Serviços Personalizados

Journal

Artigo

texto em

texto em  Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Enviar este artigo por email

Enviar este artigo por emailIndicadores

-

Citado por SciELO

Citado por SciELO

Links relacionados

-

Similares em

SciELO

Similares em

SciELO

Compartilhar

Permalink

PermalinkIndustrial Data

versão impressa ISSN 1560-9146versão On-line ISSN 1810-9993

Ind. data vol.26 no.1 Lima jan./jun. 2023

http://dx.doi.org/10.15381/idata.v26i1.24162

Production and Management

Streamlining of Processes and Its Impact on the Issuance Time of the Dean’s Resolution for Approval of Externally Financed Projects in a Public University

1 Public accountant. Currently working as project manager at Vicerrectorado de Investigación y Posgrado of Universidad Nacional Mayor de San Marcos (Lima, Perú). E-mail: ccruzc@unmsm.edu.pe

This paper addresses the question “How does the streamlining of processes based on the analysis of activities and staff awareness-raising impact the issuance times of the Dean’s Resolution of an agreement and/or contract in a public university?” A system was implemented to streamline processes in the issuance times of the Dean’s Resolution for approval of externally sponsored projects. Database review was used as the data collection technique. The data were processes by means of the RStudio interface. A significant reduction in the time required to issue the Dean’s Resolution for the approval of an agreement and/or contract was obtained as the final result.

Keywords: streamlining of processes; Dean’s Resolution; agreement and/or contract; externally financed projects; staff awareness-raising.

INTRODUCTION

The university under study is a public institution devoted to research conducted by its researchers, graduate students, and undergraduate students. It receives financing from sources such as ProInnóvate Perú, Prociencia-World Bank-Concytec, among others, which are administered by the Vicerrectorado de Investigación y Posgrado [Vice Dean’s Office of Research and Graduate Studies] (VRIP). There were 38 projects under execution at the time of the research; it was found that there were major problems with the administrative staff of the areas involved with said projects, as well as procedures that did not allow for the timely issuance of the Dean’s Resolution (RR) of an agreement and/or contract, preventing the financial execution of the aforementioned projects from starting. This resulted in non-compliance with documents required by the financing sources, as well as in reprimands to the university, often resulting in the refund of the funds awarded to the winning project and those that were in the process of execution, creating a bad precedent for the institution.

Consequently, the problem addressed in this research was “how does the streamlining of processes based on the analysis of activities and staff awareness-raising impact on the issuance times of the Dean’s Resolution of an agreement and/or contract in a public university?”

The objective was to determine the impact of the streamlining of processes based on the analysis of activities and staff awareness-raising on the issuance times of the Dean’s Resolution of an agreement and/or contract in a public university.

The hypothesis was as follows: The streamlining of processes based on the analysis of activities and staff awareness-raising reduces the issuance times of the Dean’s Resolution of an agreement and/or contract in a public university.

This research study is relevant because it introduces an alternative for improving processes, both for internal and external users, aimed at facilitating the early financial execution of projects, enabling researchers to obtain favorable results from funding sources. Such improvement alternative may also be applied to other institutions of similar characteristics, while taking into account the specific features of their environment.

Background

Research by Núñez (2005) focuses on the poor management of approximately 300 projects, roughly equivalent to US$ 26 million, which has a strong impact on the productivity indicators of the systems and organization division of the bank under study. As a solution to this problem, the researcher proposes and designs a Project Management Office to manage the above-mentioned portfolio, fulfilling the functions, roles, and responsibilities in such a way that it can lead the organization’s sales and services.

Another important antecedent is that of the Pontificia Universidad Católica del Perú (PUCP, 2016) where the team of project managers, the Project Management Office and the Operating Manual for Project Management are internationally recognized, because they enable researchers to achieve the goals set with the funding source by providing them with the best tools.

Lastly, Ramírez (2008) states that project management in an organization is underestimated, and that there is no open communication between the different areas. Therefore, to improve project management, he proposes the involvement of the entire organization areas in planning and control.

Quality Management

According to Gryna et al. (2007), service quality is important for customer satisfaction. They distinguish between two types of customers: external customers (actual and potential) and internal customers (who receive information from all areas of the organization). Both are referred to as “interested participants”, as the goal of any service provided is to obtain some benefit, i.e., the external customer, the internal customer, and the organization benefit from it.

Quality management is thus understood as an impulse to start a new stage in the service provided by the organization, using its potential to provide a better service to its stakeholders in the area in which the organization operates. The organization must at all times be mindful of its external and internal customers, as early on as from the design of the service.

Miranda et al. (2007) identify four major approaches that should be applied within a company: inspection, quality control, quality assurance, and total quality maangement. Each of these may be applied to companies and public universities-such as the one under study-through processes, to achieve better quality management and efectiveness in meeting stakeholder objectives.

Pérez (1994) provides a number of steps to be followed in quality management, emphasizing the commitment of Management, involving the commitment of all managers to the improvement processes. Failure to do so would result in a lack of support and collaboration from the staff involved, delaying the adoption of any measures proposed within the institutions. The cost of poor quality must also be taken into account, as it leads to cumbersome processes and a total lack of motivation for any improvement process.

It should be noted that Pérez (1994) places special emphasis on the step mentioned above for the improvement of processes within quality management; the commitment to achieve quality improvement in any organization rests with senior management and employees.

PDCA Cycle

According to Zapata (2015), the PDCA cycle is based on four key stages: plan, do, check and act; that is, once the act stage is completed, the planning stage is resumed. This cycle is an essential tool within organizations, as it allows better achievement of quality results and competitiveness in processes, products, and services. It starts from the planning of actions to be executed by competent staff to address non-value adding activities.

Therefore, this cycle can be introduced into the organziation, as planning is an essential factor that will allow compentent staff to make decisions and, thus, obtain quality results in the processes of the organization. The PDCA cycle is continuous, because it returns to the planning stage once the acting stage is completed and the cycle begins again. It uses the feedback from the previous cycle as the new starting point; therefore, it can be compared to a wheel turning on an uphill slope.

Pérez and Múnera (2007) complement Zapata (2015) and state that the PDCA cycle is dynamic for the processes of an organization and allows for continuous improvement.

Funding Sources

According to Millones (2016), the Peruvian government allocates millions of soles (PEN) in competitive funds for research through the National Council for Science, Technology and Technological Innovation (Concytec, for its Spanish acronym). Public universities must adapt their statuses and regulations to the new University Law in order to obtain such funding, which entails changes in human resources, infrastructure and research activities. Institutions that do not meet the set requirements, such as infrastructure and equipment, are not eligible for funding.

At the time of writing this paper, the agency in charge of awarding Concytec’s competitive funds was the National Program for Scientific Research and Advanced Studies (Prociencia, for is Spanish acronym), which launches several calls for projects with external funding for which researchers apply in compliance with the set requirements. Funding is awarded for periods of 12 to 36 months of execution.

Research Projects

According to UNMSM (2016), research projects aim to contribute and transform scientific knowledge that foster the development and benefit of society; such projects aim to be recognized nationally and internationally through the publication of papers in indexed journals, theses, among others, to allow for research based on theoretical and quality contributions and experiences.

Research projects are intended to contribute to an academic level of high performance and impact on society. Research should reach the entire student community via papers, books or theses, to continue further knowledge, always striving for quality to differentiate itself from other institutions.

Executing Body

The Ministerio de Economía y Finanzas - MEF (n.d.) explains that the executing body is directly responsible for the execution and administration of funds, regarding revenues and expenditures, in accordance with the regulations and procedures of the National Treasury System. According to Innóvate Perú (2014), the executing body is responsible for the management, administration and financial execution and closure of the project.

Both institutions agree that the executing body is responsible for the management, administration and execution of the funds, revenues, and expenditures, under the regulations and procedures of the National Treasury System. Failure to execute the funds would affect the executing body and would results in possible reprimands, as well as restrictions on the execution of the funds, which would result in non-compliance.

Financial Management of Projects

Fabrés (2010) states that financial management of projects consists of determining the economic and human resources required to execute a project; in addition, operating costs including monitoring and control of revenues and expenses must be calculated as the proejct is executed, to detect possible deviations and make decisions that do not affect and/or damage the financial execution of such projects.

The author emphazises the importance of financial management, especially of operating costs for the monitoring and control of revenues and the value of the people who will execute and control the execution of the project, as is done in this research study.

Execution of Public Expenditure

According to Universidad Nacional Mayor de San Marcos - UNMSM (2018), the execution of public expenditure involves the collection and inflow of resources, and it used within the tax period. On the other hand, for Ministerio de Economía y Finanzas - MEF (n.d.), it is a process aimed at meeting all expenditure obligations to finance goods and services to achieve the expected results according to the authorized budget appropriations through the institutional budgets, taking into account the Programming of Annual Commitments (PCA, for its Spanish acronym), based on the principle of legality and budget balance, and all the regulations and principles of each public entity.

The purpose of both institutions is to manage resources through financial execution within the tax year, in accordance with the regulations in force in each institution. Also, both aim to obtain the expected results, as is the case of the projects where the budgetary resources are executed within the specified period and comply with the regulation of the executing and funding body.

METHODOLOGY

Experimental research was used for this study. According to Hernández et al. (2014), independent variables (presumed causes) are intentionally manipulated in this type of study to analyze the consequences on one or more dependent variables (presumed effects), namely, the research subjects.

Based on Sánchez and Reyes (2009), this research study follows a time-series and quasi-experimental design, because the sample data were collected in different time periods as part of a pretest and posttest stage, following the scheme shown below:

O1 O2 O3 X O4 O5 O6

O: Observation or result of the dependent variable

X: Application of the independent variable

The unit of analysis consisted of the dossiers of externally funded projects (Fondecyt and Innóvate Perú), which included the fields of applied research, basic research, scientific equipment and PhD programs.

The population consisted of all externally funded projects, and its size was infinite due to their nature. On the other hand, the sample size consisted of 11 externally funded projects from 2017, 2018 and 2019.

Database review was used as the data collection technique, using the document management system (DMS) implemented by the university under study. The data were processed in R language via the RStudio interface. The script used is presented below:

#Leo los datos

> data=read.table("clipboard",header=T)

> attach(data)

#Hacemos el análisis descriptivo

> library(MVN)

Warning message:

package ‘MVN’ was built under R version 4.1.1

> mvn(data)

$multivariateNormality

Test HZ p value MVN

1 Henze-Zirkler 0.5700759 0.08723356 YES

$univariateNormality

Test Variable Statistic p value Normality

1 Anderson-Darling pre 0.4570 0.2127 YES

2 Anderson-Darling post 0.6451 0.0672 YES

$Descriptives

n Mean Std.Dev Median Min Max 25th 75th Skew

pre 11 42.18182 10.215852 46 21 55 35 49 −0.5768621

post 11 17.27273 5.968097 16 11 27 12 22 0.3384319

Kurtosis

pre −0.8783542

post −1.6787233

> boxplot(pre,post)

#Pruebo si hay igualdad de varianzas

> var.test(pre,post)

F test to compare two variances

data: pre and post

F = 2.9301, num df = 10, denom df = 10, p-value = 0.1049

alternative hypothesis: true ratio of variances is not equal to 1

95 percent confidence interval:

0.7883321 10.8904468

sample estimates:

ratio of variances

2.930066

#Pruebo la hipótesis

> t.test(pre,post,alternative="greater",var.equal=T)

Two Sample t-test

data: pre and post

t = 6.9826, df = 20, p-value = 4.456e-07

alternative hypothesis: true difference in means is greater than 0

95 percent confidence interval:

18.75651 Inf

sample estimates:

mean of x mean of y

42.18182 17.27273

RESULTS

Descriptive Analysis

The data collected in the pretest and posttest are shown in Table 1 (days).

Table 1 Data Collected.

| Pretest | Posttest |

|---|---|

| 49 | 12 |

| 35 | 16 |

| 34 | 12 |

| 55 | 25 |

| 49 | 12 |

| 52 | 23 |

| 21 | 27 |

| 35 | 19 |

| 46 | 11 |

| 49 | 21 |

| 39 | 12 |

Source: Prepared by the author.

The corresponding descriptive statistics are shown in Table 2.

Table 2 Descriptive Statistics of RR Issuance Times.

| Statistic | Pretest | Posttest |

|---|---|---|

| Mean | 42.1818182 | 17.2727273 |

| Median | 46 | 16 |

| Standard deviation | 10.2158522 | 5.968097 |

| Coefficient of variation | 0.2421862 | 0.3455214 |

| Kurtosis | −0.88 | −1.68 |

| Skewness | −0.57 | 0.33 |

| 1st quartile | 35 | 12 |

| 3rd quartile | 49 | 22 |

Source: Prepared by the author.

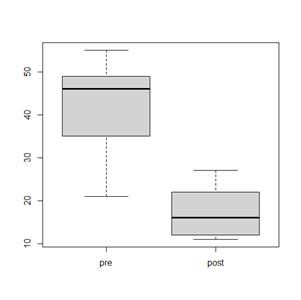

Figure 1 shows the box-and-whisker plot of values obtained in the pretest and posttest.

As shown in Table 2, there is a significant difference between the means and medians of the pretest and posttest moments. This result is further supported in Figure 1, where it is observed that the box and whiskers corresponding to the posttest are significant lower than those if the pretest.

Data normality was analyzed using the Shapiro Wilk test, yielding the following results:

H0: Data follow a normal distribution.

H1: Data do not follow a normal distribution.

α: 0.05

Shapiro-Wilk for pretest

W = 0.91345, p-value = 0.2678

Shapiro-Wilk for posttest

W = 0.86316, p-value = 0.06326

The null (H0) hypothesis is accepted in both cases, indicating that the data follow a normal distribution; therefore, the data are parametric.

Inferential Analysis

It was found in the previous section that the data are parametric; therefore, the hypothesis test used was the Student’s t-test, applied to non-related samples, for which the equality or inequality of variances were tested using the F test. The statistical hypothesis pertaining to the test of variances, as well as the results, are detailed below.

H0: Variances are equal

H1: Variances are not equal

α: 0.05

The results were as follows:

F test to compare two variances

F = 2.9301, num df = 10, denom df = 10, p-value = 0.1049

alternative hypothesis: true ratio of variances is not equal to 1

95 percent confidence interval:

0.7883321 10.8904468

The p-value is greater than the type I error probability α. The null hypothesis (H0) is accepted; therefore, variances are equal.

The following is the contrast of hypotheses performed using Student’s t-test for equal variances, for which the statistical hypotheses are stated.

H0: u1= u2

H1: u1> u2

α: 0.05

The results of the test were as follows:

Two Sample t-test

data: pre and post

t = 6.9826, df = 20, p-value = 4.456e-07

alternative hypothesis: true difference in means is greater than 0

95 percent confidence interval:

18.75651 Inf

sample estimates:

mean of x mean of y

42.18182 17.27273

Similar to the previous case, the p-value is lower than the type I error probability α; therefore, the null hypothesis (H0) is rejected and the alternative hypothesis (H1) is accepted. Hence, it can be stated that there is evidence in favor of the result obtained in the posttest being lower than that of the pretest, that is, a significant reduction in time as a result of the implementation of the independent variable or stimulus.

Method Applied

Initially, during the pretest, for the issuance of the Dean’s Resolution (RR) of an agreement and/or contract, the funding organization submitted it (or them) duly signed by both parties to the submissions desk of the Vice Dean’s Office of Research and Graduate Studies (VRIP). Subsequently, the agreement and/or contract passed along to the Secretariat and were sent to the Vice Dean’s Office through an internal route for the respective signature. Once signed, the document(s) would return by the same route and be sent to the Dirección de Prospectiva y Gestión de la Investigación y Posgrado [Directorate of Prospective and Management of Research and Graduate Studies] (DPGIP), which would issue the document requesting the issuance of the RR for the wining project and the signature of the Vice Dean. On average, the waiting time for the document to be returned was three (3) days; thereafter, the corresponding area was in charge of managing the document and the RR was issued after an average of 42 days.

Based on the above, the delay in the issuance of the RR led to discomfort on the part of researchers and a series of delays regarding the execution of the project and the submission of deliverables to the funding source within the established deadlines. As a result, a number of meetings were held with the Dean, as well as meetings with the main actors involved in the issuance of Dean’s Resolutions. It was agreed that all documentation related to the externally funded projects had to be stamped VERY URGENT EXTERNAL PROJECTS. Thus, it was possible to reduce many steps from the VRIP. All agreements and/or contracts are forwarded directly to the DPGIP for the drafting of the documents, which are signed by the Vice Dean and processed by the corresponding areas within one day. This practice makes it possible to obtain the RRs in an average of 17 days, thus achieving good results in the execution of the project and the submission of deliverables to the funding sources as part as the posttest.

DISCUSSION

Delays in the issuance of Dean’s Resolutions of agreements and/or contracts for the financial execution of expenditure were due to the lack of knowledge, interest and commitment of the staff to address this type of request; therefore, they repeatedly set it aside. Unfortunately, the lack of knowledge of how to work with this type of contract and the lack of motivation of the staff involved led to a lack of urgency and, as a result, the files remained unattended for up to four months in the same area.

In response to this situation, the DPGIP prepared a model Dean’s Resolution proposal that approves the agreement and/or contract to expedite the process, and coordinated directly with the heads responsible for each area and with the personnel involved. In order to maintain a results-based approach, the head of the DPGIP decided to provide non-monetary incentives to the staff to acknowledge their efforts, dedications and commitment to the requests. In addition, it was decided to stamp Dean’s Resolution requests VERY URGENT in order to differentiate them from other requests from the university under study; therefore, reducing the time required for the researcher to comply with the indicators of the funding sources.

This research study shares similarities with Ramírez (2008) and Núñez (2005). At first, the staff of the areas involved understimated the projects with external financing, there was a lack of communication and ignorance of the serious problems in the management of projects. Consequently, the university was not well regarded as executing body by the funding sources, to the detriment of the researchers of the aforementioned academic institution.

Unlike the study conducted by the PUCP (2016), in the pretest stage of this research, the university under study did not have a specific project management area or staff to act as project managers to accompany researchers. This situation was subsequently remedied and validated in the posttest, in which the mentioned results were obtained.

CONCLUSIONS

The implementation and streamlining of all the processes and procedures based on the analysis of the activities, as well as the staff awareness-raising was of utmost importance for this research, since they reduced the time required to issue the Dean’s Resolution of the agreement and/or contract for the winning projects conducted by researchers of the university under study.

To meet the expected indicators, the human component, which plays a key role in them, served as a starting point.

The streamlining of processes and procedures, based on the analysis of the activities and staff awareness-raising, improved the level of compliance with the financial execution of the wining externally financed projects.

For this research to be applied in any university, the commitment of senior management is essential to achieve the expected results.

In the context of improvement achievements, the establishment of clear, measurable, and contrasted indicators is a priority.

REFERENCIAS

Fabrés, G. (3-5 de marzo de 2010). Gestión Económica de los Proyectos para ONG. Jornadas "Capacitando a las ONG/sida: Mejorando la prevención del VIH", Barcelona, España. http://www.sidastudi.org/resources/doc/100315-gestion-economica-de-proyectos-7126676484247006498.pdf [ Links ]

Gryna, F. M., Chua , R. C. H., DeFeo , J. A., y Pantoja Magaña, J. (2007). Método Juran Análisis y planeación de la calidad. México D. F., México: McGraw Hill. [ Links ]

Hernández Sampieri, R., Fernández Collado, C., y Baptista Lucio, P. (2014). Metodología de la Investigación. México D. F., México: McGraw Hill. [ Links ]

Innóvate Perú. (2014). Manual Operativo de Proyectos con Fondos Externos. Lima: InnóvatePerú. https://www.mef.gob.pe/contenidos/archivos-descarga/Manual_Operativo_del_Proyecto_Invierte.pdf [ Links ]

Millones Gómez, P. A. (2016). Investigación en provincias: Dificultades y Retos. Revista Cientítica Salud & Vida Sipanense, 3(2). [ Links ]

Ministerio de Economía y Finanzas. (S.F). Definiciones. https://www.mef.gob.pe/es/?option=com_content&language=es-ES&Itemid=100770&view=article&catid=27&id=375&lang=es-ES [ Links ]

Miranda González, F. J., Chamorro Mera, A., y Rubio Lacoba, S. (2007). Introducción a la Gestión de la Calidad. Madrid, España: Delta Publicaciones. [ Links ]

Núñez Fernández, A. D. (2005). Importancia de una oficina de gestión de proyectos en una institución bancaria en el Perú. (Tesis de maestría). Universidad Nacional Mayor de San Marcos, Lima. [ Links ]

Pérez Fdez. de Velasco, J. A. (1994). Gestión de la Calidad Empresarial. Calidad en los servicios y atención al cliente. Calidad total. Madrid, España: ESIC Editorial. [ Links ]

Pérez Villa, P. E., y Múnera Vásquez, F. N. (2007). Reflexiones para implentar un sistema de gestión de la calidad (ISO 9001:2000) en cooperativas y empresas de economía solidaria (Documento de trabajo). Bogotá, Colombia: Universiad Cooperativa de Colombia. [ Links ]

Pontificia Universidad Católica del Perú. (2016). Manual operativo para la gestión de proyectos de investigación. https://textos.pucp.edu.pe/pdf/4714.pdf [ Links ]

Ramírez, L. (2008). Aplicación de la metodología de la cadena crítica y la teoría de las restricciones en la planificación del departamentos de investigación y desarrollo de una compañia de desarrollo técnológico. Venezuela. [ Links ]

Sánchez Carlessi, H., y Reyes Meza, C. (2009). Metodología y Diseños en la Investigación Científica. Lima, Perú: Visión Universitaria. [ Links ]

UNMSM. (2018). Clasificador de ingresos. https://ogpl.unmsm.edu.pe/resources/Normas/Institucional/ClasificadorIngresos2018.pdf [ Links ]

UNMSM. (2016). Estatuto de la UNMSM. Perú: Fondo Editorial UNMSM. https://campusindustrial.unmsm.edu.pe/industrialito/Files/estatuto-unmsm-ANEXO_RR_03013-R-16.pdf [ Links ]

Zapata Gómez, A. (2015). Ciclo de la Calidad PHVA. Bogotá, Colombia: Universidad Nacional de Colombia. [ Links ]

Received: October 04, 2022; Accepted: December 13, 2022

Este es un artículo publicado en acceso abierto bajo una licencia Creative Commons

Este es un artículo publicado en acceso abierto bajo una licencia Creative Commons