Servicios Personalizados

Revista

Articulo

texto en

texto en  Inglés (pdf)

Inglés (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Enviar articulo por email

Enviar articulo por emailIndicadores

-

Citado por SciELO

Citado por SciELO

Links relacionados

-

Similares en

SciELO

Similares en

SciELO

Compartir

Permalink

PermalinkComuni@cción

versión impresa ISSN 2219-7168

Comuni@cción vol.11 no.1 Puno ene./jun 2020

http://dx.doi.org/10.33595/2226-1478.11.1.393

Original article

Accountability in the management of the municipal government of Puno-Peru (2011-2018)

1National University of the Altiplano, Puno, Peru

In the management of municipal governments, access to information and transparency on public investment and budget execution is very restricted, since semi-annual or annual reports are generally accessed with reluctance and limitations, which makes not only effective the social control but also accountability. The research aimed to understand the mechanisms of the accountability process that is implemented in the management of the municipal government of Puno. The study is of a documentary and qualitative nature. The empirical reference is based on the analysis of information corresponding to the financial years of 2011 - 2018. The results are: Accountability in the management of the municipal government of Puno conditioned by the political will of the municipal authorities and officials and in the Institutionalization of participatory mechanisms for access to information and transparency denotes a partial nature, of an aggregate nature and not very representative, expressed in public hearings. The aspects considered emphasize the legislative work, the budget report, the prioritized projects and the consolidated expenses and investment report, which were very global in nature. The limited representation is expressed in that the participants in the public hearings were the directors of the construction management committees, the users of the prioritized projects and sympathizers of the political organization of the municipal authority. Conclusion: The accountability process of the municipal government of Puno implemented through centralized or decentralized public hearings, had a partial, aggregate character and limited representativeness.

Keywords: Local government; public investment; access to information; transparency; accountability

INTRODUCTION

In Peru and Latin America, within the framework of the process of decentralization and modernization of the State, since the beginning of the 90s of the last century, the spaces (local coordination council, consultation groups, management committees) and mechanisms (plan concerted development, participatory budgeting, social control, and accountability) of citizen participation that influence the democratization of the management of regional and local governments (Tumi, 2015); laying the basic conditions for the consolidation of a democratic management, whose limits and possibilities in light of the relatively favorable juridic-legal framework, have been evidenced by various studies.

Indeed, on the one hand, in Peru, the rule of law that strengthens the democratization of public management, transparency and accountability is expressed in a favorable juridic-legal framework: reform of the Political Constitution (Law 27680) that establishes the citizens' right to participate in public affairs and the law on transparency and access to public information (Law N° 27806) recognize as rights of social control the revocation and removal of authorities and the demand for accountability; The organic law of municipal governments (Law N° 27972) establishes mechanisms of social control that is expressed in the implementation of citizen surveillance and accountability.

On the other hand, various studies refer to the incidence of the participatory budget (PP) in the democratization of public investment: Montecinos (2014) points out the importance of institutional design and citizen participation in the participatory budgeting process; Goldfrank (2006) holds that even where the mayors were committed to the PP, the problems of extreme dependency remained on scarce and unreliable transfers from the central government, and a fragmented civil society with little interest in institutionalized participation; In turn, Valverde, Gutiérrez, & García, (2013) emphasize the example of participatory budgeting as elements that contribute to the consolidation and improvement of the quality of democracy, but whose impact (as revealed by the budget exercises participatory in Mexico City) is still in its infancy; as well as Jiménez (2012), emphasizes the importance of social accounting as a requirement of transparency and accountability in public management in the perspective of the consolidation of democracy.

Likewise, in relation to the democratization of public investment via civil society organizations, Rocchi & Venticinque (2010) state that the democratizing potential of citizen participation is linked to the possibility of introducing through it an alteration in asymmetries of political representation; while Cardona (2012), analyzes the relations between the State and society generated by citizen oversight to promote the effectiveness of local public management. On the contrary, Pastor (2004), maintains that a democratic learning of the participating actors does not emerge, nor has it been possible to consolidate positions of collective political action, observing skepticism, immobility, distrust and a certain institutionalized inertia about forms and possibilities of citizen participation in public management.

Therefore, accountability is part of the democratization process of public management and consequently within the consolidation of democracy, good governance and the construction of active and effective citizenship.

Notwithstanding this, in the municipalities, access to information on budget formulation, distribution and execution is very restricted, which limits the monitoring, control and transparency of management; that according to Baca (2006) with difficulties (if the mayor so wishes) the semiannual reports are accessed two or three months late. This hinders or conditions citizen surveillance actions.

Likewise, in most local governments, accountability for public investment, through reports or public hearings, is limited only to the superficial or generic presentation of accounts by municipal authorities and officials on participatory budget agreements. and the investment budget; whose process is totally limited and deficient, lacking detailed and procedural information.

In the municipal government of Puno, despite the fact that there have been important changes in the access to information and transparency of public investment based on citizen participation and the political will of the municipal authorities, the processes, results and impacts obtained are little known or little spread.

Faced with this complex problem and multiple determinations, the study is aimed at understanding the accountability process that has been implemented in the management of the municipal government of Puno-Peru in the 2011-2014 and 2015-2018 management.

THEORETICAL FRAMEWORK

The theoretical perspective of the study takes as its starting point the concept of accountability and the characterization of the country's context. Accountability according to Ackerman (2008) and shared in some components by Bolaños (2010), is a dynamic, proactive process through which public servants report, explain and justify their action plans, performance and achievements and subject to the corresponding penalties and rewards. While the current context of Peru is marked by advances in the country's decentralization process, the modernization of the State and the democratization of public management, especially sub-national (regional and local).

In this framework, the theoretical model of the research is circumscribed within the challenge and strategic challenge of building a solid Rule of Law, an effective system of accountability and a transparent sub-national (regional and local) government:

On the rule of law, Cossío (2008) highlights the role that transparency plays in strengthening the rule of law; while O'Donnell (2000) emphasizes the relationship between the rule of law and democracy; Holmes (2008) refers to political plurality combined with active and even combative and irreverent citizenship as essential elements for the construction of a democratic State of Law.

On accountability, Fox (2008) maintains that it has a soft face (giving answers) and a hard face (which includes sanctions) and offers a roadmap for the transit from access to information to a full regime. accountability; while Mashaw (2008) proposes a useful new taxonomy of the accountability regimes that occur in the public, private and society sectors; Hernández (2009) raises the need for an ethical concept of accountability; Melossi (1992) relates accountability to social control as the basis for the consolidation of democracy; Peruzzotti (2007) conceives the issue by articulating citizen participation and the control and oversight agencies; In turn, Franciskovic (2013), as a public management challenge, relates accountability to the results-based budget.

On the construction of a transparent sub-national (regional or local) government: Merino (2008) emphasizes the need to articulate a vision of transparency as public policy, as an organizational value that allows a qualitative transformation in the way power is managed. administrative Arellano (2008); it refers to the complementary factors that configure access to public information in a new public management (effective surveillance, organizational restructuring and reform of administrative procedures); Gutiérrez (2004) conceives access to public information and transparency within public management; Naessens (2010) emphasizes the importance of ethics and transparency as essential factors in the construction of good governance; while Emmerich (2004) from a global perspective conceives transparency, accountability, citizen participation articulated to government responsibility.

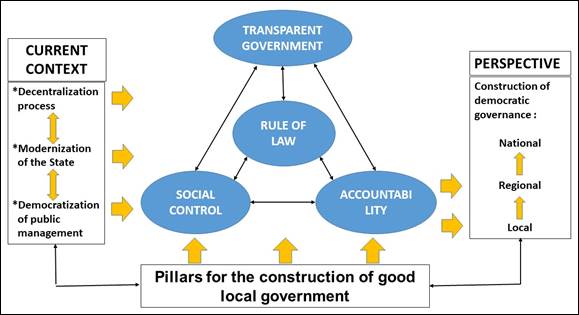

Consequently, the theoretical model considers that the dialectically articulated components are configured in the fundamental pillars of the construction of good local government (BGL)

and of citizenship (active and effective) in the perspective of the construction of local democratic governance, regional and national (Figure 1).

Figure 1 Theoretical perspective: Good Governance and the construction of Local Democratic Governance.

Within this perspective, accountability and social control are two sides of the same process (Cunill, 2007) that affect the possibilities of institutionalizing social accounting (Peruzzotti & Smulovitz, 2002) based on citizen participation in public management (Peruzzotti, 2007) and the quality of democracy (López & Hincapié, 2014); whose level and degree of effectiveness is conditioned by the political will of the municipal authorities and officials and the social will of civil society organizations expressed in the degree of strengthening of their internal democracy, dynamism, propositional capacity and strategic vision.

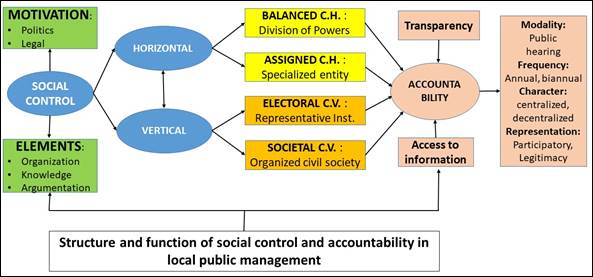

Therefore, according to the preceding approaches (Cunill, Smulovitz, Peruzzotti, López & Hincapie) and in accordance with the juridic-legal framework, the process of analysis of social control (citizen surveillance) as a right that civil society has and the surrender of accounts as the responsibility of the municipal authority (political will) in local public management in the perspective of building good local government (BGL) considers the following elements of structure and function (Figure 2).

In sum, the democratization process of local public management, given its importance, is configured as a strategic challenge for both municipal authorities and officials in the possibility of carrying out transparent, democratic and participatory management and a consistent accountability process not only with the juridic-legal framework but with the political will; and for civil society, in its role of effective social surveillance and control.

METHODOLOGY

The research is of a documentary and qualitative nature; as it seeks to account for the scope of accountability in the democratization of investment in the municipal government of Puno. The information collection process was carried out in 2014 to analyze the management of the mayor Luis Butrón Castillo and in 2018 to analyze the management of the mayor Iván Flores Quispe.

The theoretical population was made up of managers of local civil society organizations, who are configured as potential participants in public accountability hearings. The type of sampling was non-probabilistic, in the modalities combined for convenience and saturation: For convenience, given that the selection of the analysis units was focused on the degree of interest of the participating agents in the issue of accountability. The in-depth interview guide was applied until reaching the degree of saturation. Thanks to which, the operational population was 56 participating agents.

The techniques and instruments for collecting information were through secondary and primary sources. Documentary sources: Accountability reports, annual reports on budget execution, transparency website and portal, review of minutes of the participatory budgeting process; analysis of other sources (magazines, radio and television spots, bulletins) that report mechanisms of access to information that the municipal authorities establish for the accountability of public management. Primary sources: In-depth interviews with executives of social organizations, authorities and municipal officials. Observation of accountability hearings.

The information was processed with the Atlas ti software; The interpretation was made based on the construction of hermeneutical maps and analysis techniques of content and meaning relative to capturing the perception of the profile of the municipal authority, the performance of municipal management and respect for the autonomy of the organizations of civil society, the timeline of public hearings and content analysis of annual reports.

RESULTS AND DISCUSSION

The scope of accountability in the management of the municipal government of Puno can be seen in the rule of law and political will of municipal authorities, investment priorities, access to information, transparency and dynamics of public hearings.

Ethics and rule of law: Profile and political will of the municipal authorities

a) Municipal authority profile

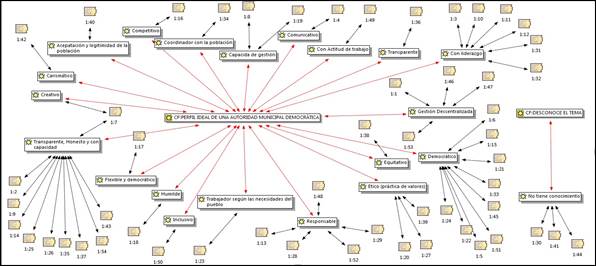

The municipal authorities, in the perception of the social and institutional actors, have the following basic features that characterize their profile (Figure 3):

The democratic authority must undertake the task of informing, training and persuading, dialoguing with society and sharing a vision on common objectives; When there are authorities with a concerted and participatory political will, people think that “there is a future” and assume, as a practical effect, their own modes of coexistence and interaction.

Thanks to which, the authority should be concerned with contributing to the construction of not only active citizenship (with knowledge and exercise of their rights and knowledge and fulfillment of their responsibilities) but the formation of effective citizenship; as well as the emergence of new leaders with strategic thinking and vision.

Therefore, the democratic nature of the municipal authority (mayor and councilors), in the perception of the members and directors of local civil society organizations, should be expressed in the way how concerted and participatory management is implemented, based on delegation of functions, demonstrating and modeling transparency in the management of public affairs and empowering civil society in co-management with a sense of co-responsibility.

b) Performance of the municipal authority

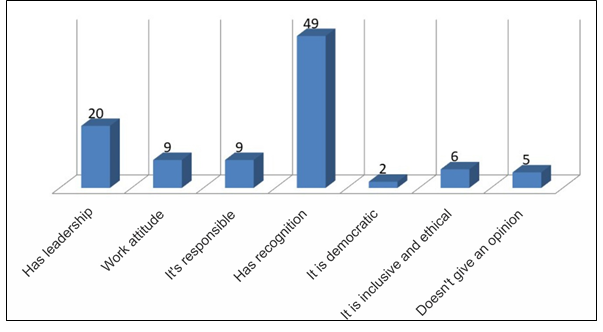

The local coordinating council, management committees, construction management committees, the status of participating agent in the participatory budgeting process, among others, are set up in the main areas of consultation between civil society and the municipal government in local public management; spaces that make the population visible on the characteristics of the performance of the municipal authority of Puno.

In the perception of the social actors, it is emphasized in two attributes of the performance of the municipal authority (Figure 4), which is expressed in that it has recognition and leadership; being less interest in the other features of the performance profile.

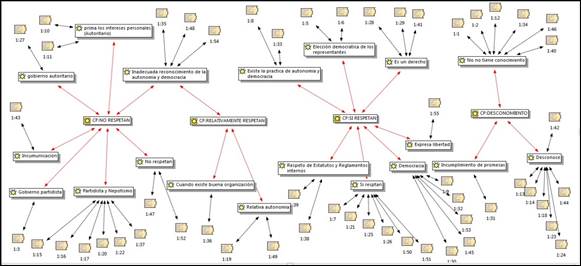

c) Respect for the autonomy and internal democracy of social organizations

The degree of respect of the municipal authority to the autonomy and internal democracy of the organizations of the civil society, in the perception of the social actors denotes contradictory tendencies: expressions or situations of full or relative respect as stipulated by the legal framework- legal; or conversely, bypassing or minimizing the autonomy and internal democracy of social organizations (Figure 5).

In effect, on the one hand, in the perception of the social actors, as a predominant trend, full respect or respect relative to the autonomy and internal democracy of their organizations, is based on the preservation of fundamental rights (especially, civil and political) and as part of the construction of democracy and the democratization of public management.

The positive perception of respect for autonomy and internal democracy is expressed in the following testimonies: “Respect for autonomy is a right of every citizen and therefore of every organization”; “It is part of democracy”; “It is clearly established in the statutes or internal regulations of social organizations”; “It is expressed in the practice of internal democracy of organizations”; “... in the democratic election of the representatives of the organization before the spaces and mechanisms of citizen participation for local management.”

On the other hand, contrary to previous perceptions, the fact that the authorities do not respect the autonomy and internal democracy of society's organizations is emphasized; situations that are expressed in: “… the authoritarian character”; “... in acting with political criteria in favor of the municipal authority”; “In the welfare attitude to control organizations”; “This situation is corroborated by the weakness of social organizations, given that managers do not enforce the autonomy of social organizations.”

Consequently, the results of the study show that the rule of law and the political will of the authorities are vital factors that influence the democratization of public investment and accountability; a situation that is consistent with various studies: the rule of law as the foundation of democracy building and accountability O'Donnell (2000), since without a constitutional rule of law the principles that underpin transparency could hardly be established and accountability Cossío (2008); the law is the product of negotiation and an instrument of power in such a way that the ruler accepts legal restrictions and enforces them only when this attitude provides him with benefits Holmes (2008). From another perspective, Villarreal (2009), maintains that citizen participation in public management is a condition for the construction of democratic governance.

Accountability, access to information and transparency

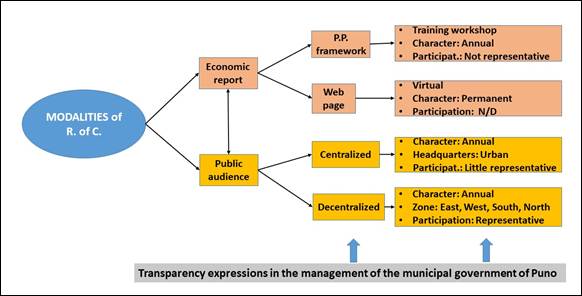

a) Accountability modalities

The Puno municipal government implements the economic report and public hearings as accountability mechanisms; which have made possible different degrees of representativeness and level of access to information, annual nature or realization at specific junctures (Figure 6).

The economic report is carried out in two specific circumstances: On the one hand, annually, directly or in person, as part of the participatory budget formulation process, especially in the training workshops for the participating agents in accordance with the provisions of the instructions of the PP. On the other hand, in the form of a secondary and permanent source, the economic report is carried out through the website or transparency portal of the Puno provincial municipality; in which the information added by direct administration or work management committee is presented.

The public hearing constitutes another form of accountability of the municipal government of Puno, which enables an institutional space for civil society to receive the municipal management report and express their opinion.

Consequently, the access to information, transparency and accountability that the local government of Puno implements, is expressed in the economic reports made annually in the participatory budget workshops, the website or transparency portal that is permanent and annual and decentralized public hearings; which have an aggregate, generic and superficial character. The results of the study agree with what Baca (2006) pointed out, in the sense that in recent years access to information and transparency in most of the country's municipal governments has improved substantially, although in a heterogeneous way; as well as with Cossío (2008), who analyzes the right to information and the consolidation of a transparency policy in Mexico as a necessary condition of the rule of law.

From an integral perspective, Merino (2008), points out that the transparency policy cannot be automatically transferred from one institution to another, nor can it be regulated without affecting previously assumed routines; that is, what is universal is the right of access to information, not the transparency policy. In the same direction, Arellano (2008), invites to incorporate the specificities of the administrative apparatus in the reflection; recovering the logic of the sociology of organizations, emphasizes the importance of endogenizing incentives and the relevance of giving an organizational sense to transparency. Gutiérrez (2004), points out that access to information and transparency of public management in Mexico, highlights the quality of democracy, both institutionally and culturally.

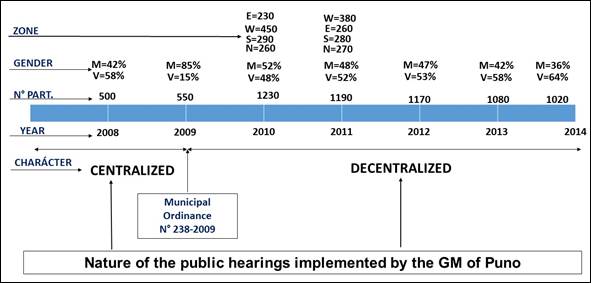

b) Public Hearings Timeline

Public hearings as an accountability mechanism implemented by the municipal authority had two modalities: centralized and decentralized (Figure 7).

In effect, on the one hand, until 2009, public hearings as a transparency mechanism implemented by the municipal authority of Puno, were centralized. From the registered information, there are the following references:

The public hearing for fiscal year 2008 was held in the first quarter of 2009. For which, previously, Municipal Ordinance N° 238-2009-CM-MPP was issued, which from that year to the present regulates public hearings. of accountability in the MPP. The accountability was carried out in the coliseum of the city of Puno; in which 500 representatives of social organizations from the four zones participated. Participants by gender denote the predominance of males (58%) over females (42%).

The 2009 public accountability hearing, which was held in an analogous manner at the Eduardo Rodríguez Ponce de León Coliseum in the city of Puno, in March 2010; In which 550 representatives of civil society organizations from the four areas of the city of Puno participated. The proportion of participants by gender denotes a predominance of men (85%) over women (15%).

On the other hand, the rendering of accounts through public hearings, since 2010 was carried out annually and on a decentralized basis (in each area of the city of Puno) having as guiding framework the Municipal Ordinance (N° 238- 2009-CM-MPP), presenting the following features:

The public accountability hearing for 2011 was held in the first quarter of 2012, in which, in global terms, 1230 representatives of social organizations from the four areas of the city of Puno participated, with the following proportions: In the eastern area, held at the civil construction site, 230 representatives participated; West area, held at the Huajsapata Neighborhood Market, 450 participants attended, in the South and North area, it was held at the premises of neighborhood organizations, which included the participation of 290 and 260 representatives of social organizations, respectively. In the proportion of participants by gender, 48% were men and 52% women.

The public hearing for 2012 was also decentralized: in the North area, it was held in the Totorani community hall, where 270 social representatives attended; in the South zone, carried out in the premises of the municipality of Salcedo small town, it had the participation of 280 representatives of social organizations; In the eastern area, it was held at the civil construction site, 260 representatives participated; In the western area, it was held at the Huajsapata Neighborhood Market, 380 participants attended.

In the public hearing in 2013, 1080 managers from social organizations participated, with a predominance of men (58%).

In the public hearing for the financial year 2014, 1,020 managers participated, increasing the predominance of males (64%) over female managers.

While the accountability process implemented by Mayor Iván Flores (2015-2018), basically, meant the continuity of public hearings initiated in the preceding period or through economic management reports:

In the financial years of 2016 and 2017, the public accountability hearings were decentralized;

In the financial years of 2015 and 2018, only economic management reports were made.

In general, throughout 2015-2018, access to information, transparency and accountability was aggregate, partial, segmented and unrepresentative.

Consequently, in the municipal government of Puno, the decentralization of public hearings carried out since 2010 as a fundamental form of accountability, however, its aggregate, partial and segmented nature; The participation mechanism improved, as it increased not only the number of participating agents, but also allowed direct access to information, transparency and social control of the management of the municipal government of Puno.

c) Dynamics and centers of interest in public accountability hearings

The accountability that the municipal authority of Puno implemented from the 2010 exercise was through public hearings (carried out in the first months of the following year), in the areas (East, West, North and South) of the city; whose dynamics had the following structure: Registration of participating agents in the area; welcome to municipal authorities; video projection illustrating works executed in the area; Mayor's report (works carried out during the financial year, projects to be carried out in the following financial year, projects considered strategic supported by before and after photos, report of works carried out by the administration of the management committee); interpellation of civil society, expressed through two wheels of questions and the subsequent response by the municipal authority; closure of public hearing.

In the perception of the social actors participating in the public hearings, its emphasis is generally denoted in the recognition of the municipal authority, compliance with the executed projects, observation of the works management committees and presentation of new demands and needs.

The recognition of the municipal authority is given by decentralized audiences, which not only enables a greater degree of participation, but the report is more pragmatic, since the projects carried out during the year are evidenced by the testimonies of the population and the illustrations (video and photos) presented at the accountability.

Conformity with the projects or works carried out in the different areas is given while the perception of the social actors indicates that these needs were very felt and demanded by the population and that they were even presented to the previous authorities, without any response.

The observations to the works management committees, essentially, were related to the difficulties encountered in the quality and durability of the works, as well as on the management in the execution of the works, in which certain doses of bureaucratism, welfare is pointed out and authoritarianism.

Public hearings are also configured as a space for the presentation of new demands from the population of the areas of the city of Puno, consisting of road infrastructure (asphalting, improvement or maintenance of tracks, sidewalks), social and neighborhood sports infrastructure (sports fields , platforms, multipurpose rooms), educational infrastructure for educational institutions of initial and primary level, basic and environmental sanitation (water, sewage, electrification and green areas), among the most important.

d) Access to information and transparency: The reports of public hearings

In the framework of access to information and transparency, the reports made by the municipal authority during public accountability hearings include the following aspects: legislative work, budget report, prioritized projects, consolidated expenses and investments.

The report of the legislative work carried out in the public hearings, considers the municipal ordinances and municipal council agreements:

The municipal ordinances approved in the 2011-2014 term, in global terms, reach 30 ordinances each year; while in the 2015-2018 term, 109 ordinances were issued, being higher in 2016 (31 OM) and 2018 (33 OM). In municipal council agreements, greater dynamism is denoted in both municipal efforts.

The municipal ordinances were published in the official newspaper El Peruano; while the municipal council agreements and mayoral decrees in the municipal cartel and electronic portal; although several of the latter were not disseminated according to the observations presented by the Comptroller General of the Republic.

The budget report made at public hearings, within the categories of initial opening budget and budget execution. In this regard, in the financial years of 2011 - 2018, the following specific figures are available (Table 1):

Table 1 Consolidated report by PIA and budget execution by the municipal government of Puno: period 2011 - 2018

| MUNICIPAL MANAGEMENT | FISCAL YEAR | OPENING INSTITUTIONAL BUDGET (PIA) | BUDGET EXECUTION |

| 2011 to 2014 | 2011 | 35 195 660 | 61 411 805 |

| 2012* | 8 626 000 | 18 517 626 | |

| 2013* | 8 626 000 | 16 510 086 | |

| 2014* | 8 626 000 | 7 400 000 | |

| 2015 to 2018 | 2015 | 47 799 272 | 82 720 751 |

| 2016 | 46 120 915 | 103 922 530 | |

| 2017 | 51 406 777 | 100 696 675 | |

| 2018 | 51 519 982 | 93 498 870 |

Source: Public Hearings Report- MPP, Puno, 2014 and 2018

(*) Only consider capital expenditure budget

In general terms, in the financial years considered (2011-2018), the execution budget is greater than the initial opening budget (PIA); This is because the municipal authorities of both administrations, after having approved the PIA at the beginning of the fiscal year, carry out procedures with the central government to obtain a budget increase.

Within the initial opening budget, which has a referential character that is formulated at the beginning of each year; in the financial year of 2011 it has a greater magnitude compared to the other years considered in the administration of the mayor Luis Butrón Castillo. While the budgetary execution of the municipal government of Puno in the 2014-2018 period, presents an increasing trend; situation that clearly denotes a relative effectiveness of the management capacity of municipal authorities to capture resources from the central government.

Accountability on prioritized projects and budget investment

From the report that the municipal authorities made in the public hearings on the execution of the prioritized projects, during the management of Luis Butrón Castillo (2011 - 2014) and the management of the mayor Iván Flores Quispe (2015-2018), which considers the number of projects and the budget executed by financial year denotes the following trends (Table 2).

In general terms, regarding the number of prioritized projects, there is a growing decreasing trend in the financial years 2011 and 2014; a situation that is relatively consistent with the magnitude of the budget execution, on what was executed in the financial year. In the period 2015-2018, there is a cyclical trend (it is significantly reduced in the financial years of 2016 and 2018; while it increases in the year 2015 and 2017.

On the other hand, in relation to the proportion of prioritized projects and the magnitude of the budget executed in each of the financial years considered; from the accountability report made by the municipal authority, it is denoted that there is agreement between the number of prioritized projects and the amount of budget execution.

Table 2 Report on the prioritization of projects and budget investment in the municipal government of Puno: period 2011 -2018

| MUNICIPAL PERIOD | FISCAL YEAR | PRIORITIZED PROJECTS (N°) | BUDGET (S/) |

| 2011 to 2014 | 2011 | 58 | 29 991 947 |

| 2012 | 59 | 18 517 626 | |

| 2013 | 44 | 17 416 694 | |

| 2014 | 35 | 7 400 000 | |

| 2015 to 2018 | 2015 | 93 | 36 872 397 |

| 2016 | 47 | 22 089 702 | |

| 2017 | 100 | 36 872 397 | |

| 2018 | 31 | 34 840 359 |

Source: Annual memory report, provincial municipality of Puno, 2014 and 2018

Consequently, on the accountability and democratization of public investment in the municipal government of Puno; the results show that its scope, expressed in terms of effects and impacts, are still initial, limited and even embryonic; highlighting fears about the real political will of local authorities and the limited interest, weakness of civil society organizations and ignorance of the juridic-legal framework.

These results are corroborated with the studies carried out by: Mashaw (2008) that emphasizes the objectives and actors involved in the accountability process; López & Hincapié (2014) emphasize the quality of democracy; Franciskovic (2013) in a challenge by establishing itself as an effective means of surveillance and sanction between society and government, through which public officials must respond, explain and justify their actions, subject to an ethical legal order and compliance with objectives. Cabrera & Villalobos (2012) point out that accountability should be a practice that favors the use as an input of social control by citizens and of evaluation by the state apparatus itself, with the consequent benefits for social democracy, efficiency and effectiveness of the State.

CONCLUSIONS

Building a solid rule of law, transparent government and an effective accountability system are the fundamental pillars of a democratic regime; in which framework, accountability as a strategy for democratizing local public management is conditioned by the political will of municipal authorities and officials and the institutionalization of participatory spaces and mechanisms for access to information and transparency.

Accountability in the municipal government of Puno denotes a partial nature, of an aggregate nature and not very representative; situation that is expressed in the annual public hearings in whose dynamics the considered aspects emphasize the legislative work, the budget report, the projects prioritized by zones and the consolidated report of expenses and investments, which had a very aggregate character. The limited representation is expressed in that the participants in the public hearings were the directors of the construction management committees, the users of the prioritized projects and sympathizers of the political organization of the municipal authority.

Public hearings are configured in the main accountability mechanism implemented by the Puno municipal authority; which in recent years had a decentralized character and made it possible to express the level of recognition or limited legitimacy of municipal authority and management, the claiming or proposing attitude of the managers of social organizations, as well as a space for the presentation of new demands and initiatives.

REFERENCIAS BIBLIOGRÁFICAS

Ackerman, J. (2008). Más allá del acceso a información: transparencia, rendición de cuentas y Estado de Derecho. México: Siglo XXI editores. [ Links ]

Arellano, D. (2008). Transparencia y organizaciones gubernamentales. En Más allá del acceso a la información. Transparencia, rendición de cuentas y estado de derecho. Mexico: Siglo XXI editores. [ Links ]

Baca, E. (2006). Situación y Perspectivas de la Vigilancia Ciudadana y Rendición de Cuentas en el Perú, en el marco de la descentralización y el Presupuesto Participativo. En Recuperado de: http://www.mesadeconcertacion.org.pe/documentos/documentos/doc_00464.pdf. Siglo XXI editores. [ Links ]

Bolaños, J. (2010). Bases conceptuales de la rendición de cuentas y el rol de las entidades de fiscalización superior. Revista Nacional de administración, 1(1), 109-139. https://doi.org/10.22458/rna.v1i1.288 [ Links ]

Cabrera, L. C., & Villalobos, J. V. (2012). El derecho a la rendición de cuenta en Venezuela. Período: 1999-2012. VI Jornadas Nacionales de Investigación de la URBE. Recuperado de http://virtual.urbe.edu/eventostexto/JNI/URB-166.pdf [ Links ]

Cardona, S. (2012). Las veedurías ciudadanas en cuanto mediaciones/mediadores de las relaciones Estado-sociedad en el ámbito local. Administración & Desarrollo, 40(55), 19-32. Recuperado de https://dialnet.unirioja.es/servlet/articulo?codigo=4088449 [ Links ]

Cossío, J. R. (2008). Transparencia y estado de derecho. Ackerman, John M ., coord. Más allá del acceso a la información. Transparencia, rendición de cuentas y estado de derecho. México: UNAM, 100-118. [ Links ]

Cunill Grau. Nuria. (2007). La rendición de cuentas y el control social. Una aproximación conceptual. Seminario internacional. Candados y derechos: Protección de programas sociales y construcción de ciudadanía. [ Links ]

Emmerich, G. E . ( 2004 ). Transparencia, rendición de cuentas, responsabilidad gubernamental y participación ciudadana. Polis: Investigación y Análisis Sociopolítico y Psicosocial, 2(4), 67-90. Recuperado de http://www.redalyc.org/articulo.oa?id=72620404 [ Links ]

Fox, J. (2008). Transparencia y rendición de cuentas. Más allá del acceso a la información. Transparencia, rendición de cuentas y estado de derecho, 174-198. [ Links ]

Franciskovic, J. (2013). Retos de la gestión pública: presupuesto por resultados y rendición de cuentas. Journal of Economics Finance and Administrative Science, 18, 28-32. [ Links ]

Goldfrank, B. (2006). Los procesos de" presupuesto participativo" en América Latina: éxito, fracaso y cambio. Revista de ciencia política (Santiago), 26(2), 3-28. https://doi.org/10.4067/S0718-090X2006000200001 [ Links ]

Gutiérrez, R. (2004). Acceso a la información y transparencia de la gestión pública. Sus efectos en el proceso de consolidación democrática. Sociológica, 19(56), 87-109. [ Links ]

Hernández, A. (2009). Hacia un concepto ético de" rendición de cuentas" en las organizaciones civiles. En-claves del pensamiento, 3(5), 47-70. Recuperado de http://ref.scielo.org/2d6bt4 [ Links ]

Holmes, S. (2008). Linajes del Estado de derecho. Más allá del acceso a la información. Transparencia, rendición de cuentas y Estado de derecho. México, Instituto de Investigaciones Jurídicas de la Universidad Nacional Autónoma de México/Siglo XXI Editores/Universidad de Guadalajara/Cámara de Diputados. [ Links ]

Jiménez, M. C. (2012). La importancia del accountability social para la consolidación de la democracia en América Latina. En Revista Relaciones Internacionales, Estrategia y Seguridad (Vol. 7). https://doi.org/10.18359/ries.84 [ Links ]

López, J. A., & Hincapié, S. (2014). La rendición social de cuentas en la calidad de la democracia. Una discusión sobre aportes y retos de la política comparada. Reflexión política, 16(31), 1-12. [ Links ]

Mashaw, J. L. (2008). Rendición de cuentas, diseño institucional y la gramática de la gobernabilidad. Ackerman, John M ., coord. Más allá del acceso a la información. Transparencia, rendición de cuentas y estado de derecho. México: UNAM , 119-173. [ Links ]

Melossi, D. (1992). El Estado del Control Social: un estudio sociológico de los conceptos de estado y control social en la conformación de la democracia. Siglo XXI. [ Links ]

Merino, M. (2008). La transparencia como política pública. Ackerman, John M ., coord. Más allá del acceso a la información. Transparencia, rendición de cuentas y estado de derecho. México: UNAM , 240-262. [ Links ]

Montecinos, E. (2014). Diseño institucional y participación ciudadana en los presupuestos participativos: los casos de Chile, Argentina, Perú, República Dominicana y Uruguay. Política y gobierno, 21(2), 351-378. [ Links ]

Naessens, H. (2010). Ética pública y transparencia. Encuentro de Latinoamericanistas Españoles : congreso internacional, 2113-2130. Recuperado de https://halshs.archives-ouvertes.fr/halshs-00531532 [ Links ]

O’Donnell, G. (2000). Further thoughts on horizontal accountability. Seminário: Institutions, Accountability and Democratic Governance in Latin American .” Notre Dame: Kellogg Institute for International Studies/University of Notre Dame. Notre Dame. [ Links ]

Pastor, E. (2004). La participación ciudadana en el ámbito local, eje transversal del trabajo social comunitario. Alternativas. Cuadernos de Trabajo Social , N. 12 (diciembre 2004 ); pp. 103-137. [ Links ]

Peruzzotti, E. (2007). Rendición de cuentas, participación ciudadana y agencias de control en América Latina. XVII Asamblea General Ordinaria OLACEFS, Santo Domingo. [ Links ]

Peruzzotti, E., & Smulovitz, C. (2002). Accountability social: la otra cara del control. Controlando la política. Ciudadanos y medios en las nuevas democracias latinoamericanas, 23-53. [ Links ]

Rocchi, G., & Venticinque, V. (2010). Calidad democrática, ciudadanía y participación en el ámbito local. Espacio Abierto: cuaderno venezolano de sociología, 19(4), 601-620. Recuperado de https://dialnet.unirioja.es/servlet/articulo?codigo=3399816 [ Links ]

Tumi, J. (2015). Espacios y mecanismos de participación ciudadana en la democratización de la gestión del gobierno local de Puno-Perú. Revista Cuestiones de Sociología: Investigación En Ciencia Y Desarrollo, 4(1), 43-66. Recuperado de http://revistas.unap.edu.pe/csociologia/index.php/csociologia/article/view/60 [ Links ]

Valverde, K., Gutiérrez, E., & García, F. de M. (2013). Presupuesto público sin participación ciudadana: La necesidad de un cambio institucional en México para la consolidación democrática. Revista mexicana de ciencias políticas y sociales, 58(218), 105-128. https://doi.org/10.1016/S0185-1918(13)72291-8 [ Links ]

Villarreal, M. T. (2009). Participación y gestión pública en Nuevo León, México. Revista Enfoques, 7(11), 417-439. Recuperado de https://www.redalyc.org/articulo.oa?id=96011647013 [ Links ]

Received: May 22, 2019; Accepted: February 05, 2020

Este es un artículo publicado en acceso abierto bajo una licencia Creative Commons

Este es un artículo publicado en acceso abierto bajo una licencia Creative Commons