Dosis, A. (2016), "On signalling and screening in markets with asymmetric information", HAL working paper N° 01285190. [ Links ]

Gerschlager, C. (2007), "Adam Smith’s account of self-deceit and informal institutions", DULBEA working paper N° 7-10. RS.

Gruss, L. and and Piotti, G. (2010), "Blurring the lines: strategic deception and self-deception in markets", MPIfG discussion paper N° 10/13.

Huo, L., Huang, P. and Guo, C.X. (2012), "Analyzing the dynamics of a rumor transmission model with incubation", Discrete Dynamics in Nature and Society, p. 21. [ Links ]

Kaplan, S.N. and Rauh, J. (2013), "It’s the market: the broad-based rise in the return to top talent", Journal of Economic Perspectives, Vol. 27 No. 3, pp. 35-56.

Kaplow, L. and Shavell, S. (2007), "Moral rules, the moral sentiments, and behavior: toward a theory of an optimal moral system", Journal of Political Economy, Vol. 115 No. 3, pp. 494-514. [ Links ]

Lindstrom, M. (2008), Buyology: Truth and Lies about Why we Buy, Doubleday, New York, NY. [ Links ]

Manner, M. and Gowdy, J. (2010), "The evolution of social and moral behavior: evolutionary insights for public policy", Ecological Economics, Vol. 69 No. 4, pp. 753-761. [ Links ]

Nekovee, M., Moreno, Y., Bianconi, G. and Marsili, M. (2007), "Theory of rumor spreading in complex social networks", Physica A, Vol. 374 No. 1, pp. 457-470. [ Links ]

Paganelli, M.P. (2010), "The moralizing role of distance in Adam Smith: the theory of moral sentiments as possible praise of commerce", History of Political Economy, Vol. 42 No. 3, pp. 425-441. [ Links ]

Perri, T. (2016), "Lemons and loons", Review of Behavioral Economics, Vol. 3, pp. 173-188. [ Links ]

Ramiah, V. and Moosa, I.A. (2015), "Neoclassical finance, behavioral finance and noise traders: a review and assessment of the literature", International Review of Financial Analysis, Vol. 41, pp. 89-100. [ Links ]

Wang, Y.Q., Yang, X.Y., Han, Y.L. and Wang, X.A. (2013), "Rumor spreading model with trust mechanism in complex social networks", Communications in Theoretical Physics, Vol. 59 No. 4, pp. 510-516. [ Links ]

White, M. (2010), "Adam smith and Immanuel Kant: on markets, duties, and moral sentiments", Forum for Social Economics, Vol. 39 No. 1, pp. 53-60. [ Links ]

Witztum, A. (2010), "Interdependence, the invisible hand, and equilibrium in Adam Smith", History of Political Economy, Vol. 42 No. 1, pp. 155-192. [ Links ]

Zak, P.J. (2011), "Moral markets", Journal of Economic Behavior and Organization, Vol. 77 No. 2, pp. 212-233. [ Links ]

Zanette, D.H. (2002), "Dynamics of rumor propagation on small-world networks", Physical Review E, Vol. 65, p. 041908. [ Links ]

Zhang, T. and Zhang, D. (2007), "Agent-based simulation of consumer purchase decision-making and the decoy effect", Journal of Business Research, Vol. 60 No. 8, pp. 912-922. [ Links ]

Zhou, X., Gibler, K. and Zahirovic-Herbert, V. (2015), "Asymmetric buyer information influence on price in a homogeneous housing market", Urban Studies, Vol. 52 No. 5, pp. 891-905. [ Links ]

Notes

1. As an example, see Zhou et al. (2015) for an analysis of buyer heterogeneity in the housing market, where the heterogeneity is essentially attached to the geographical location of the potential buyers.

2. Banerjee et al. (2006) claim that the typical distribution of income might be fitted by an exponential, log-normal, or gamma distribution. Here, we directly associate the sensitivity to price to the income of the agent and adopt the exponential distribution to reflect this connection.

Citation:

Gomes, O. and Frade, J. (2019), ""Fool me once, …": deception, morality and self-regeneration in decentralized markets", Journal of Economics, Finance and Administrative Science, Vol. 24 No. 48, pp. 312-326. https://doi.org/10.1108/JEFAS-04-2018-0032

Received: 1 April 2018

Revised: 8 November 2018

Accepted: 21 November 2018