Inglés (pdf)

Inglés (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Enviar articulo por email

Enviar articulo por email Citado por SciELO

Citado por SciELO  Similares en

SciELO

Similares en

SciELO

Permalink

PermalinkIntroduction

The influence of oil price in oil endowed economies, also called “petro-states”, has been analyzed from different perspectives (Priest, 2012; Alekperov, 2015; Bouoiyour et al., 2017; Sánchez, 2016). The effects of price volatility depend on the social, economic and geopolitical conditions of the country or region. In the case of Mexico, the economy is marked by the “paradox of abundance” or the “resource curse” (Sánchez, 2016); oil revenues contribute between 25 and 30% of public revenues (CEFP, 2019), making it, highly dependent on them (Anderson and Park, 2016; Huizar, 2015; Sierra and Méndez, 2017). Mexico is among the top 20 crude oil-and-condensate-producing and -exporting countries (EIA, 2020). Compared to other oil companies, Pemex is cost-competitive and profitable (Pemex, 2020a). However, the link between oil and public finances is an opportunity cost at a corporate level. The bonanzas from price increases go mostly to finance the federal budget through TDC, which, during 1977-2019, represented, on average, 98.5% of Pemex's profits (Pemex, 2019a, b; SIE, 2019).

At a corporate level, the best way to look at the price effect is through the BS (Cornejo et al., 2012; Morales et al., 2013). On a financial level, the situation of Pemex is defined by two variables, which play a determining role in the cash flow achieved annually: the oil price and the payment of TDC. The payment of TDC is an expense recorded in the BS and an accounting overview of inflows and outflows that reflects the balance of losses or profits of the firm at the end of the year (Pemex, 2019a). Conversely, the price is an external element to Pemex which is regulated by the international market, and in Mexico, that is taken as a reference to prepare the federal budget due to its influence on the public income and the investment decisions (Rodríguez and López, 2019; Reed et al., 2019).

In BS, the annual balance is determined by making a sequential subtraction of Pemex's total income, which, in turn, is determined by the oil price. The objective of this study is to understand how oil price expansions are reflected in Pemex BS and how they affect its corporate income and investment. For this purpose, six variables are used as follows: (1) total income; (2) sales revenue; (3) operating cost; (4) investment; (5) payment of TDC (6) payment of interest on debt. Total income includes sales of goods and services (internal and external); operating cost, salaries, rents and purchase of supplies; investment, i.e. the use of capital in various activities that yield benefits; TDC, i.e. the payment of tax obligations to the state and interest, i.e. the cost of indebtedness (Pemex, 2019a). This information is incorporated into a VAR model, which has been used in different research on oil prices (Cologni and Manera, 2008; Muhammad et al., 2018; Mirmirani and Cheng Li, 2004; Ismail et al., 2021; Kamaljit and Vashishtha, 2020).

Oil in Mexico is managed by a company that has its own accounting records where it reflects revenues and expenses that are equally affected by price. However, Pemex embodies two contradictory objectives within the national economy. On the one hand, it serves as a financial ark for the public treasury, which obtains a third of its financing from oil revenues; on the other hand, it needs resources to strengthen itself corporately (Pemex,2019b). Over time, Pemex management adjusts to the two scenarios which cannot be linearly related, as it would be proposed by a deterministic regression model that omits mutual adjustment dynamics of variables. Consequently, this research uses a VAR model because it assumes endogenous dependence of variables, i.e. the price and BS variables are mutually determined and are not the result of rational processes (Sims, 1982; Rodríguez, 2011). It should be noted that the results support this endogenous dependence between variables; however, there is a strong bias in favor of using Pemex financial management as an instrument of tax collection over the productive strengthening of the company. The contribution of the paper, in this sense, is an analysis of a corporate and accounting vision of Pemex. The results give solid support to the recommendation of reducing the tax burden and an impulse to new research with a micro-economic or financial focus, focusing on an in-depth proposal of a real plan for recovery and strengthening of Pemex, as opposed to the alternative of leaving it in the role of a supplier of public funds, exclusively (Sánchez, 2016; Hernández and Bonilla, 2020). Our first hypothesis is that Pemex responds to the state tax collection objectives and, at the same time, has investment needs; these two elements compete at a financial level, affecting the use of available resources. The second is that the oil price has a positive impact on Pemex's total income, but all the potential effect on investment is absorbed by TDC.

The rest of this paper is structured as follows. Section 2 reviews the most relevant literature on oil prices and literature focused on Mexico. Section 3 presents descriptive statistics on oil price, oil revenues and oil production, as well as a financial description of the variables and BS balance. Section 4 describes the method. In Section 5, the paper exhibits the results while Section6 discusses them, including practical implications of the research. Finally, Section 7 presents the conclusion.

Literature review

Regarding oil price, the same variation is perceived differently by households, politicians, financial markets and economists (Baumeister and Kilian, 2016), depending on the conditions of each country, its position (oil exporter or importer), macro-economic policy and its level of development (Derbali et al., 2019). This has been corroborated by Muhammad et al. (2018), for BRICS economies with a time-varying structural vector auto-regressive (TV-SVAR) model, which simulates the transmission dynamics of the effects stemming from random shocks and by Cologni and Manera (2008) for G-7 countries with a structural-cointegrated VAR model. In general, global energy demand reshapes oil trade (Priest, 2012), influencing the productive dynamics of countries (Shen et al., 2018; Abboud and Betz, 2021) and the best incentive for oil investment, in the face of price uncertainty, is non-distortionary taxes (Blake and Roberts, 2006).

Unlike companies that demand oil-derived inputs and experience a rise in costs, price expansions benefit those that produce oil, since they generate a higher-cash flow than expected. In this sense, the studies of Iqbal and Shetty (2018) are important, which address the impact of oil prices on capital expenditure of a group of oil companies, applying a VAR model, impulse-response function (IRF) and augmented-Dickey-Fuller test; they find that price effect depends on the sector in which they are located (exploration and extraction and refining) and size. ElFayoumi (2018) performs a similar analysis for USA companies in the manufacturing, commercial and mining sector, using a financial approach and a VAR model. His results show that price variations do affect company profits And that of Waheed et al. (2018), who estimate the effect of price on the stocks of companies in different sectors in Pakistan, finding that an increase gives positive signals to stock markets, boosting their performance. VAR models were born as a solution to classical econometric modeling based on the work of Sims (1982). Sims strongly criticized the classical macro-econometric models, since they do not consider many restrictions of economic theory that would cast doubt on the veracity of the results obtained (Rodríguez, 2011, pp. 86-87).

In the case of Mexico, oil is usually examined from a sectoral perspective and particularly from its contribution to public revenues (Bazán and González, 2011; Beshears, 2013; Fuentes and Cárdenas, 2010; Martínez, 2004; Sánchez, 2016; Silva et al., 2021; Huizar, 2015). Pemex is crucial for the Mexican state. Well-documented economic and market-based reasons (Álvarez, 2014; López and Nava, 2018; Salazar and Venegas, 2018), among other reasons, highlight the strategic value of oil and the possibility that Mexico can play its oil card to enhance its development. Pemex is a firm that, despite the policy of fiscal asphyxiation which has characterized it, has survived and generates profit. If the fiscal burden, the cost of its debt and other liabilities had been administered in the past within a framework balancing the national and business priorities, they could have been covered adequately or with minimal damage to the corporate finances, taking advantage of the periods of high prices that also led to higher income (Rodríguez and López, 2019; Sánchez, 2016). Any strategy to revitalize and stimulate oil activity requires considerable resources and high prices as incentives for investment (Bazán and González, 2011). The current government has undertaken a rescue plan for Pemex, which is a task of maximum complexity due to financial fragility caused by tax burden, excessive indebtedness (which exceeds US$100bn) (Fitch Ratings, 2020) and a drop in production (Hernández and Bonilla, 2020). Most notably, Pemex is once again playing an important role in national politics and is expected to progressively improve its presentation card in the global environment (Pemex, 2019b; Álvarez, 2014; Durán-Encalada and Paucar-Cáceres, 2012; Cabrera and Díaz, 2021).

The originality of the research consists of examining the impact of oil prices at the company level using Pemex BS variables, which is something that in the case of Mexico has not been proposed in the literature. The benefit from price increases is diluted by subtracting TDC payment, which is the highest compared to the rest of the BS expenditures. The VAR model captures this situation, giving quantitative support to the analysis and demonstrating empirically that Pemex management, in the face of oil price variations, privileges payment of TDC over investment.

Pemex financial statement, 1977-2019

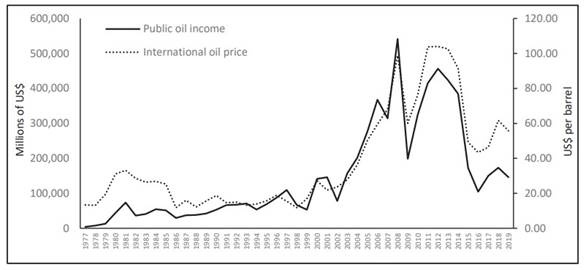

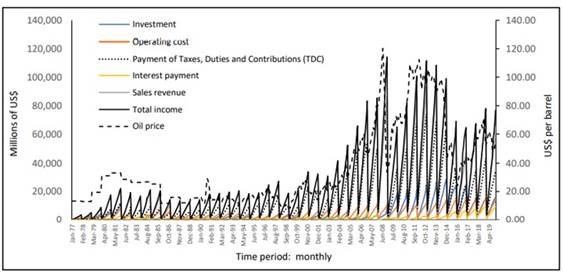

This section presents descriptive information on the trajectory of oil prices, public oil revenues and oil production during 1977-2019. Likewise, BS variables are used in the VAR model; their description and position in each of the formulas and the financial margin when subtracting each outlay. In general, the analyzed series shows a strong trend component. As shown in Figure 1, the oil price determines the magnitude of Mexico's oil revenues, which is a country that is trapped in the “paradox of abundance” (Huizar, 2015; Sánchez, 2016; Sierra and Méndez, 2017). Oil contributes one-third of public revenues and is a volatile variable (SIE, 2019).

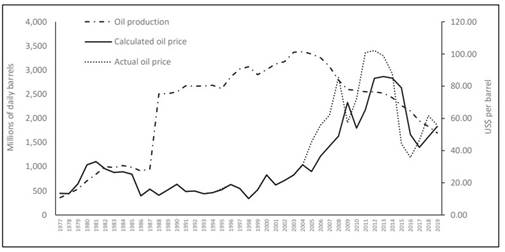

Although production had the possibility of being strengthened by price increases, it fell progressively for 15 years (2004-2019) (Figure 2). Funds were not allocated for the development of new oil fields or for the improvement of crude oil processing in refineries (Pemex,2019b; Silva et al., 2021). Pemex's investment was not favored by price dynamics and private capital inflow after the 2013 reform, which promised to be the solution to the needs of capital, was not as expected (Menchar, 2015). The outcome was that production went from 3,371 million barrels a day (mbd) in 2003 - the highest amount - to 1,701 mbd in 2019.

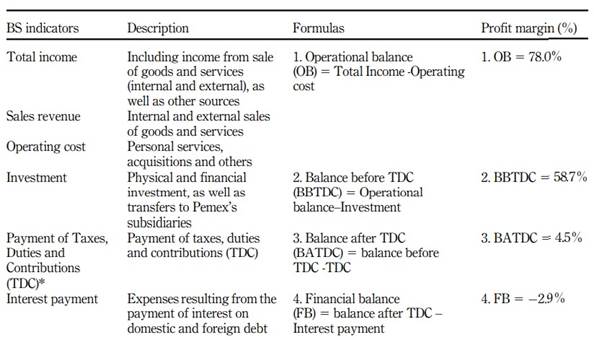

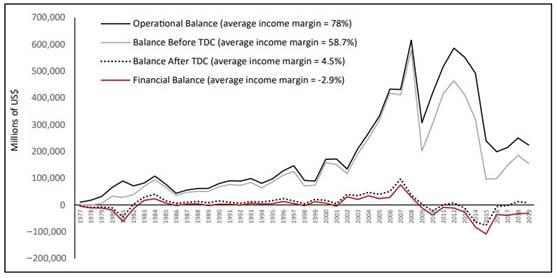

In terms of income, production capacity and brand equity, Pemex is the most important company of Mexico and one of the largest in Latin America, a region where it ranks number one in phosphate production. It is one of five companies with the largest logistics infrastructure in the world (Pemex, 2020a, (b). Considering profit and loss statements, Pemex's earnings before interest, taxes, depreciation and amortization (EBITDA) leaves it at a margin of 33% over net earnings, exceeding the ones generated by similar companies in other industries and by larger oil production companies. On the other hand, if it is appraised using the corporate indicators of the financial balance, as shown in Table 1, the average profit margin from 1977 to 2019 before payment of TDC (BBTDC) is 58.7% (formula 2) and drops to 4.5% after deducting the amount of the payment of TDC (formula 3). After deducting interests, it drops further to −2.9% (formula 4).

Table 1 Indicators from Pemex’s financial balance and average profit margin, 1977-2019

Note(s): *Indicator linked to the company’s tax burden Source(s): Own calculations based on data from Pemex’s Financial Balance for 1977-2019 (Pemex, 2019a)

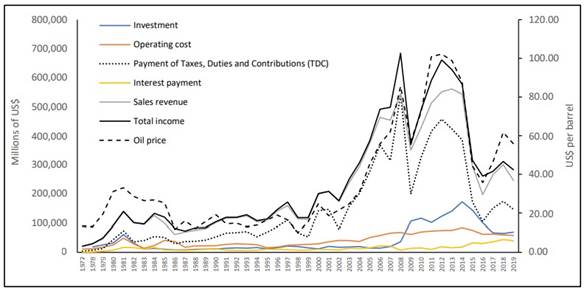

The profit margin, before and after TDC, shows that the tax burden represents a structural problem as it restricts the generation of enough cash flow not only to meet investment requirements, but also to obtain acceptable profits after taxes. If the oil price is taken into consideration along with the indicators above, the payment of TDC, for the time being, and only descriptively, has the closest relation to the oil price, which, in financial terms, poses a high-opportunity cost to the other indicators (Figure 3). Pemex creates value and has of the oil industry highest EBITDA margins and BBTDC when analyzed using the method herein (Figure 4). Tax burden remains the main problem for the company, regardless of whether it continues focusing on extraction or seeks to reactivate the whole production chain (Pemex, 2019a, (2020a).

Source(s): Own calculations based on Pemex(2019a) and SIE (2019)

Method

Sample and variables

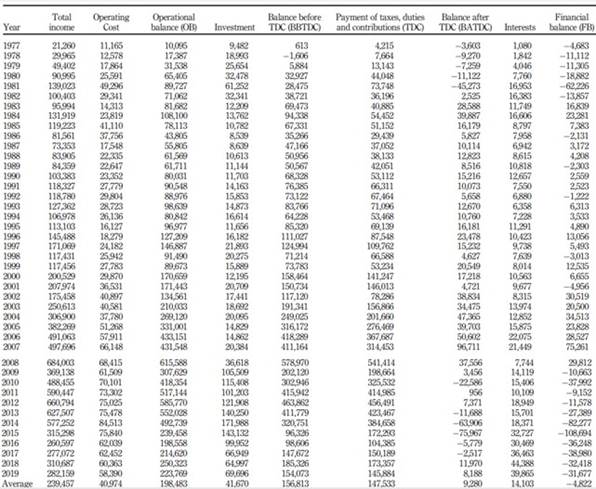

Data obtained monthly from variables for the period between 1977 and 2019 amount to 516 observations. They correspond to the oil price and the BS indicators, which are described in Table 1. Data were obtained from the Subdirección de Programación y Presupuestación de la Dirección Corporativa de Finanzas de Pemex (Subdivision of Planning and Budgeting of Pemex's Corporate Direction of Finance) and the Sistema de Información Económica del Banco de México (SIE) (Bank of Mexico's Economic Information System, SIE for its Spanish acronym). In this period, information availability and the possibility of having a homogeneous database was key, which was built for a total of 42 years - a period long enough to reaffirm what some studies conclude about Pemex profitability before TDC (Cornejo et al., 2012; Morales et al., 2013). For simplicity, Table 2 presents BS variables on an annual basis (in dollars and their averages), following the corresponding financial sequence.

Table 2 Pemex ’s financial balance, 1977 - 2019 (US$)

Source(s): Own calculations based on Pemex (2019a) and SIE (2019

Procedure

The VAR model has been useful in several studies on oil price (Mirmirani and Cheng Li, 2004; García et al., 2018; Ali et al., 2018; Cologni and Manera, 2008; Muhammad et al., 2018). The analysis in Section 3 allowed identifying some important relationships between oil price and BS variables, which can be verified with a VAR model, whose assumptions are that the series used are non-stationary and that there are lagged effects with each other and with the variables. Furthermore, there is endogeneity among variables; at one end, the selected variables depend on each other. The dynamic relationships of variables are analyzed with the Granger causality test, which determines causality unidirectionality or bidirectionality, and the IRF, which estimates the magnitude and persistence of the responses of variables to unexpected shocks (Ismail et al., 2021; Kamaljit and Vashishtha, 2020). The VAR model accommodates the fact that Pemex management responds to conflicting interests that a linear model could not represent (Sims, 1982; Rodríguez, 2011). As mentioned, the findings of Iqbal and Shetty (2018) and ElFayoumi (2018), who applied the VAR model to analyze the impact of oil price variations at the company level, were the most useful. About the procedure, the augmented-Dickey-Fuller unit root test corroborates series stationarity. The lagged test, Akaike information criterion (AIC), determines the lagged effects of variables. The χ2 test obtains the significance level. The Granger causality test defines the unidirectional or multi-directional character of lagged values of variables; the significant relationships obtained are measured with the IRF (Ehrmann and Valla, 2003).

Results and analysis

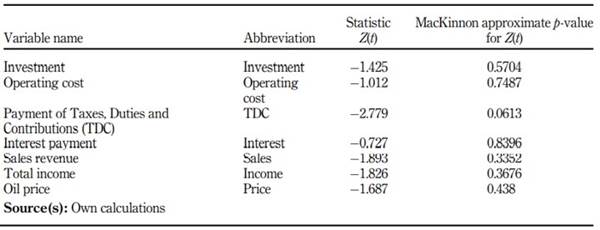

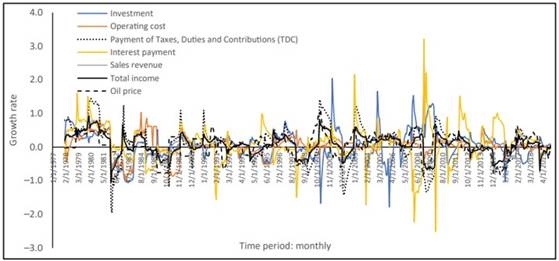

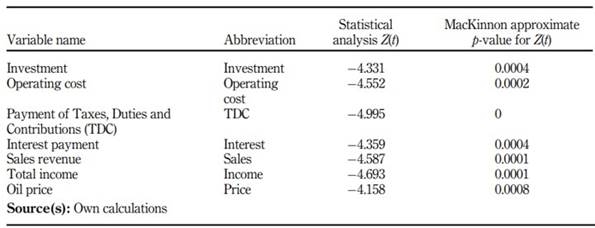

Figure 5 shows the original series. Pemex's financial indicators and the oil price show high volatility (short-term cycles, as well as stationary and random effects) and non-stationarity (a mean and variance that change through time, thus displaying a trend), which is confirmed by performing the augmented-Dickey-Fuller test for unit root (Table 3).

By applying a logarithmic transformation to obtain stationary data, a system of seven equations, with a 12-month difference is obtained as follows:

Growth in investment = ln(investment t ) - ln(investment t−12 ) (1)

Growth in operating cost = ln(operating cost t ) - ln(operating cost t−12 ) (2)

Growth in TDC = ln(TDCt t ) - ln(TDC t−12 ) (3)

Growth in interest = ln(interest t ) - ln(interest t−12 ) (4)

Growth in sales = ln(sales t ) - ln(sales t−12 ) (5)

Growth in income = ln(income t ) - ln(income t−12 ) (6)

Growth in price = ln(price t ) - ln(price t−12 ) (7)

New series are interpreted as annual growth rates (Figure 6). The unit root hypothesis is rejected using the augmented-Dickey-Fuller test, thus confirming stationarity (Table 4).

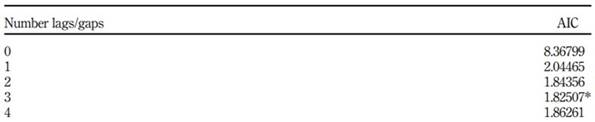

A multivariate time series regression analysis is performed. Assuming the variables' endogeneity, each variable growth is considered to be consecutively consistent with the growth of other variables or, if taken to an extreme, dependent on each other's growth. The VAR model rests on the premise that each variable helps to forecast the other ones, thus providing an equation system that is solved simultaneously and that allows characterizing its dynamics at different lag levels (Sims, 1982; Stock and Watson, 2001). The result of AIC lag test, which is used for knowing the lagged effects of a variable's performance on another variable, points to the inclusion of three lags in the model (Table 5).

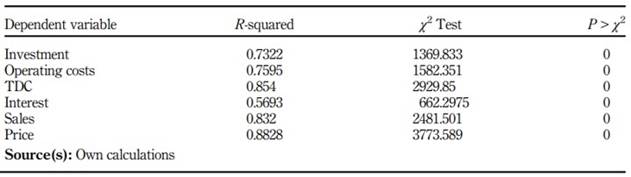

In the VAR model with three lags, there is a high degree of collinearity between the variables, total income and sales revenue (correlation of 0.99). This is because the second variable derives from the first one. The sales revenue variable was chosen due to its better fit to the model, thus leaving six out of seven initial equations. Table 6 shows the results on the goodness of fit.

The χ2 test indicates that all the equations are statistically significant. From R-squared values, which show the variations explained by the equations, the lowest one corresponds to Interest (0.56), while the highest corresponds to price (0.88). The remaining variables show an R-squared exceeding 0.72.

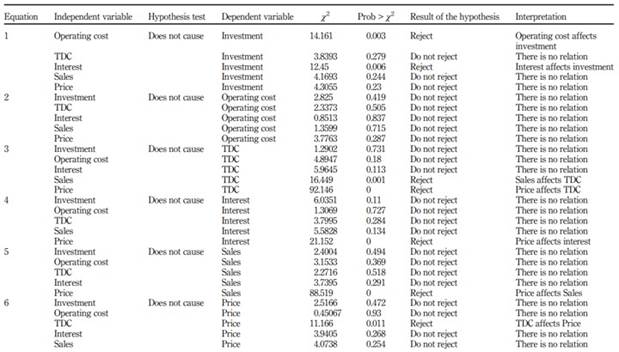

The Granger causality Wald test (Table 7) served to determine whether a variable's lagged values help to forecast another variable and whether they are unidirectional or multi-directional is validated (Stock and Watson, 2001; Ismail et al., 2021; Kamaljit and Vashishtha, 2020). In total, thirty relationships were assessed for the six equations, but only five relationships were statistically significant:

Table 7 Granger causality test

Note(s): The model meets the assumptions of not having auto-correlation and normality of the errors

Source(s): Own calculations

The growth rate of operating costs and interests is consistent with the growth rate of investment;

The growth rate of oil prices and sales revenue is consistent with the growth rate of TDC;

The growth rate of oil prices is consistent with the growth rate of interests;

The growth rate of oil prices is consistent with the growth rate of sales revenue and

The growth rate of TDC is consistent with the growth rate of oil prices.

It is worth noting that the operating cost equation (2) is unable to identify any causal relationship with other variables. There is not enough statistical evidence to assume that other variables are consistent with operating costs. Therefore, for this model, these expenses constitute a variable that depends solely on its trajectory through time. Table 8 summarizes the results.

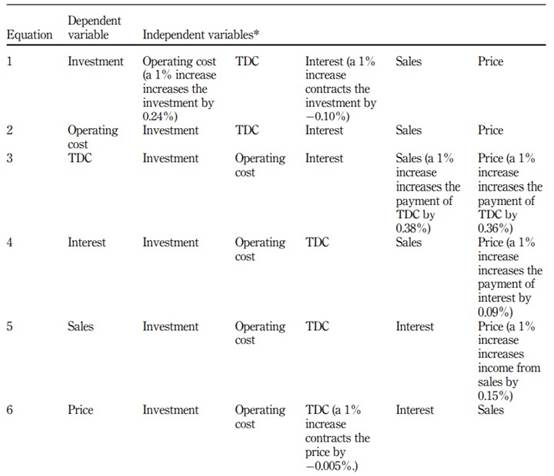

Table 8 VAR model results

Note(s): *The variables effect corresponds to the first month of the given time period

Source(s): Own elaboration based on data from Table 7

The significant relations obtained with the Granger causality test are measured using IRF over eight months as shown.

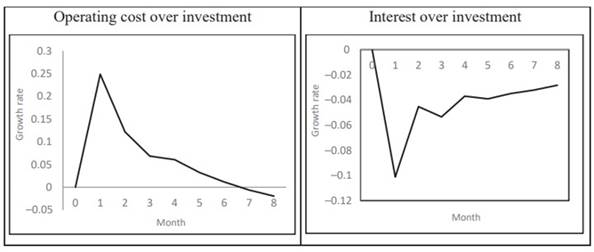

Operating cost, interest and investment

Increases in operating cost and interests have two effects on investment. The first one is positive. A 1% increase in operating cost causes an increase of 0.24% in investment, having a one-month lag which tends to disappear eventually. The second effect is negative. A 1% increase in interest reduces investment by −0.10%, whose effect also weakens over time. Based on the results from the VAR model, it is possible to state regarding the first relationship that although the operating cost had a positive impact on investment, there is no evidence suggesting that the first relationship is bidirectional. On the other hand, the negative effect of interest points to the persistent demand for resources caused by the cost of debt (see Figure 7).

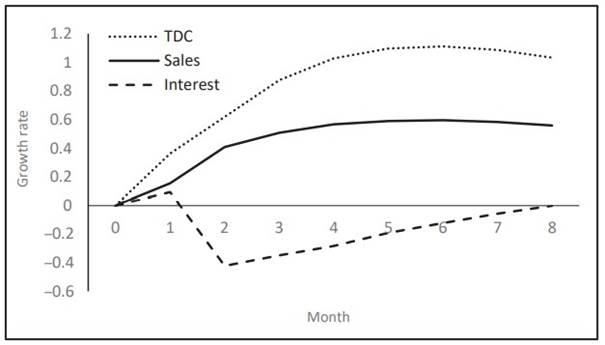

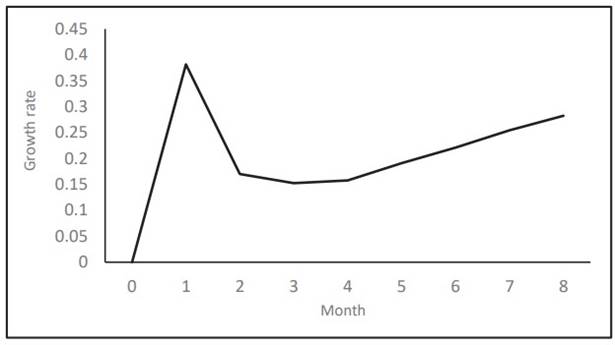

Price, TDC, sales and interest

The price influences three variables: TDC, sales and interests. Regarding TDC, the most significant relationship regarding price, a 1% increase in price causes an increase of 0.36% in TDC in the first month; in addition, it is the only variable exceeding 1% in the following months. For sales, of 1% increase in price causes an increase of 0.15% in sales in the first month, exceeding 0.50% in the following months; following the logical financial sequence, the effect of price must be first applied to income. Lastly, an increase of 1% in price causes an increase of 0.09% in interests in the first month. No robust evidence was found to suggest that increases in oil price or sales have an impact on investment; in other words, the variable is unrelated to price cycles and/or income. On the contrary, the most notable effect is the one that price has over TDC, which confirms the assumption about Pemex's poor-financial management, which is reflected by two facts: it provides a considerable portion of its profits for public financing and inadequate investment for the development of the energy sector (see Figure 8).

Sales and TDC

The impact of the Sales variable on TDC is another very important interaction and the result of the previous assumption. A 1% increase in Sales causes an increase of 0.38% in TDC in the first month and it remains positive in the following months (Figure 9). As shown in Figure 8, the price has an effect on TDC, but this effect is first reflected in the company's income, from which expenses are deducted to obtain the ending financial balance. Therefore, the behavior of the payment of TDC, which is related to an increase in sales, confirms the reduction of Pemex's financial margin to negative levels.

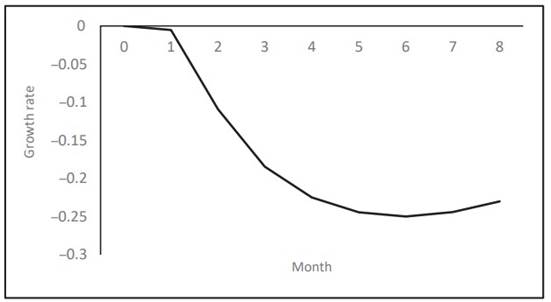

TDC and price

The payment of TDC negatively affects price. A 1% increase causes a decrease of −0.005% in the first month, which tends to worsen in the following months (see Figure 10). The interpretation here has to do with the nature of the price as a variable dictated by the international market (Cologni and Manera, 2008; Muhammad et al., 2018; Derbali et al., 2019). Pemex's stability and financial viability is assessed according to price volatility and the impact it has on its finances. If Pemex reacts by increasing TDC during high-price seasons, it would be sending a wrong message to the market; it would be considered insolvent to meet its current liabilities. Pemex is the only case in the world where price expansion does not increase investment but rather the tax cost of producing oil.

Analysis of results

From the obtained results, the most important ones are those showing a relationship between investment (1) and TDC (3) equations. The first equation shows that Pemex's physical and financial investments are unrelated to price cycles and sales; in other words, these do not have any impact on investment. It is worth noting that from 1977 to 2019 prices experienced increased seasons, staying at and even exceeding US$100 per barrel. The surplus generated from oil market dynamics, which in Mexico reported on an average annual extraordinary income of almost US$500,000m during a whole decade (2005-2014), was absorbed by the tax burden (SIE, 2019). The second equation shows that an increase in price and sales of 1% caused tax increases of 0.36 and 0.38%, respectively. In other words, the surplus resulting from price increases was extracted by increases in Pemex's tax burden and, on top of that, investment was not encouraged, all of which accounts for production cutbacks at every level of the oil production company (Fuentes and Cárdenas, 2010; Silva et al., 2021; Hernández and Bonilla, 2020).

On the other hand, investment would have a positive increase of 0.24% as a result of a 1% increase in operating cost; but considering equation (2) apart, it is also unrelated to price. In fact, it only depends on itself in the model. Therefore, labor, materials, maintenance costs and general services do not increase as price increases. On the contrary, Investment decreases when the payment of interest increases, a variable on which price did have a positive effect. Pemex is the most indebted company in the world, and since the company gets more resources during certain periods of price increases, incentives have been created to cover the cost of debt over other priorities; under normal conditions or during low-price periods, debt acquisition tends to increase in order to pay TDC (Fitch Ratings, 2020).

In general, the most notable result of the model is that price increases - reflected by financial sequence in business income growth - are absorbed by three variables, which in order of importance are as follows: TDC, sales and interests; on the other hand, it does not have any impact on the other two variables: investment and operating cost. From a corporate finance approach, Pemex lacks management oriented to value creation (Huizar, 2015; López and Nava, 2018). Strategic investment has not been considered in making long-term operational and financial decisions and it will not be if paying excessive taxes remains a structural problem. The results validate the working hypothesis: in Pemex financial management, the interest of using it for fiscal objectives prevails, and the oil price and corporate income derived from it do not have a positive impact on financial balance, since the entire effect is absorbed by TDC.

Discussion

Pemex manages a strategic resource for the Mexican economy and its contribution to public revenues is significant. The research corroborated with an empirical method (VAR model), which several studies have already analyzed about Pemex's fiscal burden (Fuentes and Cárdenas, 2010; Bazán and González, 2011; Cornejo et al., 2012; Morales et al., 2013; Anderson and Park, 2016). The information from the BS was essential. The influence of the oil price is easily corroborated in a “petro-state” like Mexico, but the most relevant thing was to know how it affected Pemex's corporate income and its distribution among the different financial expenditures of the company.

In that sense, the results of this research have important implications for Pemex's financial sustainability. In the realm of economic policy, they invite those responsible for the energy sector to evaluate the role it has played in the national economy. It is necessary to assess whether its finances are being managed in a balanced way and whether price expansions have really benefited from it. The results show that they have not. First, the relationship found between oil price and TDC is strong evidence of Pemex's fiscal role in the national economy and of its main function as a provider of public funds (Sánchez, 2016; Salazar and Venegas, 2018). Second, when weighing the price-investment relationship, it is also evidence of the negative impact that it generates on productivity, since it restricts investment in aspects such as infrastructure, technological development and human capital. The fiscal role of Pemex prevails, and according to the financial balance, the financial and productive cost of this is high, since oil revenues do not favor savings and investment (Huizar, 2015; Rodríguez and López, 2019). The main recommendation is that fiscal and energy policy should reconcile objectives, implementing a progressive tax reduction plan.

In the academic and research fields, a new perspective is provided by focusing on Pemex through its BS, which is a key instrument that until now the literature has overlooked. Knowing, in terms of accounting and quantitatively, the reaction of financial variables to price movements, in particular of TDC, is a significant contribution to studies that have worked on the issue of the tax burden but with a qualitative or quantitative perspective that fails to capture the real impact of the tax burden at a corporate scale (García et al., 2018; Sierra and Méndez, 2017; Durán-Encalada and Paucar-Cáceres, 2012). At the same time, it opens an opportunity to further explore the micro-economic part of Pemex in its different facets, since investment, in the results of the model, is not affected by price and is a fundamental variable at the corporate level due to its relationship with asset formation, productivity and competitiveness.

Conclusion

The research examined the impact of oil price on Pemex BS in the period 1977-2019. In the VAR model, the most significant relationship found with the Granger causality test and IRF was that of price - TDC. In the face of price increases, TDC also increased (immediately and over time). In contrast, there was no evidence that price affected Investment; it is a variable disconnected from price cycles. The benefit in total income from oil price expansions was diluted by subtracting TDC payment, which is the highest BS outlay. The revenue margin and profit after TDC were mostly negative; therefore, Pemex is a company managed for fiscal purposes.

The results managed to give quantitative support to the study of the Pemex tax burden. It is suggested that future research should approach Pemex from micro-economic, financial and accounting theory. For example, going deeper into the data of its BS or income statement, whose impacts are sectorial and macro-economic. It would be interesting to study how the investment affects the formation of public capital in the sector - derived from the null impact that the price of oil has on it, associating this concept with the investment destined for productive infrastructure, research, and development of technology - which is registered in its BS, or analyze the trajectory of Pemex's corporate debt, which is the highest in the world and takes away about 10% of its total annual income through interest payments. Both perspectives could have important political implications at the national, sectoral and corporate levels. Let us remember that oil revenues account for one-third of the country's income, which determines Pemex's fiscal burden, its disposable income and its capacity to finance investment.