English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mail Cited by SciELO

Cited by SciELO  Similars in

SciELO

Similars in

SciELO

Permalink

PermalinkIntroduction

This study investigates the behavioural aspect of budgetary slack as suggested by Daumoser et al. (2018 ), in particular, examines the effect of gender and code of ethics on budgetary slack ethical judgment. The behavioural aspect is essential because playing a role in decision-making ( Isidore R. and P., 2019 ). Budgetary slack has been viewed as a behavioural issue because it relates to the moral frame of the budgeting setting ( Hobson et al., 2011 ) and leads to dysfunctional budget behaviour ( Daumoser et al., 2018). While budgetary slack has attracted considerable attention, previous studies have focused on factors affecting budgetary slack: individual, organizational and social factors. Examples of individual elements are participation ( Adnan and Sulaiman, 2007 ; Dunk, 1993 ; Dunk and Nouri, 1998; Kren, 2003 ; Lukka, 1988 ; Maiga and Jacobs, 2007 ; Young, 1985 a), information asymmetry ( Chow et al., 1988 ; Douglas and Wier, 2000 ; Dunk, 1993 ; Dunk and Nouri, 1998; Onsi, 1973 ; Young, 1985b), ethical position (Douglas and Wier, 2000), personal values (Hobson et al., 2011), culture and religion (Adnan and Sulaiman, 2007), perceptions of fairness ( Özera and Yilmaz, 2011 ), individuals' organizational commitment (Yilmaz et al., 2014), trust between superiors and subordinates ( Chong and Ferdiansah, 2011 ), obedience pressure ( Davis et al., 2006 ) and mood ( Altenburger, 2021 ). Examples of organizational factors are the effectiveness of budget controls ( Kren, 2003; Özera and Yilmaz, 2011; Yilmaz and Özer, 2011), incentives (Douglas and Wier, 2000), pay schemes (Chow et al., 1988 ; Dunk and Nouri, 1998; Hobson et al., 2011; Waller, 1988 ) and superiors' ability to detect slack (Dunk and Nouri, 1998). Examples of social factors are environmental uncertainty and social pressure (; Young, 1985a). Additionally, budgetary slack has been studied in various contexts, such as industry sectors: manufacturing ( De Baerdemaeker and Bruggeman, 2015 ); Chemical (Nouri and Parker, 1996); and Non-Financial ( Damrongsukniwat et al., 2015 ), and countries: Malaysia (Adnan and Sulaiman, 2007); USA (Hobson et al., 2011); Nigeria ( Ajibolade and Akinniyi, 2013 ); Turkey (Yilmaz et al., 2014); Australia (Chong and Ferdiansah, 2011); and Indonesia ( Donna and Ningsih, 2020 ; Mareta et al., 2021 ; Wafiroh et al., 2020 ).

Douglas and Wier, 2000) argue that budgetary slack contains ethical issues because budgetary slack is not consistent with role-related norms and the desired virtues of professional managers and accountants. Hobson et al., 2011) argue that budgetary slack may pose a moral dilemma because it permits a subordinate to take excessive resources by deception. Such behaviour violates the expected social norms and standards of professional conduct ( Davis et al., 2006 ). However, research on budgetary slack using an ethical perspective is still limited (e.g. Douglas and Wier, 2000; Hobson et al., 2011; Stevens, 2002 ). This study attempts to add more empirical evidence on the effect of an individual aspect (gender) and organizational factor (code of ethics) on budgetary slack ethical judgment.

According to psychology theories ( Dawson, 1992 , 1995; Eagly, 1987 ; Gilligan, 1982 ), gender may be responsible for various types of assessments and behavioural intentions ( Shawver and Clements, 2015 ), and it is likely an antecedent of ethical judgment. So, examining the role of gender on budgetary slack righteous judgment is essential. For example, Beltramini et al. (1984 ) and Peterson et al. (2001 ) found that women are more concerned with ethical issues and see ethics as more critical than men. Therefore, this study investigates if women judge budgetary slack as more unethical than men.

A code of ethics is a written, separate, formal document consisting of moral standards that help guide employees or corporate behaviour ( Davidson and Stevens, 2013 ; Stevens, 1994). The code of ethics is investigated because the theory of social norms ( Bicchieri, 2006 ), known as the activation model of social norms, suggests that a code of ethics would improve the behaviour of managers in their decision-making (Davidson and Stevens, 2013). However, the Bicchieri's model suggests that social norms must be activated through situational cues to be effective. Therefore, this study examines if a code of ethics affects budgetary slack ethical judgment to provide evidence of whether a code of ethics can be used to activate social norms.

To examine the effect of gender and code of ethics on budgetary slack ethical judgment, we performed an experimental study. The participants are undergraduate and postgraduate accounting students at a major university in Indonesia who have taken management accounting and business ethics courses. The results show that gender affects budgetary slack ethical judgments. Compared to men, women assess budgetary slack as being more unethical. Further, the results show that the code of ethics also affects budgetary slack ethical judgment. This study finds that an individual supported by a code of ethics assesses budgetary slack as an action that is more unethical than individuals without such a code of ethics.

The rest of the paper is organized as follows. Section 2 reviews the previous relevant research and develops the hypotheses. Sections 3-5 explain the research method used, analysis and discussion. Finally, the conclusions are presented in Section 6.

Literature review

2.1 Ethical decision-making model and budgetary slack studies from an ethical perspective

The ethical decision-making model developed by Rest (1986 ) describes a four-step ethical decision-making process: moral sensitivity, moral judgment, moral intention and moral behaviour. Moral sensitivity exists when a moral agent acknowledges a situation that presents an ethical dilemma and has potential consequences that may affect others due to the behaviour of the moral agent. Moral judgment is assessing whether specific actions are morally right or wrong. The moral intention appears when someone chooses a particular action but has not yet to undertake it. Finally, ethical behaviour appears when an individual is involved in moral behaviour. We used Rest’s (1986 ) model because it is generalizable to various environments ( Jones, 1991 ). In this study, we emphasize moral judgment because moral judgment is typically considered the most crucial step of ethical decision-making in Rest’s (1986 ) model. It describes the determination of whether a course of action is morally right or wrong ( O'Fallon and Butterfield, 2005 ).

Previous research related to the ethical perspective on budgetary slack has been done by Douglas and Wier, 2000 ), Hobson et al., 2011) and Stevens, 2002). Douglas and Wier, 2000 examined the effect of ethical positions (relativism and idealism) on budgetary slack and found that ethical positions affect budgetary slack. Hobson et al., 2011) examined the effect of pay schemes and personal values on moral judgments of budgetary slack. Their results showed that participants with the slack-inducing pay scheme created budgetary slack, and the participants judged budgetary slack as an unethical act. Stevens, 2002examined the effect of reputation and ethical concerns on creating budgetary slack and found that budgetary slack is negatively associated with reputation and ethical considerations.

2.2 Gender and budgetary slack ethical judgment

Gender is one of the variables often used in business ethics research ( Nguyen and Biderman, 2008 ). Further, ( Nguyen and Biderman(2008) explain why the study of gender differences in ethical judgments (especially in business ethics) is widely used. With the influx of women into managerial-level positions or higher, understanding the ethics of women compared to men provides insights into how to build a positive ethical climate in a global company. In addition, the psychology literature explains that gender does matter for various types of judgment and behavioural intentions (Shawver and Clements, 2015).

Gender socialization theory explains that because gender identity is stable and does not change, the difference in the values, interests and nature of women and men in their work environments should lead to differences in the perception of ethics, and it grows more stable over time ( Dawson, 1992 , 1995). Men and women have personalities that develop from childhood. Therefore, their moral values and ethical views will vary throughout their lives (Dawson, 1992 ). This theory also explains that men and women are fundamentally different regarding their moral development. The diverse values lead to other forms of ethical behaviour and attitudes between women and men. According to this theory, men place value on money, progress, strength and the size of actual personal performance, while women concentrate more on harmonious relationships and helping others ( Clikeman et al., 2001 ).

Beltramini et al. (1984) and Peterson et al. (2001 ) found that women are more concerned with ethical issues and see ethics as more critical than men. Akaah (1989 ) found that women have more significant ethical concerns than men. This research lays on Eynon et al. (1997 ), which showed that women have higher moral reasoning than men. Weeks et al. (1999 ) showed differences between the ethical judgments of men and women, in which women demonstrated a higher ethical judgment in 7 of 19 scenarios while men showed a higher ethical assessment in 2 of the 19 scenarios. Valentine and Rittenburg (2007 ) found that professional businesswomen have a higher ethical judgment than experienced businesspeople. ( Nguyen and Biderman, 2008) suggested that the moral judgment of female students is higher than that of male students. Sweeney et al. (2010 ) found that the ethical decision of women is higher than that of men. Therefore, the first hypothesis is as follows:

H1. Women will judge budgetary slack as more unethical than men.

2.3 Code of ethics and budgetary slack ethical judgment

Altenburger (2017 ) stated that contextual factors might considerably influence budget reporting honesty. Further, Altenburger (2017 ) investigated the impact of descriptive social norms on managerial honesty and concluded that injunctive norms could considerably influence managers' budget reporting behaviour because many people conform to the preferences of their peer group.

To develop the hypothesis that a code of ethics affects budgetary slack ethical judgments, we use the theory of social norms (Bicchieri, 2006), known as the activation model of social norms. The social norms theory explains norms in terms of the expectations and preferences of those who follow these norms. The existence of a norm depends on an adequate number of people who believe that such a norm exists and is associated with specific situations (Bicchieri, 2006). Bicchieri provides an operational definition of the activation of the social norms that generate meaningful predictions that can be tested ( Davidson and Stevens, 2013 ). The Bicchieri's model shows how people can take a particular context and then map it into a specific interpretation that shapes their beliefs and expectations about the motives and behaviour of people, and especially the activation of social norms that creates relevant beliefs and expectations that impact behaviour (Davidson and Stevens, 2013).

Bicchieri's models of social norms' activation include a contingency or initial condition that must be met before a social norm is activated (Bicchieri, 2006). The contingency or initial condition presents the foundational condition necessary for a social norm to be activated. This condition states that individuals know that a behavioural rule exists and applies to specific conditions or situations. The three conditions of a conditional preference are (a) Empirical expectations, a condition where an individual believes that a sufficiently large subset of the population conforms to behavioural rules in certain situations; (b) Normative expectations, a condition where an individual believes that a sufficiently large subset of the population expects individuals to conform to behavioural rules in certain situations; and (c) Normative expectations with sanctions, a condition where an individual believes that a sufficiently large subset of the population expects individuals to conform to behavioural rules in certain situations, prefers individuals to conform and provides penalties or rewards. Bicchieri's model suggests the activation of the norms through situational cues to be effective, and in this study, we use a code of ethics.

Codes of ethics are generally included in social norms. A code of ethics is generally the norms, rules and principles accepted by a group as a foundation or guidelines for the group's behaviour and its people. A code of ethics aims to ensure that professional people act appropriately, following the existing approaches. A code of ethics is one way to improve the organizational climate to behave ethically ( Adams et al., 2001 ). By most definitions, a code of ethics is a written, separate, formal document that consists of moral standards that help guide employees or corporate behaviour ( Schwartz, 2002 ). It is developed to guide individual behaviour and can be used to take punitive action against any of its employees who indulges in illegal or unethical behaviour ( Adams et al., 2001). Companies generally develop their codes of ethics to reduce ambiguity, improve ethical practices and establish strong work ethics ( Ibrahim et al., 2009 ).

Hegarty and Sims (1979 ) conducted a study using a field experiment with undergraduate students who studied philosophy and organizational policies as their participants. The results showed that a code of conduct positively relates to ethical decision-making. Laczniak and Inderrieden (1987 ) found that a code of conduct incorporating sanctions led to more ethical behaviour. McCabe et al. (1996 ) conducted a study of 318 people in business and found that a code of ethics is positively related to ethical behaviour. McCabe et al. (1996 , supported by Adams et al., 2001), found that individuals who work in an organization with a code of ethics are more ethical than individuals without a code of ethics. Pflugrath et al. (2007 ) found that the existence of a code of ethics significantly affected the professional judgment of accountants undertaking audits. McKinney et al. (2010 ) showed that business professionals who work in a company with a written code of ethics are less likely to accept an ethically unclear situation than business professionals who work in companies that do not have a code of ethics.

Codes of ethics are the external factors that predict the effect of budgetary slack ethical judgments ( Hobson et al., 2011). The theory of social norms and moral decision-making indicates that a code of ethics would affect ethical judgments of budgetary slack. Companies with a positive code of ethics will improve individuals' decisions and ethical beliefs ( Ford and Richardson, 1994 ). Booth and Schulz (2004 ) explained that a code of ethics also increases the perception that the organization is more concerned about ethical behaviour. Therefore, the second hypothesis is formulated as follows:

H2. Individuals supported by a code of ethics will judge budgetary slack as more unethical than individuals not supported by a code of ethics.

2.4 Budgetary slack studies and accountant code of ethics in the Indonesia context

Previous sections show that budgetary slack studies have been conducted extensively. However, budgetary slack studies from an ethical perspective are limited. Similar phenomena happen in Indonesia but with lower intensity. This study uses the Indonesia context because it has rarely been the focus of the research ( Fuad et al., 2019 ) despite its market and economic potential. Besides, research in developing countries is still limited ( Al-Harbi, 2019 ; Isola et al., 2020 ). Among recent studies of budgetary slack in Indonesia are Donna and Ningsih, 2020), Mareta et al., 2021 ) and Wafiroh et al., 2020 ). Donna and Ningsih, 2020) found that budget usage negatively affects budgetary slack, and budget participation mediates the relationship between budget usage and budgetary slack. Mareta et al., 2021 found that obsessive supervisors and locus of control influence budgetary slack. Wafiroh et al., 2020) found that high participation in budgeting leads to a decrease in the creation of budgetary slack. Our study is the first to investigate the relationship between budgetary slack and the code of ethics in the Indonesian context.

Studying budgetary slack from an ethical perspective in Indonesia is particularly important because recently, in July 2020, the Institute of Indonesia Chartered Accountants (IAI) just launched the revised moral codes of conduct (IAI, 2020). Hence, it is essential to examine whether the code of ethics can activate social norms among Indonesian accountants (candidates), namely, accounting students.

Method

3.1 Experimental design

This study uses a 2 × 3 mixed factorial design experiment. The mixed factorial design tests the effect of a combination of situational factors on the participants' variables (subject variable) ( Leary, 2012 ). We use the mixed factorial design in this study because it allows researchers to determine whether certain independent variables apply to all the participants or just to those with specific attributes (e.g. female-to-male) and to understand how specific personality characteristics relate to their behaviour under various conditions. The experiment design in this study involves one independent variable, i.e. a code of ethics manipulated in three levels: no code of ethics, a code of ethics without sanctions and a code of ethics with sanctions, and gender: women and men.

3.2 Participants and experimental procedures

The participants in this study are undergraduate and postgraduate accounting students at a major university in Indonesia who have taken management accounting and business ethics. The criteria to ensure that they understand the scenario used in this experiment related to budget and ethical decision-making. Students are used as participants and surrogates for managers because the design does not require managerial experience to understand and make righteous judgments.

The participants were randomized into three cells (no code of ethics, a code of ethics without sanctions and a code of ethics with sanctions). They received information about three experimental scenarios. At the end of the task, participants completed an exit questionnaire. The exit questionnaire gathered demographic data and personal perceptions. Response to perception statements on the exit questionnaire suggests that our experimental controls and manipulations were adequate.

Experimental research must have high internal validity. We conducted manipulation check procedures and scenario internalization to maintain high internal validity. Additionally, we performed a series of initial tests (pilot tests). We used randomization designed to address the historical and regression threats. In addition, experiment tasks took place in classrooms with the same environmental management. We did not experiment long duration (it takes only 30-45 min) to overcome the maturation and mortality threats. The experimental procedure is short and clear so that it is easy to understand by the participants. This study used different participants for pilot tests and main experimentation to overcome the testing effect. The instrumentation threat is addressed by the instrument design discussed with practitioners and academics and has passed initial tests (two pilot tests). To obtain adequate external validity of research, we paid attention to the aspects of ecological validity. Experimental manipulation scenarios were designed with realistic or reality-like situations to generalize the research results to the natural environment.

3.3 Measures: independent and dependent variables

The independent variables in this study are gender (individual factor) and code of ethics (organizational factor). We used a code of ethics instrument initially developed by Davidson and Stevens, 2013), which refers to Sarbanes-Oxley (SOX) Section 406 (c) and the decision of the Securities Exchange Commission (SEC) in connection with the disclosure requirements of the code of conduct. The code used in the experiment is consistent with those requirements, which refer to the general social norms of honesty, integrity, responsibility and fairness. However, the instrument of Davidson and Stevens (2013) was modified and developed in the context of budgetary slack. As a result, we modified the instrument to fit the requirements of our three cells (no code of ethics, code of ethics without sanctions and code of ethics with sanctions).

The dependent variable is a budgetary slack ethical judgment. The instrument used in this study is an extension of the previous research, i.e. Hobson et al., 2011) and Hartmann and Maas (2010 ). The instrument was developed by discussing it with experts in the field of management accounting and experiment research. The question used is whether budgetary slack action undertaken by a manager is a very unethical act or a very ethical one. The response to this question was measured using a Likert-type scale ranging from 1, “very unethical” to 7, “very ethical”, with 4 being “moderate”.

Results

4.1 Manipulation check and descriptive statistics

One hundred two people participated in this experiment, consisting of undergraduate and postgraduate accounting students at a major university in Indonesia, representing around 5% of the population. Regarding the instrument, before being used in the experiment, it was pilot tested. The pilot test helped give an idea of the quality and effectiveness of the manipulation. The pilot test took place on a group of undergraduate and postgraduate students studying accounting. The pilot study was conducted three times. The first pilot test showed that 40% of the manipulation check failed. We then revised the instrument and the manipulation design based on inputs from the first pilot test. After getting revised, the instrument was tested again. The second pilot test produced better results as the failure of the manipulation check decreased to 20%. A third pilot test was delivered to obtain a reasonable assurance that manipulation was successful. The third pilot test showed better results as the failure of the manipulation check was 9.5%.

The manipulation checks for the code of ethics (no code of ethics, code of ethics without sanctions and code of ethics with sanctions) were performed using two questions. The first question was, “Does the company have a code of ethics?”. The answer was either “Yes” or “No”. The second question was, “Does the company have a code of ethics with clear sanctions?”. Again, the answer was either “Yes” or “No”. The results showed that the experimental manipulation and controls had been effective.

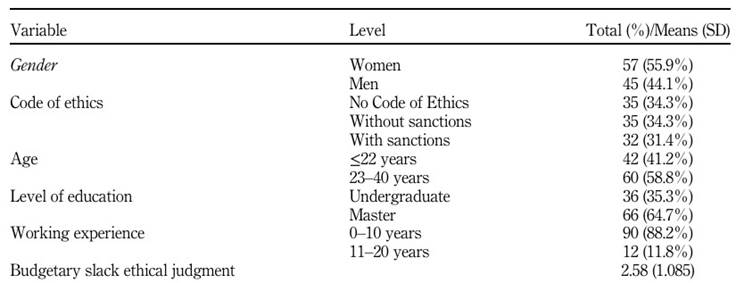

The gender variable consists of men and women, with 57 (55.9%) female participants and 45 (44.1%) male participants. The manipulated variable is the code of ethics which consists of three levels: without a code of ethics (35 participants, 34.3%), with a code of ethics without sanctions (35 participants, 34.3%) and with a code of ethics and with sanctions (32 participants, 31.4%). Budgetary slack ethical judgment has an average value of 2.58 (SD = 1.085). Overall, the results show that the participants judged budgetary slack as an unethical act. Table 1 describes the descriptive statistics of the participant's characteristics and control variables.

4.2 Hypothesis testing

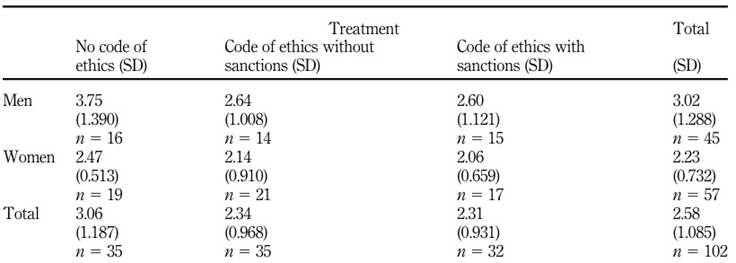

Table 2 illustrates the mean of ethical judgment, the standard deviation and the number of subjects in each cell. Table 2 shows that women had a mean of 2.23 and a standard deviation of 0.732, which is lower than the men's mean of 3.02 and a standard deviation of 1.288. The mean difference provides initial support that women assess budgetary slack as being more unethical than men. The code of ethics without sanctions showed a mean of 2.34 and a standard deviation of 0.968, which is lower than the mean of no code of ethics (3.06), and the standard deviation is 1.187. The code of ethics with sanctions showed a mean of 2.31 and a standard deviation of 0.931, which is lower than no code of ethics (mean = 3.06 and standard deviation = 1.187) and lower than the code of ethics without sanctions (mean = 2.34 and standard deviation = 0.968). The results provide initial support that budgetary slack was judged to be unethical when a code of ethics exists compared to no code of ethics.

To test the two hypotheses proposed, we use an ANOVA test. The test results show that the difference in budgetary slack ethical judgment is statistically significant (F = 15.396, p = 0.000) between men and women. Therefore, the first hypothesis is supported. Furthermore, the results showed that compared to men, women would judge budgetary slack as a more unethical act.

Hypothesis 2 states that individuals supported by a code of ethics will judge budgetary slack as more unethical than individuals not supported by a code of ethics. Table 2 shows that the mean difference between the cell without a code of ethics is 3.06 (SD = 1.187), the mean of the cell with a code of ethics but without sanctions is 2.34 (SD = 0.968) and the mean of the cell with a code of ethics with sanctions is 2.31 (SD = 0.931). Table 2 shows that the average of the cell without a code of ethics is higher than that of the other two cells. The ANOVA test results showed that the difference among all the cells was statistically significant (F = 5.675, p = 0.005). These results show that the second hypothesis is supported.

Bearing that significant differences exist between the three levels of the code of ethics, we then performed a post hoc test to see which cells of the code of ethics were different and distinct. The results of the post hoc test showed some empirical evidence. Firstly, the difference in budgetary slack ethical judgment between the cell of no code of ethics and the code of ethics without sanctions produced a significant result (p = 0.013). This result explains that individuals supported by the code of ethics without sanction judge budgetary slack as an action that is more unethical compared to individuals who are not supported by the code of ethics. Secondly, there is a significant difference between the cell of no code of ethics and the code of ethics with sanctions (p = 0.012). This result explains that individuals supported by a code of conduct with sanctions judge budgetary slack as an action that is more unethical compared to individuals who are not supported by a code of ethics. Thirdly, there was no significant difference between the cell of a code of ethics without sanctions and a code of ethics with sanctions (p = 0.992).

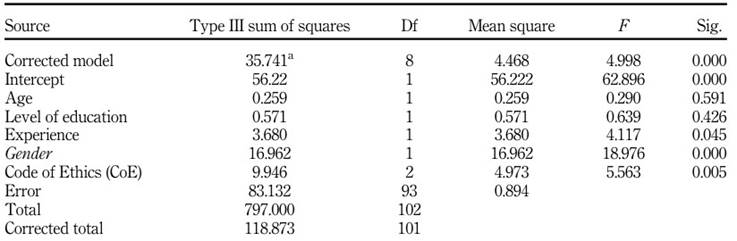

This study used a control variable or a covariate to see if other variables affect the budgetary slack ethical judgment other than the independent variables. The control variables used in this study were age, level of education and experience. Age, level of education and experience were used as covariate variables because the characteristics of participants may affect the results. An analysis of covariance (ANCOVA) was used to see any possible confounding effects in the experiment caused by age, level of education and experience.

The ANCOVA test results are shown in Table 3 . The ANCOVA test showed that the variable age (p = 0.591) and level of education (p = 0.426) did not significantly affect the ethical judgment about budgetary slack. In contrast, the variable experience had a significant effect (p = 0.045) on the budgetary slack righteous judgment. The ANCOVA test results also show that gender and code of ethics significantly impact budgetary slack ethical judgments (p values = 0.000 and 0.005, respectively) even when control variables are included in the test. These results increase the robustness of the findings tested using the ANOVA test. Overall, the results support hypotheses 1 and 2.

Discussion

The results of the ANOVA test showed that the difference in budgetary slack ethical judgment is statistically significant (F = 15.396, p = 0.000) between men and women. Additionally, the difference in budgetary slack moral judgment is statistically significant between the group without a code of ethics, the group with a code of ethics but without sanctions and the group with a code of ethics and with sanctions (F = 5.675, p = 0.005). Further, the results of the ANCOVA test show that gender and code of ethics are still significant in affecting budgetary slack ethical judgments (p values = 0.000 and 0.005, respectively) even when control variables are included in the test. Those results provide both theoretical and practical implications as follows.

5.1 Theoretical implications

The result supports the gender socialization theory (Dawson, 1992 , 1995). The theory explains that men and women are fundamentally different in their moral development and values, leading to varying forms of ethical behaviour and attitudes for women and men. Gender socialization asserts that males and females have distinct differences in their ethical decision-making processes ( Gilligan, 1982 ). Men advocate impartial, moral justice and rely on rules such as those embodied in state and federal laws, and women make moral judgments more contextually based and involve concerns for interpersonal needs and emotions ( Smith and Oakley, 1997 ). Additionally, the results of this study are consistent with Chung and Monroe (2003 ), Sweeney et al., 2010 ), Valentine and Rittenburg (2007 ), Weeks et al. (1999 ), ( Nguyen and Biderman, 2008), Dalton and Ortegren (2011 ) and Shawver and Clements (2015).

The result is also consistent with the theory of social norms by Bicchieri (2006) where individuals' ethical judgment is affected by specific activation of social norms; in this study, codes of ethics exist. Social norms often guide behaviour in particular contexts, and often they need to be activated ( Biel and Thøgersen, 2007 ). Verplanken and Aarts (1999 ) stated that relevant cues activate habitual behaviour in the environment, and the sequence of acts reveals itself with little attention paid by the actor. Bicchieri's model suggests that social norms must be activated through situational cues to be effective. This study shows that the existence of a code of ethics is one way to start social norms. In addition, a code of ethics may improve the organizational climate to support corporate members to behave ethically and avoid unethical behaviours. This study is consistent with the findings of Adams et al. (2001), Hegarty and Sims (1979), Laczniak and Inderrieden (1987 ), McCabe et al. (1996 ), McKinney et al. (2010 ) and Pflugrath et al. (2007 ).

5.2 Practical implications

The results show that individuals supported by the code of ethics without sanction judge budgetary slack as an action that is more unethical compared to individuals not supported by the code of ethics. Moreover, this result shows that individuals supported by a code of conduct with sanctions judge budgetary slack as an action that is more unethical compared to individuals not supported by a code of ethics. However, there was no significant difference between individuals supported by a code of ethics without sanctions and individuals with a code of ethics with sanctions. The results suggest that a code of conduct is more important than sanctions. Therefore, organizations should develop and implement a code of ethics.

5.3 Future research agenda

As the current study only used one individual factor, namely, gender, future studies should use other individual factors that may influence the budgetary slack ethical judgment, such as regulatory focus, personal values and religiousness. In addition, further studies can include practitioners as participants and see if there is a difference in budgetary slack ethical judgment between student participants and practitioner participants, which would improve the external validity.

Conclusions

This study examines whether gender and codes of ethics influence budgetary slack ethical judgment. The results show that women judge budgetary slack as more unethical behaviour than men. Moreover, the result indicates that individuals supported by a code of ethics consider budgetary slack as an action that is more unethical than those not supported by a code of ethics. The results explain that gender and code of ethics affect budgetary slack ethical judgment.

This study contributes to managerial accounting research by understanding the moral content of budgeting. Given the results of this study, budgetary slack is seen as containing an ethical issue. Another contribution of this research is to develop an experimental scenario for budgetary slack ethical judgment and code of ethics. This study also contributes to the practice related to ethical issues, especially among accountants, since a professional code of ethics is needed to improve accountants' ethical judgment a professional code of ethics is needed. With a professional code of ethics, they would be expected to behave ethically and appropriately, following the ethical guidelines that exist. It suggests that every profession and organization should develop a code of ethics.

This study has some limitations that may affect the external and internal validity of the experiment. Firstly, the data were collected in a classroom setting. Although the classroom setting was controlled in such a way as to retain its internal validity, there may still exist the possibility of external validity problems. Secondly, the possibility of cognitive limitations could have made it difficult for the participants to determine their behaviour in the situation described in the scenario. Thirdly, although the procedure endeavoured to be as close to natural conditions as possible, the participants' answers may still be influenced by the innate beliefs inherent in the participants.