English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mail Cited by SciELO

Cited by SciELO  Similars in

SciELO

Similars in

SciELO

Permalink

Permalink1. Introduction

The countless investigations carried out to try to exhaust the question of the capital structure are endless, for example items such as forms of data collection, variables to be chosen for an econometric model, the econometric tools used, the types of companies and the legal characteristics of the accounting-financial area.

Titman and Wessels (1988) analyzed the explanatory power of some variables on capital structure. Kochhar (1997) believes that companies with strategic assets are able to achieve a sustained competitive advantage.

Perobelli and Fama (2003) share that “theories suggest that companies select their capital structure according to theoretical attributes that determine the various costs and benefits associated with the issuance of shares or debt,” and in an attempt to do work based onTitman and Wessels (1988), using factor analysis, the authors carried out this verification for the Latin American market, in particular for Chilean companies, analyzing which variables help to maintain the indebtedness of companies listed on stock exchanges in the countries that carried out their research.

The way in which the managers combine the sources of financing is an important decision for the financial and strategic context of the company. The capital structure refers to the way in which companies use sources of origin, whether their own or those of third parties, to apply in patrimony assets and in activities that demand them.

Furthermore, inquiries related to the choice of financing - indebtedness versus own capital - have gained importance for the investigation of management strategy. In a short space of time, there was a significant increase in the attention devoted by the management strategy literature to financial aspects (Sandberg et al., 1987; Kochhar, 1997).

Therefore, the justification for this study is to evaluate the capital structure of the companies listed on the Chilean stock exchange, in the period from 2007 to 2016. Contemporary capital structure theory emerged with the work of Modigliani and Miller (1958), in which they refer that, under certain conditions, the form of financing of companies is irrelevant. The determinants of capital structure are not restricted only to company-specific factors.

As observed in previous studies, it was possible to elaborate the following research problem-question: What is the behavior of the determinants of the capital structure of companies listed on Chilean stock exchanges, under the prism of the financial theories of the pecking order and trade-off, in the period from 2007 to 2016?

The general objective of this research is to compare the behavior of variables that determine the capital structure of Chilean companies listed on the stock exchange. In this way, institutional aspects (number of employees and open units) and economic aspects (market niche, performance in the internal and external markets) will not be evaluated, being limited only to specific factors of the company.

To better guide the research, the steps to be taken to be able to answer the main objective is to select the independent variables, statistically test them in relation to the types of indebtedness and analyze the behavior of these variables as determinants of the capital structure of Argentine and Chilean companies to light from trade-off theory (TOT) and pecking order theory (POT).

This study is organized as follows: Section 1 describes the context of the studies and the research objectives; Section 2 presents the literature review, as well as the discussions of the proposed hypotheses; Section 3 describes the sample and the methodology used; Section 4 shows the research results; Section 5 presents the research conclusion.

2. Literature review

From these studies on capital structure, a long discussion was established, that is, many works were carried out and other theories were elaborated in an attempt to explain what determines the use of own or third-party capital by companies, in addition to ideal mix between funding sources.

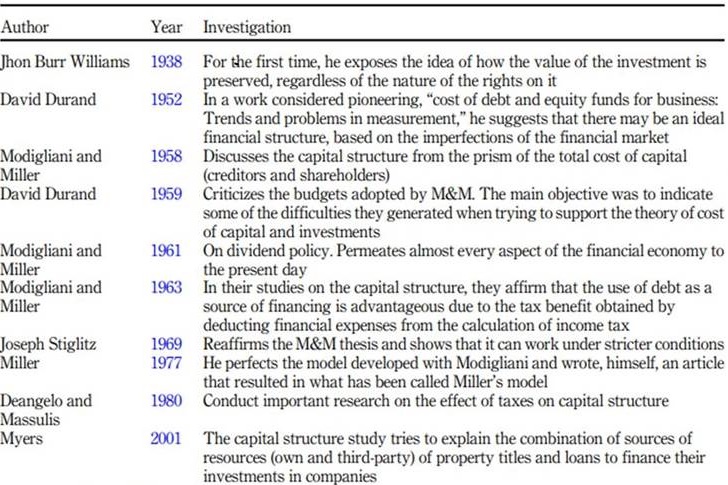

Table 1 presents the evolution of theories on capital structure in recent decades. In addition to works that are concerned with discussing differences and testing theories developed by Modigliani and Miller (1961and traditionalists, there is a class of authors who prioritized the discussion of bankruptcy costs and their influence on the definition of the structure. Capital of companies.

There is a predominance of two theoretical trends on capital structure: POT and TOT.

When trying to find a balance between indebtedness and maximizing the value of companies, going through financial difficulties and tax benefits, TOT by Modigliani and Miller (1958) Miller(1977), 1963) proposes, in perfect markets, that the capital structure can impact the value of the company, that is, although indebtedness is interesting for the company, managers know that it should not be increased indefinitely (Kraus and Litzenberger, 1973).

Fama and French (2002) confirm the predictions shared in the POT, that is, they are more profitable and companies with fewer investments have higher dividend payments. Research carried out by Bastos et al. (2009), Espinosa et al. (2012), Rodrigues et al. (2017), Fiirst et al. (2017) and Rodrigues and Santos (2018) analyzed the behavior of the capital structure of companies in Latin American countries (Brazil, Argentina, Chile, Mexico, Colombia and Peru), whose analysis periods for each study were from 1998 to 2013, rescuing the POT and TOT

2.1 Optimal capital structure: hypotheses

Research on the capital structure of companies is considered the most important in the area of finance. Various theoretical approaches have been discussed and tested in the financial literature. Perobelli and Fama (2003) found that the optimal capital structure, to be pursued by companies, was never achieved. In this case, new theories emerged that sought to explain the choice of capital structure by companies. Some relevant works in this line were developed by Remmers et al. (1974), Toy et al. (1974), Scott and Martin (1975), Stonehillet al. (1975), Ferri and Jones (1979), DeAngelo and Masulis (1980), Bradley et al. (1984), Myers and Majluf (1984), Myers (2001), Lumby (1991), Thies and Klock (1992), Balakrishnan and Fox (1993), Allen and Gregory (1995) and Rajan and Zingales (1995) Stiglitz(1969) (Perobelli and Fama 2003, p. 12). Durand(1952) Durand(1959)

Tapia and Albornoz (2017) present a regulatory model that allows the administration to establish in advance the optimal capital structure and concentrate efforts toward that objective. The effect of personal taxes on shareholders and debt owners, on tax economies and, therefore, on the optimal capital structure was studied.

Booth et al. (2001) and Bastos et al. (2009) state that it is not a very easy task in determining hypotheses between theoretical currents, as the behavior of a certain variable can be explained by one or another theory

When evaluating deals, an important issue to consider is the level of detail. If for analysts to add details is to provide an opportunity for better forecasts for each added item, then, on the other hand, it would be interesting to create more inputs, which in this case could increase the potential for errors to occur in each added input (Damodaran, 2007),).

According to Myers and Majluf (1984), Myers (1984)and Nakamura et al. (2007), the POT indicates the use of sources of resources and acting on new opportunities for the organization’s growth, in which the company’s administrators are guided by a hierarchy of resources to bet on these growth opportunities. Therefore, it is expected that more profitable companies will have to borrow less. Corroborating this idea, Ross (1977 apud Harris and Raviv, 1991) states that there is a positive relationship between the level of indebtedness and profitability. In contrast, Brito et al. (2007) state that profitability is not a determining factor in a company’s capital structure.

From this scenario, the following hypotheses are proposed:

H1. There is a significant negative relationship between return to shareholders and debt indicators.

H2. There is a significant negative relationship between asset returns and debt indicators.

For Myers and Majluf (1984), companies invest in their assets to guarantee their debts when evaluating opportunities at the time of their business, including in future situations. With this, companies disrupt risk strategies used by shareholders who intend to extract wealth from their creditors. Inverse views are taken by Brito et al. (2007), and there is a negative relationship between a company’s assets and its total indebtedness. Therefore, the following hypothesis is proposed:

H3. There is a significant positive relationship between asset growth and debt indicators.

It was noticed in previous research that companies that have growth potential have greater flexibility to invest, and they tend to increase their debts, which indicates a negative relationship with the organization’s growth (Kayo and Fama, 1997; Gaud et al., 2005). Gomes and Leal (2001), on the other hand, found a positive relationship between the level of growth and the company’s indebtedness. Brito et al. (2007) found the same relationship with longterm debt and no relationship with short-term debt. These latest studies found that companies that need more resources to invest in opportunities tend to get more into debt. Therefore, the following hypothesis is proposed:

H4. There is a significant negative relationship between sales growth and debt indicators.

For Titman and Wessels (1988), they state that fixed assets help companies to increase their debt because of payment guarantees to obtain and keep these types of investments as their assets. The idea is to mitigate the agency theory between stakeholders and shareholders Myers and Majluf (1984). Therefore, the following hypothesis is proposed:

H5. There is a significant positive relationship between asset tangibility and debt indicators.

Bastos et al. (2009) and Correa et al. (2013) found a strong influence of the current liquidity variable, whose result was a negative relationship between liquidity and debt, confirming the hypothesis of the hierarchy theory. Therefore, the following hypothesis is proposed: H6. There is a significant negative relationship between current liquidity and debt indicators.

Correa et al. (2013) and Bastos et al. (2009) found a negative relationship between the level of income tax payment and the total indebtedness of companies. The same result of this relationship is found when the indebtedness is with market value and onerous short- and long-term indebtedness. Therefore, the following hypothesis is proposed:

H7. There is a significant negative relationship between the level of income tax and debt indicators.

2.2 From Latin America to the Chilean context

Studies such as Bastos et al. (2009), Espinosa et al. (2012), Rodrigues et al. (2017), Fiirst et al. (2017) and Rodrigues and Santos (2018) analyzed Latin American countries, in particular the behavior of the capital structure of Chilean companies.

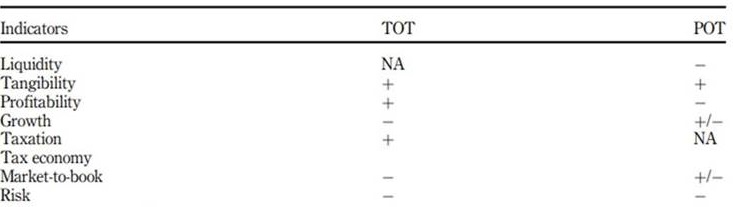

Table 2 illustrates the behaviors of variables independent of debt indicators, according to international literature:

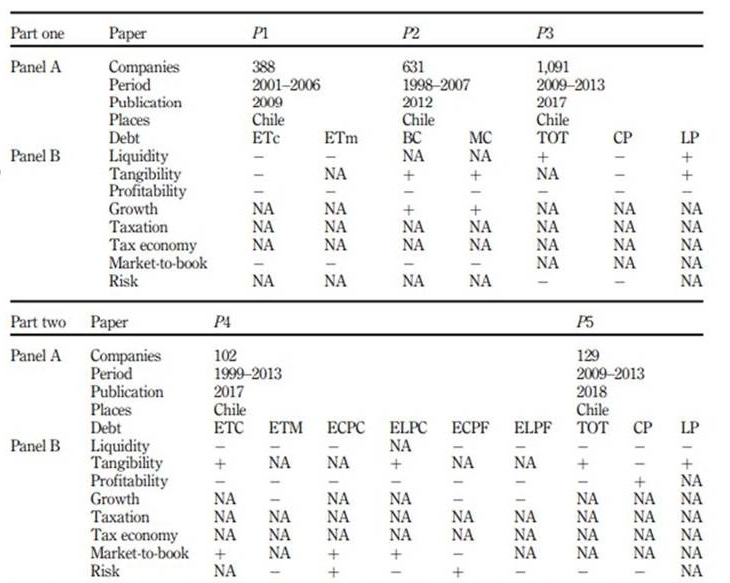

Based on studies in Latin America, the behavior of independent variables concerning debt indicators are as indicated in Table 3.

First-hand, it is clear that there were no studies on the taxation and fiscal economy variables when the studies address Chilean companies.

When evaluating the liquidity of Chilean companies, it is found that most studies found results similar to the POT.

When it comes to tangibility, it was found in the studies proposed for evaluation that most converge to POT and TOT.

When analyzing profitability, it is clear that most of the results found in studies that contain Chilean companies are in line with POT.

Assessing the growth variable, we see that the results of Chilean companies tend more toward TOT than toward POT.

In most studies that treat Chilean companies as data, market-to-book (MTB) tends more toward TOT’s results, although POT, for this variable, receives positive and negative results.

Finally, most studies with Chilean companies have results in tune with TOT and POT, negatively relating to indebtedness.

3. Method

The present empirical research studied, as methodological features, the following steps: the period of analysis and accounting-financial data; method, methodological approach, nature and research strategies; and analysis tools, diversification and variables.

Table 3 Signs of independent variables with studies of Chilean companie

Note(s): (1) P1 - Paper 1 - Bastos et al. (2009); P2 - Espinosa et al. (2012); P3 - Rodrigues et al. (2017); P4 - Fiirst et al. (2017); P5 - Rodrigues and Santos (2018) (2) ETc, total accounting indebtedness; ETm, total market indebtedness; ECPC, short-term accounting indebtedness; ELPC, long-term accounting indebtedness; ECPF, short-term financial indebtedness; ELPF, long-term financial indebtedness; TOT, total indebtedness; CP, short-term indebtedness; LP, long-term indebtedness; BC, book capital; MC, market capital; NA, not applicable

Source(s): Prepared by the authors

3.1 Data

This research proposal was carried out between 2007 and 2016 with balance sheets and results of the years related to companies listed on the Chilean stock exchange, whose period was chosen to analyze the capital structure that reflects the subprime crisis in the United States that occurred in 2007 and ended with the Brazilian political crisis in 2016.

3.2 Variables and procedures

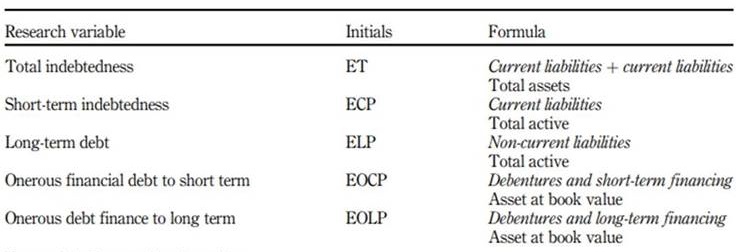

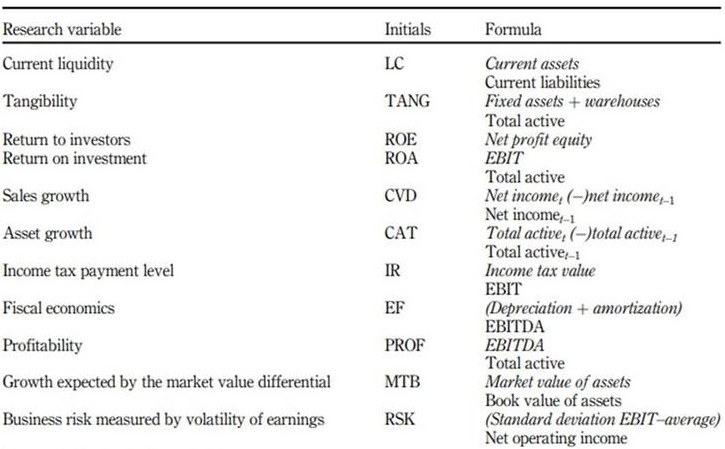

All dependent and independent variables used in the econometric tests were defined from the theoretical framework. Data are primary and quarterly and include the economic-financial variables of publicly held companies. The variables that make up this study are presented in Tables 4 and 5, which expose their names, acronyms and calculation formulas. The dependent variables shown in Table 4 represent the indebtedness indicators and were used in the panel data regression models in the execution of this study. They were based on readings from previous research.

The determinant variables of the capital structure were based on previous investigations and will be able to point out whether there is any relationship and significance for the econometric panel data model.

3.3 Econometric models

The application of the econometric models was made from this general equation:

Each study variable is represented by the respective acronyms:

E i : represents the dependent variables that deal with the indebtedness of the companies

LC it : represents the independent variable of current liquidity.

TANG it : represents the independent variable of tangibility.

ROE it : represents the independent variable of return to shareholders.

ROA it : represents the independent variable of return on investment.

CVD it : represents the independent variable of sales growth.

CAT it : represents the independent variable of asset growth.

IR it : represents the independent variable of income tax payment level.

EF it : represents the independent variable of fiscal economy.

MTB it : represents the independent variable of market-to-book.

RSK it : represents the independent risk variable of the business.

it : represents that the variables are used for all the proposed models of linear multiple regression of panel data: POLS, fixed effects and random effects.

t : represents time.

Finally, the next section presents the results of the research and analysis based on information about the correlation matrix of the variables, the signs of the variables and the validation of the assumptions of the data regression models in the panel (Breusch-Pagan, Chow and Hausman tests).

4. Results

To begin, the first step, described in Section 4.1, sought to examine the relationship between historical market values and the capital structure of companies listed on the stock exchanges and Chile, with the aim of identifying the possible behavior of the average level of indebtedness and the standard deviation of the variables studied between 2007 and 2016.

The second step, described in Section 4.2, sought to test the intensity and direction of the relationships between the variables using the Pearson correlation coefficient, together with the inflation factor of variance, to identify possible multicollinearity problems.

Finally, Section 4.3 presents the results obtained and summarizes the main results found in this research.

4.1 Descriptive analysis

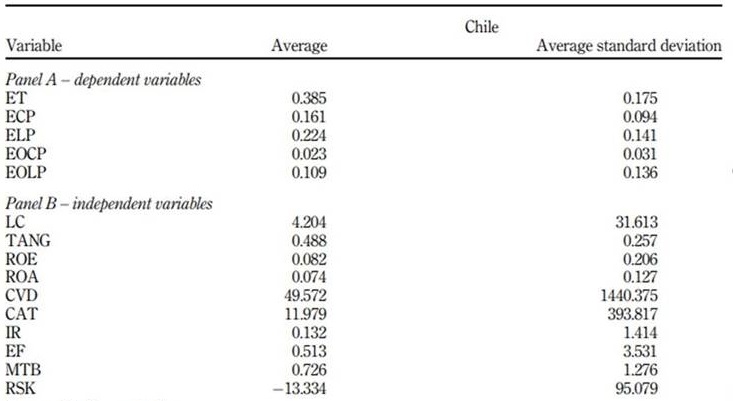

Table 6 presents the average level of indebtedness and the standard deviation of the variables studied, between 2007 and 2016, of Chilean companies evaluated. The data in panel A reveal, on average, in the period from 2007 to 2016, in Chile, the following results, in relation to the characteristics of the indebtedness (dependent variables): Chile presents average in total indebtedness, setting at 38.5%; Chile has the average shortterm debt, around 16%; for long-term indebtedness, short-term and long-term burdensome, Chile marked the presence with the lowest average only in short-term debt onerous, with 2.3%.

Regarding the behavior of independent variables, in which they represent the determining variables of the capital structure, the results reported in panel B of Table 6 were as follows:

(1) Chilean companies present four determining variables of the capital structure with the highest averages (current liquidity, ROE, growth in sales and assets)

(2) Chile’s current liquidity, which translates as the ability that companies have to settle their debts in the short term using assets also in the short term, totals to, on average, 4.2, that is, for each monetary unit of the debt short-term (obligations), companies, on average, have four units to withdraw these debts (financially, assets and rights activated);

(3) Regarding the indicators of return to partners and entrepreneurship, Chilean companies had an average with ROE of 8.2%;

(4) Chilean companies had the average of 23% in sales growth and assets growth; in relation to taxes, Chilean companies with the variable fiscal economy have the average 51%.

4.2 Correlations and panel data

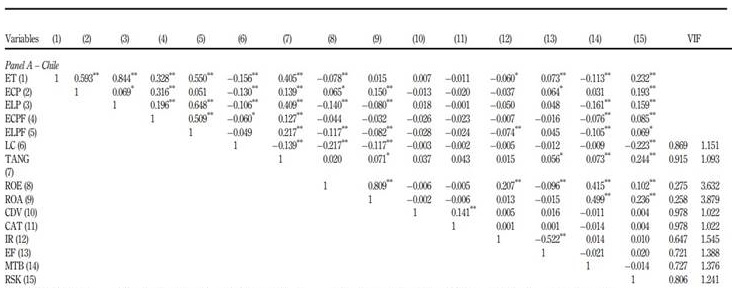

Before the presentation and evaluation of the data in the panel, it is necessary to clarify the advantages of this method. The data, as seen in Table 8, are in a cross-section, and, in the econometric literature, they are known as panel data or longitudinal data. As an advantage, according to the simple Pearson correlation calculation, they allow evaluating the data between them, in addition to the influence of their relationships on the final result of the analysis, since it allows the evaluation of the explanatory variables on the dependent variable throughout of the period studied (Wooldridge, 2010).

Therefore, Table 7 presents the relationship between the 15 variables and their correlations for each country analyzed in the research (Chile). Wooldridge (2010) also comments on the advantage of using this method to observe possible omitted variables. It is observed that the degree of freedom changes from one variable to another since some variables have a degree of freedom of 0.05, or 95% assertiveness. This variation is a consequence of the analyzed data, and this factor is indicated as advantageous by Brooks (2008), which indicates that the data are not fixed, that is, they can vary over time and according to other factors.

Table 7 Pearson correlation and variance inflation factor test

Note(s): Ps.: (*) the correlation is significant at the 0.05 level; (**) the correlation is significant at the 0.01 level; VIF: variance inflation factor

Source(s): : Prepared by the author (research data)

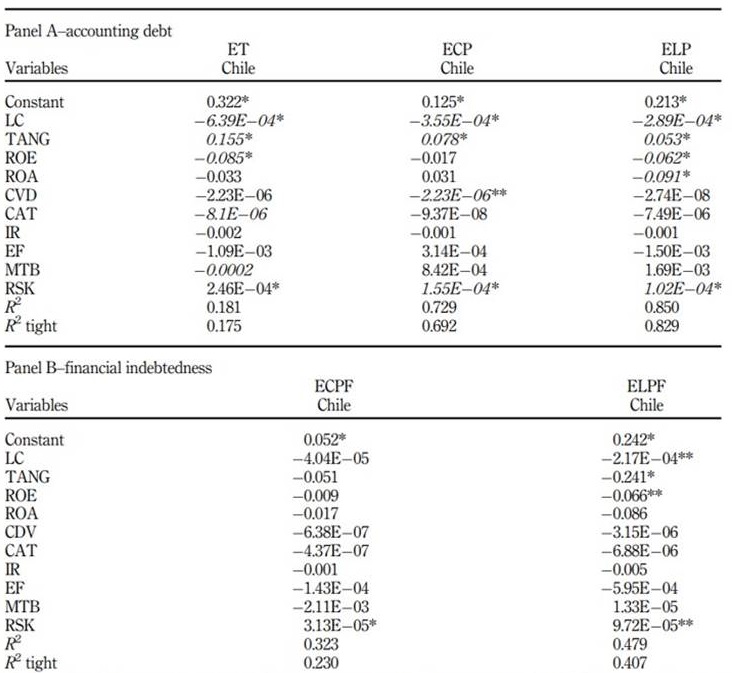

Table 8 Results of panel data regression

Note(s): Ps.: (*) the correlation is significant at the 0.01 level; (**) the correlation is significant at the 0.05 level

Source(s): Prepared by the author (research data)

The panel data presented in Table 8 provides a relationship between several data on different lines; the first line is of the constants. These constants are different for each country evaluated, and for each factor in each country, for example, the gap begins with accounting indebtedness, where the ET constant is 0.322 for Chile, all with the same degree of freedom of 0.01. In other words, for each ET factor, the percentage of Chile is only 32.2%.

The Breusch-Pagan, Chow and Hausman tests were performed on the variables of total indebtedness, short-term indebtedness and long-term indebtedness. Only the Hausman test in Chile had fixed effects.

Next, the Breusch-Pagan, Chow and Hausman tests were performed on the dependent variables of onerous short-term and long-term financial indebtedness. All countries maintained the same effects on the respective variables.

At the base of the panel are the values of R2 , which is the square of Pearson correlation, and adjusted R2 , called R2a , which present the adjustment of the correlation for the number of samples used in the Johnson and Wichern (1998) analysis. The explanatory power of the model with total debt for Chilean companies is 17.5%, considered low

Thus, the panel data offer a wide possibility of analysis of various factors in the econometric analysis, which converges with the advantages previously presented. Based on the findings in Table 7, the Pearson correlation between the variables assumes the existence of a relationship between the determining factors of the capital structure and the levels of accounting and financial indebtedness.

Table 8 shows the determinants that most influence the debt levels of companies. They are current liquidity (LC), tangibility (TANG), return to shareholders (ROE), return on assets (ROA), growth in sales (CDV), growth in assets (CAT), market-to-book (MTB) and business risk measured by the volatility of profits (RSK). This is close to the results obtained in other investigations in the area, such as Delcoure (2007), Nakamura et al. (2007), Bastos et al. (2009), Nunkoo and Boateng (2010), Williams(1938 Correa et al. (2013) and Povoa and Nakamura (2015). The analysis of the results is presented in the next section.

Being thorough, the following is evaluated:

(1) As for the results of the variables of Chilean companies, it can be seen that they tend toward the POT, as they present negative results of current liquidity concerning indebtedness.

(2) When dealing with tangibility, it is evaluated that when it comes to total indebtedness, short and long term tend to TOT and POT; when it comes to shortterm and long-term onerous debt, the results are reversed.

(3) It is noticed that the profitability results tend more towards the POT, with a negative relationship to indebtedness.

(4) In the case of growth indicators, it is found that Chilean companies tend more to TOT (with a negative relationship with indebtedness) than to POT, although POT, in this regard, is nebulous.

(5) The results of the relationship between taxation and indebtedness are negative with Chilean companies, totally inverse to the results proposed by the theoretical framework studies.

(6) Tax economy is an indicator not evaluated in Chilean companies. In this study, it presented negative values about indebtedness.

(7) When Chilean companies relate MTB with indebtedness, we find results similar to the two theories (POT and TOT), tending more toward TOT.

(8) When it comes to business risk, it is clear that Chilean companies have results that are averse to the theories (TOT and POT), with positive relationships with indebtedness.

5. Discussion and conclusions

The subject of capital structure has been extensively researched over more than sixty years and seems far from exhausted.

To define a time base, over the past ten years, research related to the capital structure is expanding the prospects for new areas of research and delving into issues that seemed to be on the verge of exhaustion. Two important works in this regard are Lemmon et al. (2008) and Frank and Goyal (2003), which review the aspects related to the determinants of capital structure. In fact, it is perceived that there is a consensus regarding the determinants of capital structure, together with the question that the two main theories of capital structure (TOT and POT) are not antagonistic, as the initial, but complementary, works suppose, and this new vision has been defended by various authors in recent years.

This research sought to analyze some determinants of the level of indebtedness of open capital companies in the Chilean stock exchanges, considering the two main theories on the subject. The analyses were performed based on data obtained from the financial statements of the open capital companies in the stock exchanges of these countries, in the period from 2007 to 2016. Static and dynamic tests were performed using the panel data model.

Already, the variable ROE and ROA point to a negative relationship for the levels of accounting and financial indebtedness. However, only Chilean companies showed a positive relationship between ROA and short-term debt. These results strongly confirm with hypothesis H1 that the relationship between return to shareholders and debt indicators is negative, and with H2 that the relationship between ROA and debt indicators is negative. Similar results are verified in Delcoure (2007), Nakamura et al. (2007), Bastos et al. (2009) and Correa et al. (2013), in addition to confirming the POT.

According to the POT, “(...) companies with higher growth rates, which demand more resources than they can generate, would tend to look outside the company for those resources necessary for expansion” (Correa et al., 2013, p. 110), that is, a positive relationship between growth and debt levels. However, growth opportunities can be seen as intangible assets, thus, “(...) the use of debt would be limited for these companies, which suggests that growing companies should be less indebted” (Correa et al. 2013, p. 110), that is, a negative relationship corroborating with the TOT. Thus, hypothesis H3, that the relationship between asset growth and debt indicators is negative, was found for total and short-term debt for Chilean companies. The H4, that the relationship between sales growth and debt indicators is negative, was found for short-term debt in Chilean companies. The results were also found in the study by Bastos et al. (2009).

The results for the MTB variable with debt levels were not significant for Chilean companies. The negative relationship was found in the studies by Nakamura et al. (2007) and Nunkoo and Boateng (2010).

Regarding tangibility (TANG), a positive and significant relationship occurred with the levels of accounting and financial indebtedness for Chilean companies, confirming hypothesis H5 for Chilean companies.

The current liquidity index (LC) presented a negative relationship with debt levels for Chilean companies, supporting the hypothesis regarding the POT. The results found induce the acceptance of hypothesis H6 of the investigation that the relation between current liquidity and the debt indicators is negative. This result goes against the findings of Nakamura et al. (2007), Bastos et al. (2009) and Povoa and Nakamura (2015). Thus, managers of companies with greater liquidity prefer to transform company assets into internal financing, as it is less expensive (Myers and Rajan, 1998), due to the greater financial slack in the retention of internally generated funds (Ozkan, 2001).

The level of income tax (IR) collection was in line with hypothesis H7, showing that Chilean companies have a negative relationship with the types of indebtedness studied in this research, bringing something new, given that studies presented in Table 3, with countries Latin Americans, did not present this variable. Finally, future research could address the influence of the cost of capital on the composition of the debt matrix of the companies listed on the Chilean stock exchanges.